Audit, Risk and Finance

Subcommittee Minutes - 21 May 2019

Present: Her

Worship the Mayor R Reese, B Dahlberg and Mr J Murray

In

Attendance: Councillors P Matheson and B McGurk, Group

Manager Infrastructure (A Louverdis), Group Manager Community Services (R

Ball), Group Manager Corporate Services (N Harrison), Group Manager Strategy

and Communications (N McDonald) and Governance Adviser (J Brandt)

Apologies: Councillor

Barker and Mr Peters

1 Appointment of

Chairperson

|

The Group Manager Corporate

Services, Nikki Harrison, called for nominations from members to appoint a

chairperson for the meeting, as an apology had been received from the

appointed Chairperson and there was no appointed Deputy Chairperson for the

Subcommittee.

|

|

Resolved AUD/2019/013

|

|

|

That the Audit, Risk and Finance Subcommittee

1. Appoints Mr John Murray

as Chairperson of the Audit, Risk and Finance Subcommittee meeting on 21 May

2019.

|

|

Dahlberg/Her Worship the Mayor Carried

|

2. Apologies

|

Resolved AUD/2019/014

|

|

|

That the Audit, Risk and Finance Subcommittee

2. Receives

and accepts the apologies from Councillor Barker and Mr Peters.

|

|

Murray/Dahlberg Carried

|

3. Confirmation of

Order of Business

It was noted that agenda item 12

would be considered after item 7 due to time constraints of the speaker.

4. Interests

There were no updates to the

Interests Register, and no interests with items on the agenda were declared.

5. Public Forum

There was no public forum.

6. Confirmation of

Minutes

6.1 19

February 2019

Document number M4041, agenda

pages 7 - 13 refer.

|

Resolved AUD/2019/015

|

|

|

That the Audit, Risk and

Finance Subcommittee

1. Confirms the minutes of the

meeting of the Audit, Risk and Finance Subcommittee, held on 19 February

2019, as a true and correct record.

|

|

Murray/Dahlberg Carried

|

7. Chairperson's Report

There was no

Chairperson’s Report.

8. Quarterly Report to

31 March 2019

Document number R10169, agenda

pages 14 - 44 refer.

Tracey Hughes, Senior Accountant,

tabled a replacement chart for agenda page 23 (document A2194360) and noted

that the $50,000 debtor payment listed on agenda page 26 had been received

since the agenda was published.

Questions were answered regarding

dividends ahead of budget, reporting for the Investment Performance Audit

undertaken by NZTA, impacts on Council resulting from the Pigeon Valley fire

emergency in February 2019, management of methane levels at Founders Park, the

increased share of NRSBU costs for Council, progress putting a management plan

for Andrews Farm in place to address issues between user groups and the

predicted shortfall in capital expenditure.

A number of questions regarding the

Greenmeadows Centre and Queens Gardens Toilets in attachment 3 of the report

were noted for discussion later in the meeting, as part of the public excluded

section of the meeting.

|

Resolved AUD/2019/016

|

|

|

That

the Audit, Risk and Finance Subcommittee

Receives the report Quarterly Report to 31

March 2019 (R10169) and its

attachments (A2175573, A2176515 and A2180205).

|

|

Her Worship the Mayor/Murray Carried

|

|

Attachments

1 A2194360 -

Replacement table for page 23 of ARF Agenda 21 May 2019

|

9. Audit plan for the

year ending 30 June 2019

Document number R10202, agenda

pages 93 - 120 refer.

Jacques Coetzee of Audit New

Zealand spoke to the report, noting that he envisaged all Councils would be

provided with comparative data for benchmarking purposes by the end of the

year.

The meeting adjourned from

9.57a.m. until 10.33a.m.

|

Resolved AUD/2019/017

|

|

|

That

the Audit, Risk and Finance Subcommittee

1. Receives

the report Audit plan for the year ending 30 June 2019 (R10202) and its attachment (A2186543).

|

|

Murray/Her Worship the Mayor Carried

|

10. Quarterly Key Risks Report - 1

January to 31 March 2019

Document number R10167, agenda

pages 45 - 67 refer.

Arlene Akhlaq, Manager Business

Improvement, presented the report. She made a point of clarity regarding item

3.2 of the report (middle bullet point), noting that it was the consolidation

of options that was planned for June, with analysis already under way. Ms

Akhlaq further noted that a new rating system had been applied to Quarter 3

risk assessments.

Malcolm Hughes, Health and Safety

Advisor, explained the increased rating on higher hazard work situations (5.11)

as a result of the March terrorist attack in Christchurch. Mr Hughes answered

questions about levels of stress experienced by frontline staff and measures

the organisation was taking to provide support.

Ms Akhlaq answered questions

about the rating for environmental and legal liability risks, the order of

risks in the report, and whether the ratings reflected residual risk.

Nikki Harrison, Group Manager

Corporate Services answered a question about the Council’s disaster

recovery fund, noting the fund remained in deficit.

|

Resolved AUD/2019/018

|

|

|

That

the Audit, Risk and Finance Subcommittee

1. Receives

the report Quarterly Key Risks Report - 1 January to 31 March 2019 (R10167)

and its attachment (A2179264).

|

|

Dahlberg/Her Worship the Mayor Carried

|

11. Health & Safety Quarterly

Performance Report 1 January to 31 March 2019

Document number R10138, agenda

pages 68 - 83 refer.

Malcolm Hughes, Health and Safety

Advisor, answered questions about security incidents in the libraries, and

plans to limit access to certain internet sites in the libraries. Safe Work

Observation visits for Elected Members were discussed and it was noted that

Councillors would be invited to attend along with senior staff.

|

Resolved AUD/2019/019

|

|

|

That

the Audit, Risk and Finance Subcommittee

1. Receives

the report Health & Safety Quarterly Performance Report 1 January to 31

March 2019 (R10138) and its attachment

(A2173565).

|

|

Dahlberg/Murray Carried

|

12. Internal Audit - Quarterly

Progress Report to 31 March 2019

Document number R10129, agenda

pages 84 - 86 refer.

Lynn Anderson, Internal Audit

Analyst, spoke to the report and answered questions about the amounts of cash

handled in the libraries, the financial system used by the Building Unit and

how this was linked in with other Council systems. It was noted that the debtor

invoicing for the marina was being managed by Nelmac, and while debtors were

transferred to Council monthly, the overall system was separate from

Council’s financial system. Discussion took place regarding reporting

mechanisms where Audit New Zealand might raise issues with Nelmac for this

council asset.

|

Resolved AUD/2019/020

|

|

|

That

the Audit, Risk and Finance Subcommittee

1. Receives the report Internal Audit - Quarterly Progress

Report to 31 March 2019 (R10129) and its attachment (A2173040).

|

|

Murray/Her Worship the Mayor Carried

|

13. Internal Audit - Summary of New

or Outstanding Significant Risk Exposures and Control Issues to 31 March 2019

Document number R10130, agenda

pages 87 - 92 refer.

Lynn Anderson, Internal Audit

Analyst, provided a number of updates regarding business continuity planning

measures being introduced, training for the Incident Management Team, and

working with Civil Defence and Police to inform evacuation plans for Maitai

flood zones.

Alec Louverdis, Group Manager

Infrastructure, answered questions about the risk of water contamination as a

wilful act, and regular ongoing monitoring at the dam.

In regards to asset management

plans coming to committee meetings, it was requested that where plans were not

as developed as others, due to delays from the Pigeon Valley fires, this should

be highlighted in the report and assistance be given by finance officers to

assist members with robust decision-making.

|

Resolved AUD/2019/021

|

|

|

That

the Audit, Risk and Finance Subcommittee

1. Receives the report Internal

Audit - Summary of New or Outstanding Significant Risk Exposures and Control

Issues to 31 March 2019 (R10130) and its attachment (A2174097).

|

|

Murray/Dahlberg Carried

|

14. Exclusion

of the Public

|

Resolved AUD/2019/022

|

|

|

That the Audit, Risk and Finance Subcommittee

1. Excludes

the public from the following parts of the proceedings of this meeting.

2. The

general subject of each matter to be considered while the public is excluded,

the reason for passing this resolution in relation to each matter and the

specific grounds under section 48(1) of the Local Government Official

Information and Meetings Act 1987 for the passing of this resolution are as

follows:

|

|

Dahlberg/Her Worship the Mayor Carried

|

|

Item

|

General subject of each matter to be

considered

|

Reason for passing this resolution in

relation to each matter

|

Particular interests protected (where

applicable)

|

|

1

|

Audit, Risk and Finance Subcommittee Meeting -

Public Excluded Minutes - 19 February 2019

|

Section 48(1)(a)

The public conduct of this matter would be likely to

result in disclosure of information for which good reason exists under

section 7.

|

The withholding of the information is necessary:

· Section 7(2)(g)

To maintain

legal professional privilege

|

|

2

|

Quarterly Report to 31 March 2019 - Debtor

Discussion, Greenmeadows Centre and Queens Gardens Toilets

|

Section 48(1)(a)

The public conduct of this

matter would be likely to result in disclosure of information for which good

reason exists under section 7

|

The withholding of the information is necessary:

· Section 7(2)(a)

To protect the privacy of

natural persons, including that of a deceased person

· Section

7(2)(h)

To enable the local

authority to carry out, without prejudice or disadvantage, commercial activities

· Section

7(2)(g)

To maintain legal

professional privilege

|

|

3

|

Quarterly Update on Legal Proceedings

|

Section 48(1)(a)

The public conduct of this

matter would be likely to result in disclosure of information for which good

reason exists under section 7

|

The withholding of the information is necessary:

· Section 7(2)(g)

To maintain legal

professional privilege

|

|

4

|

Tax planning 10-year outlook report

|

Section 48(1)(a)

The public conduct of this

matter would be likely to result in disclosure of information for which good

reason exists under section 7

|

The withholding of the information is necessary:

· Section 7(2)(h)

To enable the local

authority to carry out, without prejudice or disadvantage, commercial

activities

|

The meeting went into public excluded session at 11.36a.m.

and resumed in public session at 1.11p.m.

Restatements

It was resolved while the public was

excluded:

|

2

|

PUBLIC EXCLUDED: Quarterly Update on Legal Proceedings

|

|

|

That

the Audit, Risk and Finance Subcommittee

1. Receives the report Quarterly

Update on Legal Proceedings (R10173)

and its attachment (A2186227); and

2. Agrees

that the decision (AUD/2019/026) only be released from public excluded

business; and

3. Agrees that Report (R10173) and its attachment (A2186227) be excluded from public release at this time.

|

|

3

|

PUBLIC EXCLUDED: Tax planning 10-year outlook report

|

|

|

That

the Audit, Risk and Finance Subcommittee

1. Receives

the report Tax planning 10-year outlook report (R10163) and its attachment

(A2179101); and

2. Agrees

that the decision (AUD/2019/027) only be released from public excluded

business; and

3. Agrees that Report (R10163) and attachment (A2179101) be excluded from public release at this time.

|

There being no further business the meeting ended at 1.11p.m.

Confirmed as a correct record of proceedings:

Chairperson

Date

Chairperson

Date

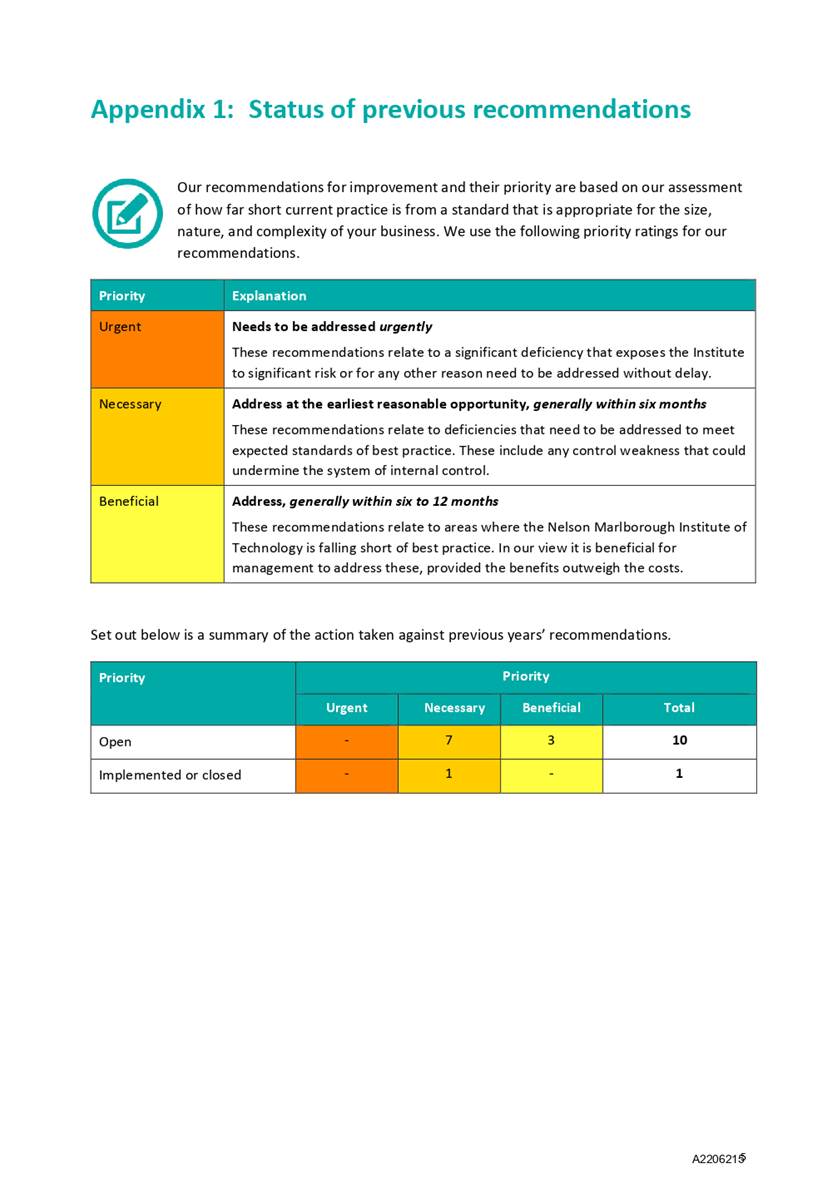

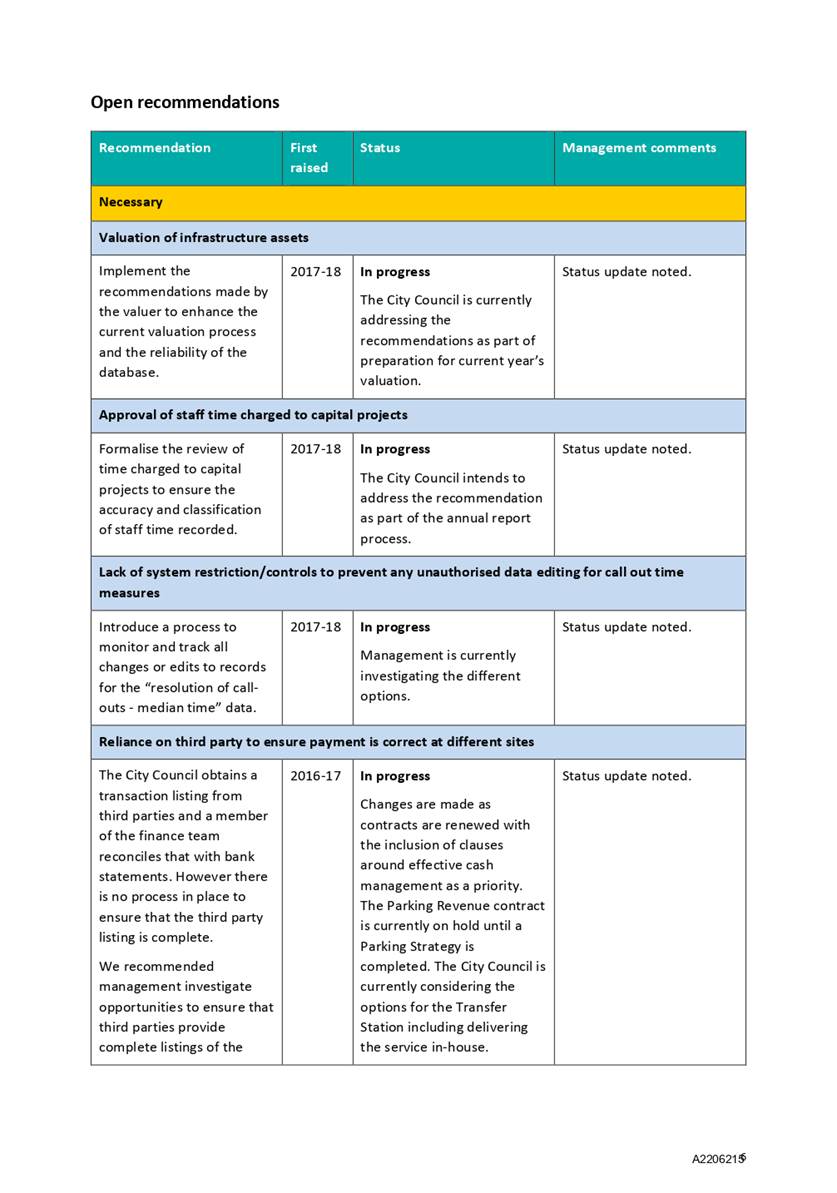

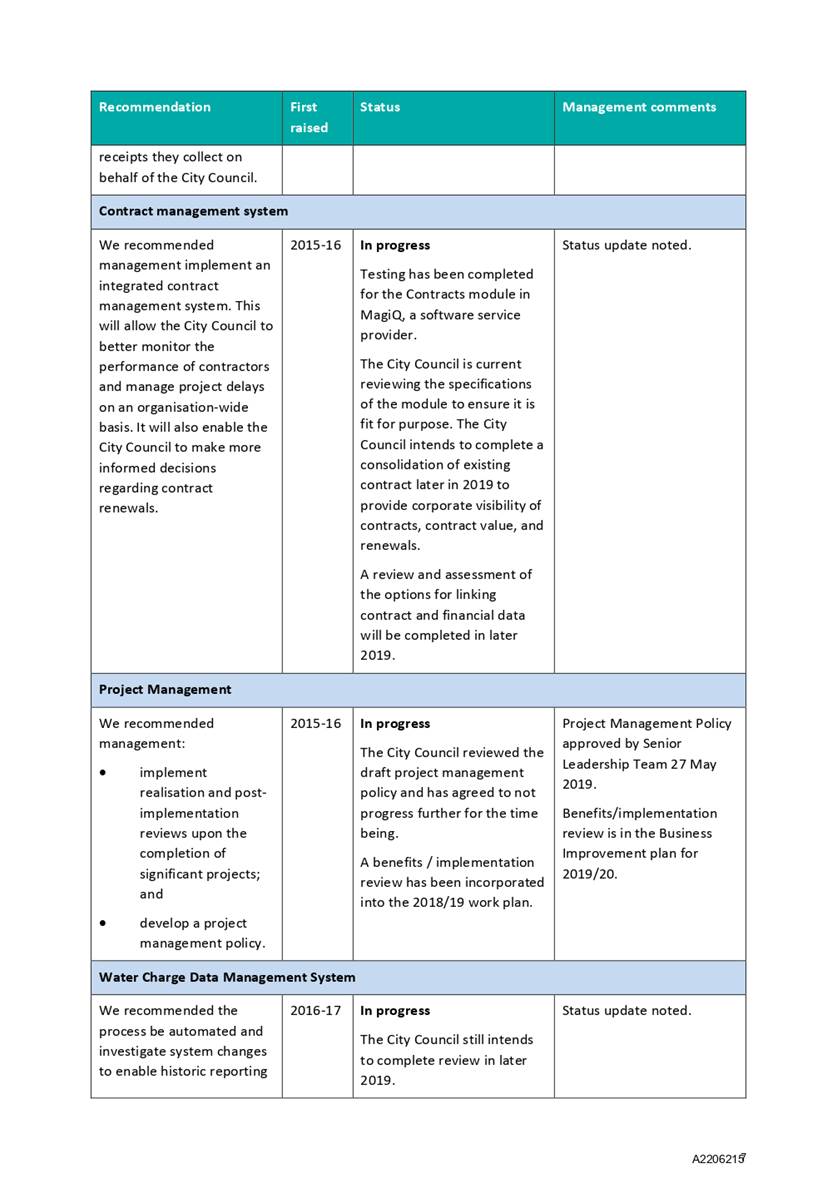

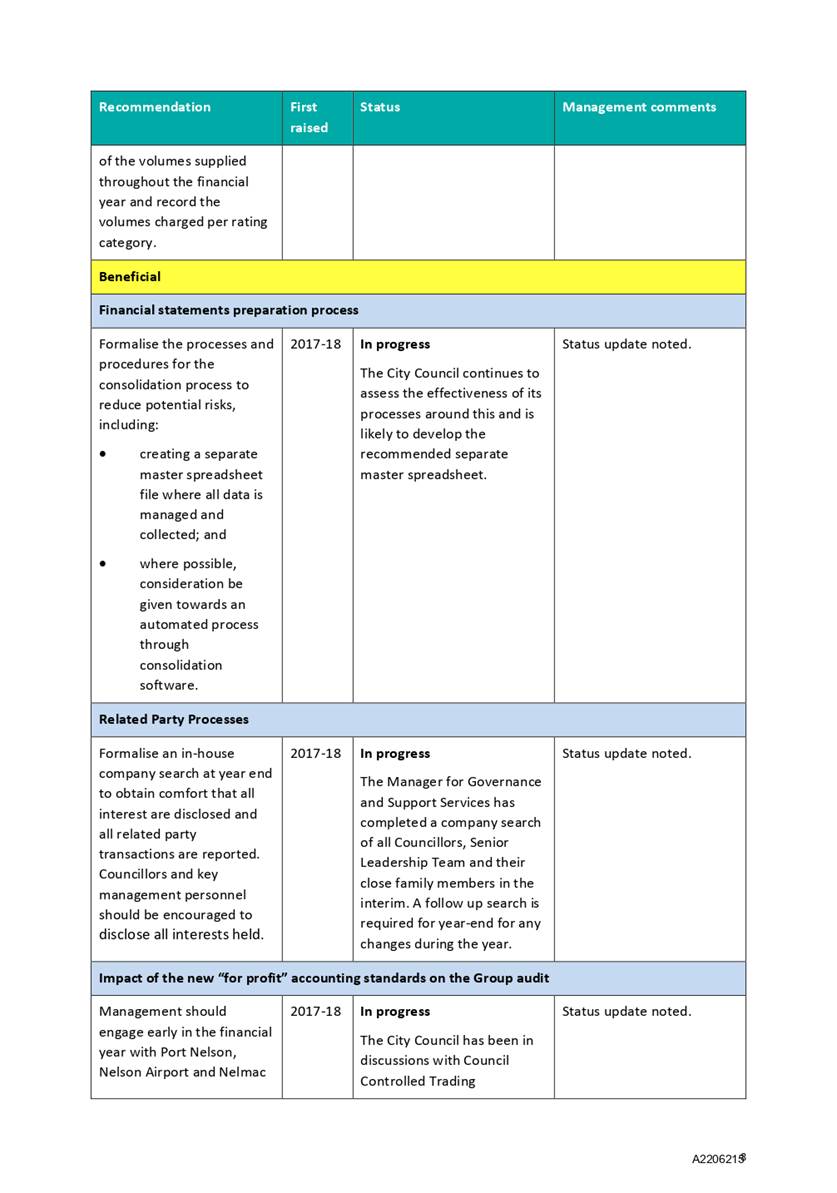

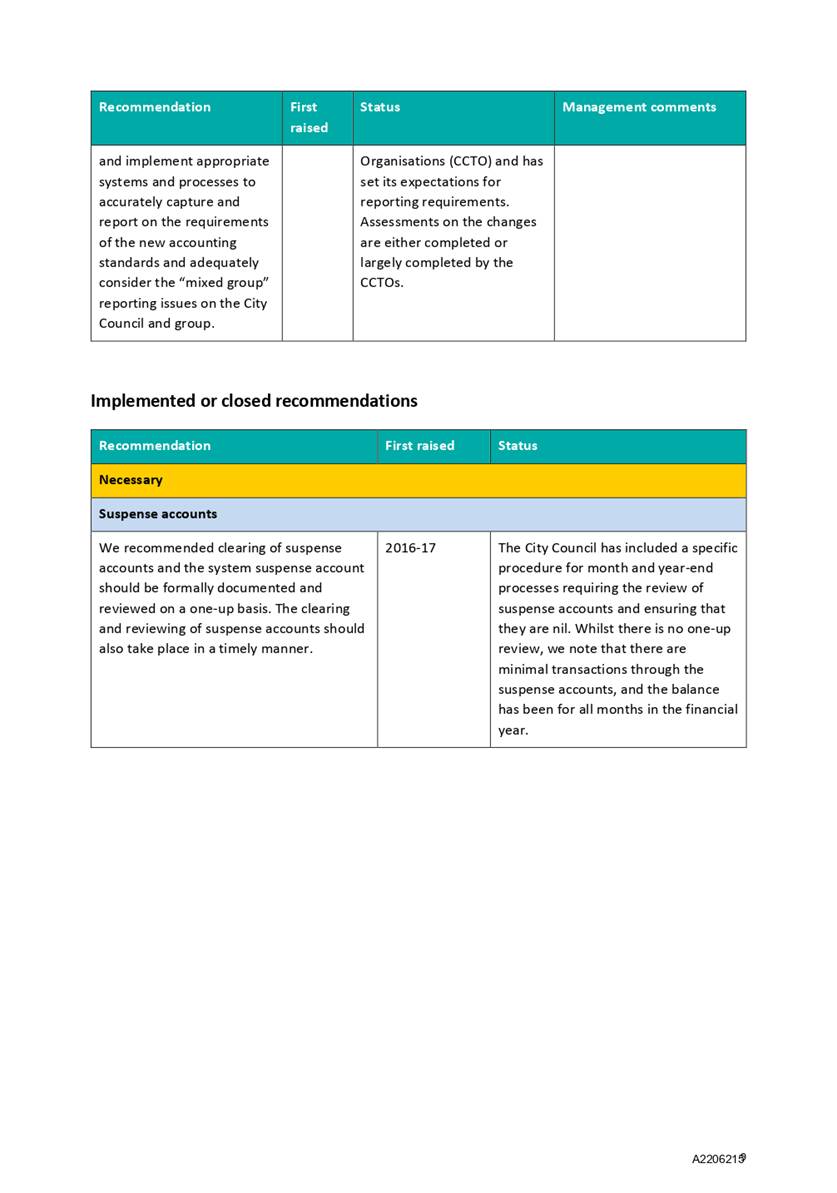

Item 7: Interim audit

letter for the year ending 30 June 2019

|

|

Audit, Risk and Finance Subcommittee

25 June 2019

|

REPORT R10240

Interim

audit letter for the year ending 30 June 2019

1. Purpose of Report

1.1 To provide the

letter to the Subcommittee on the interim audit for the year ending 30 June 2019

from Audit New Zealand.

2. Recommendation

|

That

the Audit, Risk and Finance Subcommittee

1. Receives the report Interim

audit letter for the year ending 30 June 2019 (R10240) and its attachment (A2206215); and

2. Notes

the status updates to previous audit recommendations.

|

3. Discussion

3.1 In mid-April

Audit New Zealand carried out an interim audit for the year ending 30 June 2019

on the Council's internal controls and the overall control environment. It

issued the draft letter on 11 June 2019 (Attachment 1).

3.2 There were no

minor or significant issues identified during the audit which is a good

result.

3.3 The Audit New

Zealand interim letter also contains a section on previous recommendations made

and an update on the status of these recommendations. Officers are

working to resolve these issues as soon as practical, while weighing up the

relative priority to other business improvement initiatives and internal audit

actions.

3.4 Audit NZ are

currently undertaking a review of the Councils procurement, contract management

and project management practices to support the planning, design, procurement

and delivery of renewals and new capital infrastructure. This will be

reported back on during the final audit.

4. Options

4.1 That the Subcommittee

note the status updates on previous matters in the letter to the Council on the

interim audit of Nelson City Council for the year ending 30 June 2019.

Author: Nikki

Harrison, Group Manager Corporate Services

Attachments

Attachment 1: A2206215

- Interim management letter from Audit NZ 11 June 2019 ⇩

|

Important considerations for decision making

|

|

1. Fit with Purpose of

Local Government

Section 99 of the Local Government Act 2002 requires

the audit of information contained in the Annual Report and Summary and the

interim audit forms part of that process.

|

|

2. Consistency with

Community Outcomes and Council Policy

This report supports the community outcome that

Council provides leadership, which includes the responsibility for protecting

finances and assets, and to have infrastructure which is efficient and

effective.

|

|

3. Risk

There is a risk that Council will not meet all its

legislative responsibilities if the recommendations from Audit NZ are not

accepted and actioned.

|

|

4. Financial impact

There is no financial impact.

|

|

5. Degree of significance

and level of engagement

This matter is of low significance because there are

no decisions to be made. Therefore no engagement has occurred.

|

|

6. Inclusion of

Māori in the decision making process

Māori have not been consulted in preparation of

this report.

|

|

7. Delegations

The Audit, Risk and Finance Subcommittee has the

responsibility for considering audit processes and management of financial

risk.

|

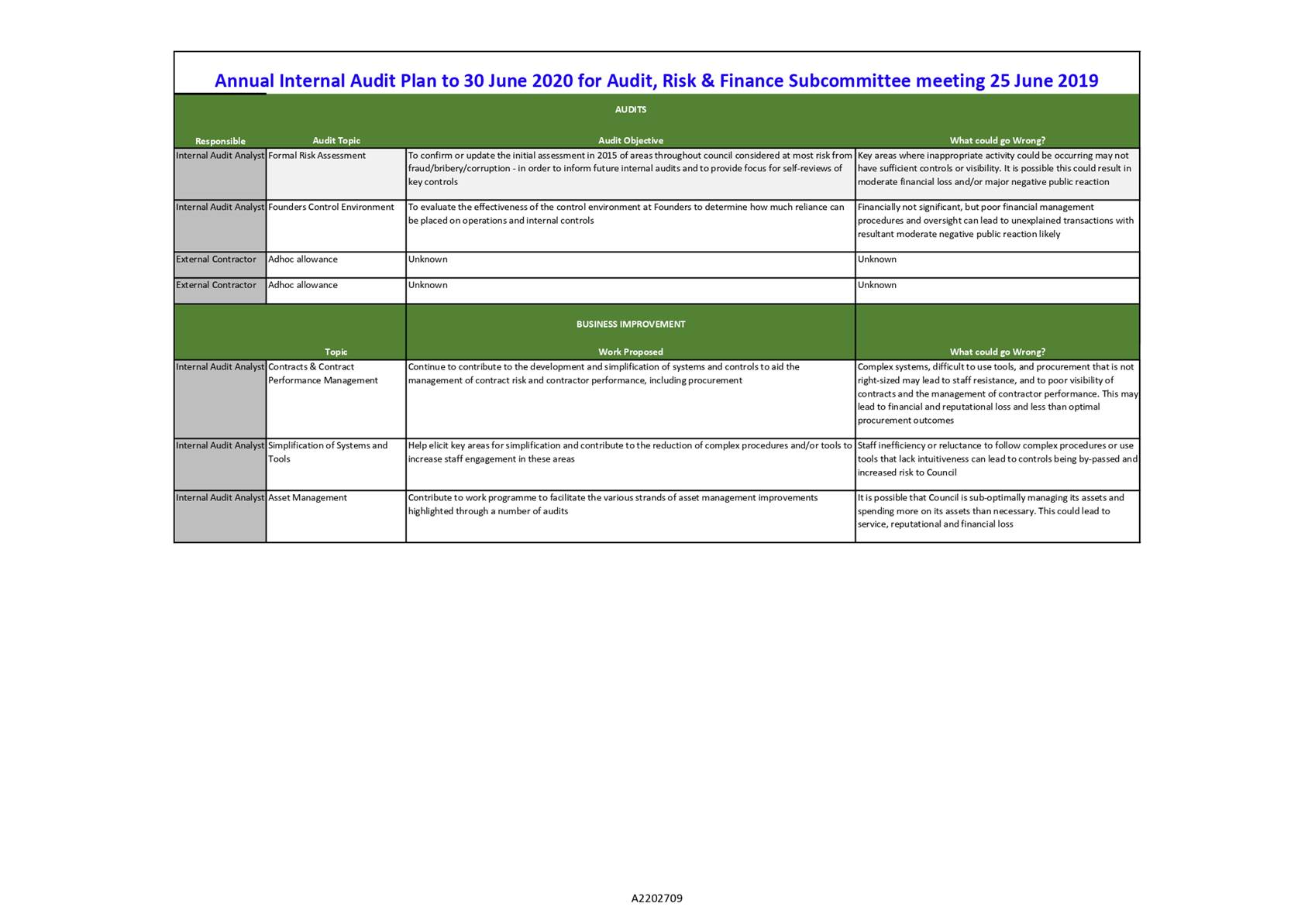

Item 8: Draft Annual

Internal Audit Plan - 30 June 2020

|

|

Audit, Risk and Finance Subcommittee

25 June 2019

|

REPORT R10266

Draft

Annual Internal Audit Plan - 30 June 2020

1. Purpose

of Report

1.1 To

approve the Draft Annual Internal Audit Plan to 30 June 2020.

2. Recommendation

|

That the Audit, Risk and Finance Subcommittee

1. Receives the report Draft Annual

Internal Audit Plan - 30 June 2020 (R10266)

and its attachment (A2202709).

|

Recommendation to Council

|

That the Council

1. Approves

the Draft Annual Internal Audit Plan - 30 June 2020 (A2202709).

|

3. Background

3.1 The

Internal Audit Charter approved by Council on 15 October 2015 requires that

at least annually, the Audit, Risk and Finance Subcommittee consider the Annual

Internal Audit Plan.

3.2 The

Internal Audit Charter cl. 8.2 requires the Internal Audit Plan to respond

to changes in the business.

3.3 Management

continues to assess how to allocate the internal audit resource to provide most

benefit to the organisation. This report reflects Management’s decision.

4. Discussion

4.1 The

Draft Internal Audit Plan (Attachment 1 A2202709) was compiled following

discussions with the Group Manager Corporate Services, Manager Business

Improvement, Chair of Audit, Risk and Finance subcommittee and Audit NZ.

Council’s most recent Quarterly Key Risks Report has also been reviewed.

4.2 Due

to the organisation’s current stretched capacity throughout and the

downstream impact on the organisation of internal audits, the Draft Plan

continues to provide a split plan incorporating internal audits and business

improvement activities.

4.3 The

proposed Plan would not compromise objectivity for the internal audit function.

4.4 This

proposal will not require additional budget this financial year.

Compilation of the Draft Internal Audit Plan and Best

Use of Internal Audit

4.5 The

availability of staff to respond to internal audits and their outcomes remains

limited. Alongside this, Council has a stated key goal in the Long Term Plan

2018-28 to lift Council performance.

4.6 The

officers believe that the best use of internal audit for this financial year is

to place some emphasis on business improvements which will contribute to the

achievement of the goal to lift Council performance.

4.7 This

proposal will not require additional budget for 2019/20 financial year.

4.8 The

Draft Plan allows for two currently unplanned audits and two pre-determined

audits. The planned topics are intentionally outside the business improvement

focus areas because: a) it ensures internal audit independence is not

compromised, and; b) it is considered too early to be auditing key areas such

as contract management where improvements are currently underway.

4.9 Following

discussions with Audit NZ, it is clear that priority areas for improvement are

contracts and contractor management. These have been included in the business

improvement section.

4.10 Other

key business improvement projects to help lift Council performance which

internal audit could contribute to include: a) improvements to asset management

systems and processes based on the drawing together of difference improvement

strands identified through audits; b) the simplification of procedures and

tools. Time has been provided for these in the Draft Plan.

5. Options

5.1 Option

1, is to approve the Draft Internal Audit Plan, which provides for a smaller

number of audits, as well as a contribution to business improvement. This

option is recommended.

5.2 The

alternative, Option 2, is for Council to decide the Internal Audit Plan should

only provide for internal audits this financial year. This is considered less favourable

as the downstream effect of a large volume of audits on the organisation is not

considered viable.

|

Option 1: Approve Draft

Internal Audit Plan proposal

|

|

Advantages

|

· Remedying

some of the already known weaknesses, such as contracts and contractor

performance management, as soon as practicable is in Council’s best

interests.

· The primary goal of business improvement is to increase effectiveness and efficiency to

improve the organisation’s ability to deliver services. A good improvement

plan will focus on the organisation’s most important activities

and any associated risks, and will address any necessary mitigations. This is

closely aligned to the internal audit process but is forward-looking, while

internal audit informs past performance.

|

|

Risks and Disadvantages

|

· There

may be future costs where external audits are required in areas where

internal audit has had some responsibility or involvement in the previous 12

months.

|

|

Option 2: Provide for Internal

Audits only in the Audit Plan

|

|

Advantages

|

· Council

will have a greater knowledge of areas across the organisation where there

have been systems or control failures.

|

|

Risks and Disadvantages

|

· A

higher volume of internal audits impacts on the organisation, taking scarce

organisational resources away from performing other key responsibilities,

which may have higher consequences to the organisation than those of the

risks found from an audit.

· While

control weaknesses are likely to be identified from an internal audit, the

ability to treat these is limited due to scarce resources throughout the

organisation.

|

Author: Lynn

Anderson, Internal Audit Analyst

Attachments

Attachment 1: A2202709 -

Draft Internal Audit Plan to 30 June 2020 ⇩

|

Important considerations for decision making

|

|

1. Fit

with Purpose of Local Government

This decision will help to ensure the resources

available in internal audit contribute optimally to business improvement and

internal auditing that will help give confidence that Council will be able to

meet its responsibilities effectively and efficiently.

|

|

2. Consistency

with Community Outcomes and Council Policy

This report supports the community outcome that

Council provides leadership, which includes the responsibility for protecting

finances and assets, and to have an infrastructure which is efficient and

effective.

|

|

3. Risk

It is more likely that Council may not meet its

responsibilities effectively and efficiently if this recommendation is not

accepted.

|

|

4. Financial

impact

This decision will fit within existing budgets.

|

|

5. Degree

of significance and level of engagement

This matter is of low significance because it does

not affect the level of service provided by Council or the way in which

services are delivered. Therefore no engagement has been undertaken.

|

|

6. Inclusion

of Māori in the decision making process

No engagement with Māori has been undertaken in

preparing this report.

|

|

7. Delegations

The Audit, Risk and Finance Subcommittee has the

delegation to consider the Annual Internal Audit Plan and the resourcing for

this each year.

Areas of Responsibility:

· The

internal audit function

Powers to Recommend:

· To

Council any matters within the areas of their responsibility

|

Audit, Risk and Finance

Subcommittee

Audit, Risk and Finance

Subcommittee