AGENDA

Ordinary meeting of the

Audit, Risk and Finance Subcommittee

Tuesday 13 February 2018

Commencing at 9.00am

Council Chamber

Civic House

110 Trafalgar Street, Nelson

Membership: Mr John Peters (Chairperson), Her Worship the

Mayor Rachel Reese, Councillor Ian Barker, Councillor Bill Dahlberg and Mr John

Murray

Guidelines for councillors

attending the meeting, who are not members of the Committee, as set out in

Standing Order 12.1:

·

All councillors, whether or not they are members of the

Committee, may attend Committee meetings

·

At the discretion of the Chair, councillors who are not Committee

members may speak, or ask questions about a matter.

·

Only Committee members may vote on any matter before the

Committee

It is good practice for both Committee members and

non-Committee members to declare any interests in items on the agenda.

They should withdraw from the room for discussion and voting on any of these

items.

Audit, Risk and Finance

Subcommittee

Audit, Risk and Finance

Subcommittee

13

February 2018

Page

No.

1. Apologies

Nil

2. Confirmation

of Order of Business

3. Interests

3.1 Updates

to the Interests Register

3.2 Identify

any conflicts of interest in the agenda

4. Public

Forum

5. Confirmation

of Minutes

5.1 14

November 2017 9 - 16

Document number M3123

Recommendation

That the

Audit, Risk and Finance Subcommittee

Confirms

the minutes of the meeting of the Audit, Risk and Finance Subcommittee, held on

14 November 2017, as a true and correct record.

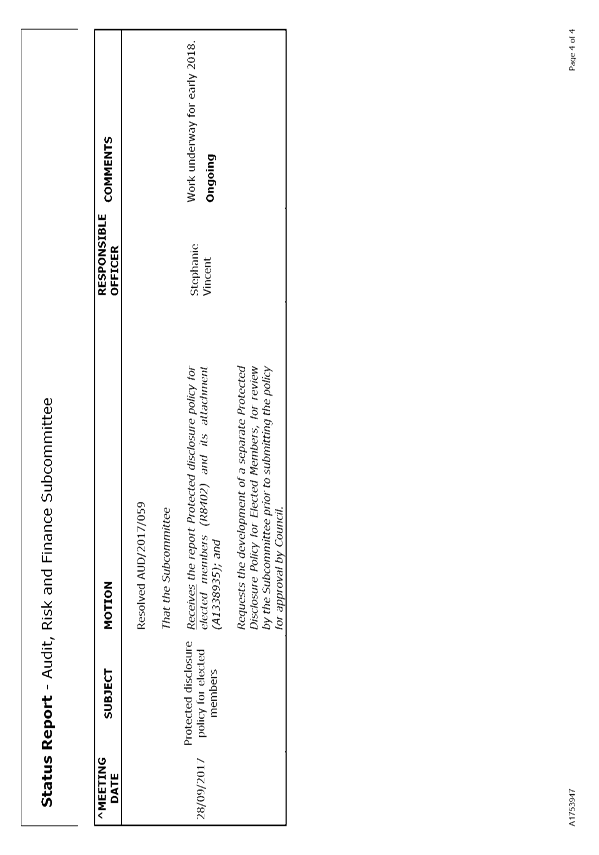

6. Status Report -

Audit Risk and Finance Subcommittee -13 February 2018 17 - 21

Document number R8930

Recommendation

That the Audit, Risk and Finance Subcommittee

Receives the Status Report Audit,

Risk and Finance Subcommittee 13 February 2018 (R8930) and its attachment (A1753947).

7. Chairperson's Report

8. Theatre Royal Loan 22 - 41

Document number R8838

Recommendation

That the Audit, Risk and Finance Subcommittee

Receives the report Theatre Royal

Loan (R8838) and its attachments

(A1898640 and A1906067).

Recommendation to Council

That the

Council

Agrees

to take on the Nelson Historic Theatre Trust’s loan of $632,256 from the

Nelson Building Society; and

Confirms

that it expects the Nelson Historic Theatre Trust to repay the full loan

amount (total $2,132,256); and

Agrees

to increase the mortgage over the building to $2,132,256; and

Sets

the loan repayment terms for the Nelson Historic Theatre Trust at $60,000 per

year, payable quarterly (commencing in September 2018), with payment terms

subject to review every five years.

9. Audit NZ - Letter to

the Council on the audit for year ending 30 June 2017 42 - 50

Document number R8222

Recommendation

That the Audit, Risk and Finance Subcommittee

Receives the report Audit NZ -

Letter to the Council on the audit for year ending 30 June 2017 (R8222) and its attachment (A1891276).

10. Tendering Processes - Follow Up

Report 51 - 74

Document number R8832

Recommendation

That the Audit, Risk and Finance

Subcommittee

Receives the report Tendering

Processes - Follow Up Report (R8832)

and its attachments (A1856124 and A1897197); and

Notes

that all recommendations rated as high from the 2016 Crowe Horwath Report have

been actioned.

11. Audit NZ - Audit Engagement

Letter for the Long Term Plan 2018-28 75 - 103

Document number R8865

Recommendation

That the Audit, Risk and Finance

Subcommittee

Receives the report Audit NZ -

Audit Engagement Letter for the Long Term Plan 2018-28 (R8865) and its attachment (A1894901); and

Notes the subcommittee can provide feedback

on the Audit Engagement Letter to Audit NZ if required and that the Mayor will

sign the letter once the subcommittee’s feedback (if any) has been

incorporated.

12. Corporate Report to 31 December

2017 104 - 114

Document number R8857

Recommendation

That the Audit, Risk and Finance Subcommittee

Receives the report Corporate

Report to 31 December 2017 (R8857)

and its attachments (A1903395 and A1904902).

13. Internal Audit Quarterly Report

to 31 December 2017 115 - 117

Document number R8869

Recommendation

That the Audit, Risk and Finance Subcommittee

Receives the report Internal Audit

Quarterly Report to 31 December 2017 (R8869)

and its attachment (A1894689).

14. Key Organisational Risks

Calendar 2017 - 4th Quarterly Report 118 - 135

Document number R8797

Recommendation

That the Audit, Risk and Finance

Subcommittee

Receives the report Key

Organisational Risks Calendar 2017 - 4th Quarterly Report (R8797) and its attachment A1895817.

15. Health, Safety and Wellbeing

Performance Report, October - December 2017 136 - 152

Document number R8871

Recommendation

That the Audit, Risk and Finance

Subcommittee

Receives the report Health, Safety

and Wellbeing Performance Report, October - December 2017 (R8871) and its attachment (A1895727).

16. Security Incidents at Council Libraries 153 - 166

Document number R8872

Recommendation

That the Audit, Risk and Finance

Subcommittee

Receives the report Security

Incidents at Council Libraries (R8872)

and its attachment (A1848048).

17. Recruitment

in a Tight Labour Market 167 - 184

Document number R8885

Recommendation

That the Audit, Risk and Finance

Subcommittee

Receives the report Recruitment in

a Tight Labour Market (R8885) and

its attachment (A1896279).

Public Excluded Business

18. Exclusion

of the Public

Recommendation

That the Audit,

Risk and Finance Subcommittee

Excludes

the public from the following parts of the proceedings of this meeting.

The

general subject of each matter to be considered while the public is excluded,

the reason for passing this resolution in relation to each matter and the

specific grounds under section 48(1) of the Local Government Official

Information and Meetings Act 1987 for the passing of this resolution are as

follows:

|

Item

|

General subject of each matter to be considered

|

Reason for passing this resolution in relation to each matter

|

Particular interests protected (where applicable)

|

|

1

|

Audit,

Risk and Finance Subcommittee Meeting - Public Excluded Minutes - 14

November 2017

|

Section

48(1)(a)

The public

conduct of this matter would be likely to result in disclosure of information

for which good reason exists under section 7.

|

The

withholding of the information is necessary:

· To

maintain legal professional privilege

|

19. Re-admittance

of the public

Recommendation

That the Audit,

Risk and Finance Subcommittee

Re-admits

the public to the meeting.

Note:

·

The Commercial Subcommittee is scheduled to commence at 1pm.

·

Lunch will be available from 12pm.

(delete as appropriate)

Audit, Risk and Finance Subcommittee

Minutes - 14 November 2017

Minutes of a meeting of

the Audit, Risk and Finance Subcommittee

Held in the Council

Chamber, Civic House, 110 Trafalgar Street, Nelson

On Tuesday 14 November

2017, commencing at 9.01am

Present: Mr

J Peters (Chairperson), Her Worship the Mayor R Reese, Councillor I Barker,

Councillor B Dahlberg and Mr J Murray

In Attendance: Councillors

G Noonan, P Matheson, S Walker, Group Manager Infrastructure (A Louverdis),

Group Manager Strategy and Environment (C Barton), Group Manager Community

Services (C Ward), Group Manager Corporate Services (N Harrison), Senior

Strategic Adviser (N McDonald) Tracey Hughes and Governance Adviser (E

Stephenson)

Apology: Her

Worship the Mayor R Reese for lateness

1. Apologies

|

Resolved AUD/2017/069

That the Audit, Risk and

Finance Subcommittee

Receives and

accepts the apology from Her Worship the Mayor for lateness.

Barker/Dahlberg Carried

|

2. Confirmation of Order of Business

There was no change to the order

of business.

3. Interests

Councillor Barker declared an

interest in Tahunanui Beach Holiday Park.

4. Public Forum

There was no public forum.

5. Confirmation of Minutes

5.1 28

September 2017

Document number M2963, agenda

pages 7 - 13 refer.

|

Resolved AUD/2017/070

That the Audit, Risk and

Finance Subcommittee

Confirms the

minutes of the meeting of the Audit, Risk and Finance Subcommittee, held on

28 September 2017, as a true and correct record.

Murray/Barker Carried

|

6. Status Report - Audit Risk and

Finance Subcommittee -14 November 2017

Document number R8676, agenda

pages 14 - 17 refer.

Group Manager Corporate Services,

Nikki Harrison answered questions on this item.

|

Resolved AUD/2017/071

That the Audit, Risk and Finance Subcommittee

Receives the Status Report

Audit, Risk and Finance Subcommittee 14 November 2017 (R8676) and its attachment (A1753947).

Barker/Murray Carried

|

Attendance: Her Worship the Mayor entered the meeting at

9.06am.

7.

|

Chairperson's Report

|

|

The Chairperson provided a verbal report in which he

commented on report scheduling, noting that the August month-end Corporate

Report had only been received that day, which was ten weeks after the period

in question. He said that this did not provide opportunity for adequate

oversight and monitoring and requested that the minutes record that the

Subcommittee did need more timely information, noting that the Group Manager

Corporate Services would be tabling an update on September month-end during

the Corporate Report item.

|

|

Resolved AUD/2017/072

That the Audit, Risk and

Finance Subcommittee

Receives the

Chairperson’s verbal report.

Mr/Barker Carried

|

8. Report from 28 September Works

and Infrastructure Committee (Chairperson’s Report)

Document number R8681, agenda

pages 18 - 20 refer.

Chairperson of the Works and

Infrastructure Committee, Councillor Walker, spoke to the report and Group

Manager Infrastructure Alec Louverdis answered questions.

|

Resolved AUD/2017/073

That the Audit, Risk and Finance

Subcommittee

Receives the

(Chairperson’s) Report from 28 September Works and Infrastructure

Committee (R8681) and its

attachment (A1839317).

Dahlberg/Barker Carried

|

9. Corporate Report to 31 August

2017

Document number R7001, agenda

pages 21 - 34 refer.

Group Manager Corporate Services,

Nikki Harrison, spoke to the report and answered questions. The September 2017

Key Indicators report was tabled.

A typographical error was pointed

out in agenda page 28, Attachment 1 – Borrowing statistics - 33.6% should

be 3.36%.

Councillor Barker left the table

at 9.43am, during discussion on the Tahunanui Beach Holiday Park and returned

to the table at 9.48am.

|

Resolved AUD/2017/074

That the Audit, Risk and Finance Subcommittee

Receives the report Corporate

Report to 31 August 2017 (R7001)

and its attachments (A1854215, A1853357 and A1852936).

Murray/Dahlberg Carried

|

|

Attachments

1 A1865625 Key

Indicators September 2017

|

10. Health and Safety: Quarterly

Report

Document number R7022, agenda

pages 35 - 48 refer.

Health and Safety Adviser Malcolm

Hughes answered questions on the report.

|

Resolved AUD/2017/075

That the Audit, Risk and Finance Subcommittee

Receives the report Health and

Safety: Quarterly Report (R7022)

and its attachment (A1845583).

Her Worship the Mayor/Dahlberg Carried

|

|

Recommendation to Council

AUD/2017/076

That

the Council

Notes

the report Health and Safety: Quarterly Report (R7022) and its attachment (A1845583); and

Acknowledges

the assessment of critical health and safety risks contained in the

attachment (A1845583).

Her Worship the Mayor/Dahlberg Carried

|

11. Insurance renewal 2017/18

Document number R7525, agenda

pages 49 - 54 refer.

|

Resolved AUD/2017/077

That the Audit, Risk and Finance Subcommittee

Receives the report Insurance

renewal 2017/18 (R7525); and

Notes

the decision made to exit Local Authority Protection Program (LAPP) and join

the Aon South Island Collective from 1 July 2017; and

Notes

the decision made to purchase an additional $125 million shared limit (to a

total limit of $250 million) with a Council sublimit of $160 million from 1

November 2017.

Dahlberg/Barker Carried

|

12. Internal Audit Quarterly

Report to 30 September 2017

Document number R7589, agenda

pages 55 - 59 refer.

Internal Audit Analyst, Lynn

Anderson updated the committee on recent audits undertaken and answered

questions.

|

Resolved AUD/2017/078

That the Audit, Risk and Finance Subcommittee

Receives the report Internal

Audit Quarterly Report to 30 September 2017 (R7589).

Dahlberg/Barker Carried

|

13. Key Organisational Risks

2017 - 3rd Quarterly Report

Document number R7681, agenda

pages 60 - 77 refer.

Risk and Procurement Analyst,

Steve Vaughan, spoke to the report and answered questions.

Discussion took place on the

risks to the organisation caused by staff shortages and it was agreed to add a

request for the provision of a report to the Audit, Risk and Finance

Subcommittee on this issue to the motion.

|

Resolved AUD/2017/079

That the Audit, Risk and Finance Subcommittee

Receives the report Key

Organisational Risks 2017 - 3rd Quarterly Report (R7681) and its attachment (A1842185); and

Requests

officers report back on what is being done to mitigate

the risk to the organisation and its business resulting from staff shortages.

Murray/Her Worship the Mayor Carried

|

Her Worship the Mayor R Reese

requested that the public be excluded to allow confidential discussion on a

matter relating to a reputational risk to Council, as part of Item 13 - Key

Organisational Risks 2017 – 3rd Quarterly Report.

Public

Excluded Business

14. Exclusion of the Public

|

Resolved AUD/2017/080

That the Audit, Risk and Finance Subcommittee

Excludes

the public from the following parts of the proceedings of this meeting.

The

general subject of each matter to be considered while the public is excluded,

the reason for passing this resolution in relation to each matter and the

specific grounds under section 48(1) of the Local Government Official

Information and Meetings Act 1987 for the passing of this resolution are as

follows:

|

Item

|

General subject of each matter to be considered

|

Reason for passing this resolution in relation to

each matter

|

Particular interests protected (where applicable)

|

|

1

|

Key Organisational

Risks 2017 - 3rd Quarterly Report

|

Section 48(1)(a)

The public conduct of

this matter would be likely to result in disclosure of information for

which good reason exists under section 7.

|

The withholding of the

information is necessary:

Section 7(2)(g)

·

To maintain legal professional

privilege

|

Her Worship the Mayor/Dahlberg Carried

|

The

meeting went into public excluded session at 10.50am and resumed in public

session at 11.19am, at which time the meeting was adjourned.

15. Re-admittance

of the public

|

Resolved AUD/2017/081

That the Audit, Risk and

Finance Subcommittee

Re-admits the public to

the meeting.

Her Worship the Mayor/Barker Carried

|

The

meeting was reconvened at 11.38am.

16. Section 17A Service Delivery

Review progress report

Document number R8167, agenda

pages 78 - 123 refer.

Policy Adviser, Gabrielle Thorpe,

spoke to the report and answered questions.

It was noted that the correct

date for the funding model change for Saxton field was July 2018, not September

2018, as stated on page 102 of the agenda (Attachment 5 of the report).

|

Resolved AUD/2017/082

That the Audit, Risk and Finance Subcommittee

Receives the report Section 17A

Service Delivery Review progress report (R8167) and its attachments (A1824993, A1845758, A1844354,

A1843923, A1837281, A1633609, A1819898, A1844359, A1853049).

Barker/Dahlberg Carried

|

17. Tax Risk Management Strategy

Document number R8585, agenda

pages 124 - 132 refer.

Senior Accountant, Tracey Hughes

spoke to the report and answered questions.

Discussion took place regarding

the management of council’s tax liability as a whole to maximise its

efficiency. It was noted that Council would be engaging with Tasman District

Council to consider this topic. It was agreed that a request for the provision

of a report to the Subcommittee on efficient tax management, after that work

has been completed, be added to the motion.

|

Resolved AUD/2017/083

That the Audit, Risk and Finance Subcommittee

Receives the report Tax Risk

Management Strategy (R8585) and

its attachments (A1847439 and A1847460); and

Requests

that a review is undertaken of the group tax strategy to ensure maximum group

efficiencies.

Murray/Dahlberg Carried

|

|

Recommendation to Council

AUD/2017/084

That

the Council

Adopts

the Tax Risk Management Strategy (A1847439).

Barker/Dahlberg Carried

|

There being no further business the

meeting ended at 11.55am.

Confirmed as a correct record of proceedings:

Chairperson

Date

Chairperson

Date

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

REPORT R8930

Status

Report - Audit Risk and Finance Subcommittee -13 February 2018

1. Purpose

of Report

1.1 To

provide an update on the status of actions requested and pending.

2. Recommendation

|

That the Audit, Risk and Finance Subcommittee

Receives the Status Report

Audit, Risk and Finance Subcommittee 13 February 2018 (R8930) and its attachment (A1753947).

|

Attachments

Attachment 1: A1753947

- Audit Risk and Finance Subcommittee Status Report ⇩

Item

6: Status Report - Audit Risk and Finance Subcommittee -13 February 2018:

Attachment 1

Item 8: Theatre Royal

Loan

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

REPORT R8838

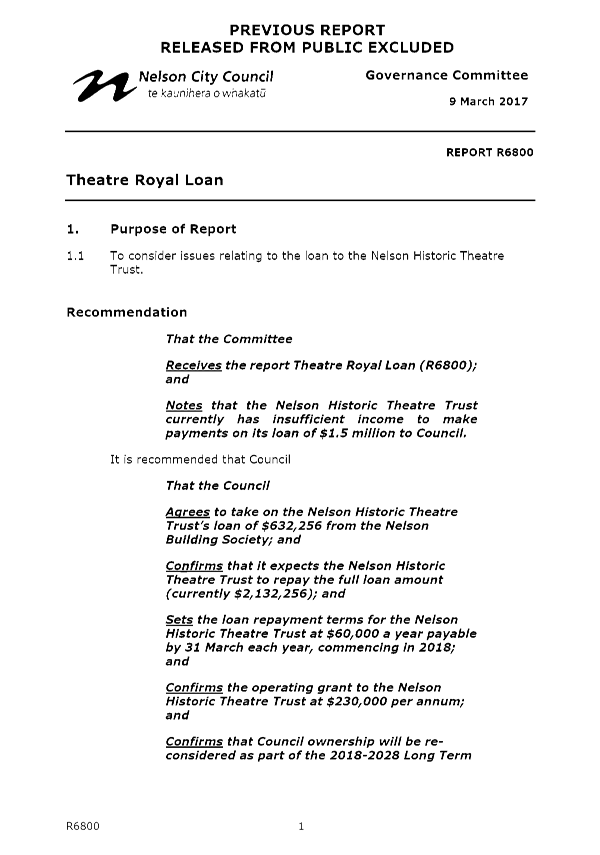

Theatre

Royal Loan

1. Purpose

of Report

1.1 To

consider issues relating to the loan to the Nelson Historic Theatre Trust.

2. Summary

2.1 The

Nelson Historic Theatre Trust received a loan ($1.5 million) from Council to

complete the capital redevelopment of the Theatre. The loan is secured against

the building asset. The Trust also has a loan ($0.63 million) from the Nelson

Building Society (NBS). Due to a combination of issues, repayments have not

been made against the Council loan, and the Trust is making interest only

repayments against the NBS loan.

2.2 This

position is unsustainable. It is recommended that Council takes on the NBS loan

and requests the Trust make repayments against that loan of $60,000 per annum.

This course of action gives both the Trust and the Council some long term

certainty.

3. Recommendation

1.

|

That the Audit, Risk and Finance

Subcommittee

Receives the report Theatre

Royal Loan (R8838) and its

attachments (A1898640 and A1906067).

|

Recommendation to Council

|

That the Council

Agrees to take on the Nelson

Historic Theatre Trust’s loan of $632,256 from the Nelson Building

Society; and

Confirms that it expects the

Nelson Historic Theatre Trust to repay the full loan amount (total

$2,132,256); and

Agrees to increase the mortgage

over the building to $2,132,256; and

Sets the loan repayment terms

for the Nelson Historic Theatre Trust at $60,000 per year, payable quarterly

(commencing in September 2018), with payment terms subject to review every

five years.

|

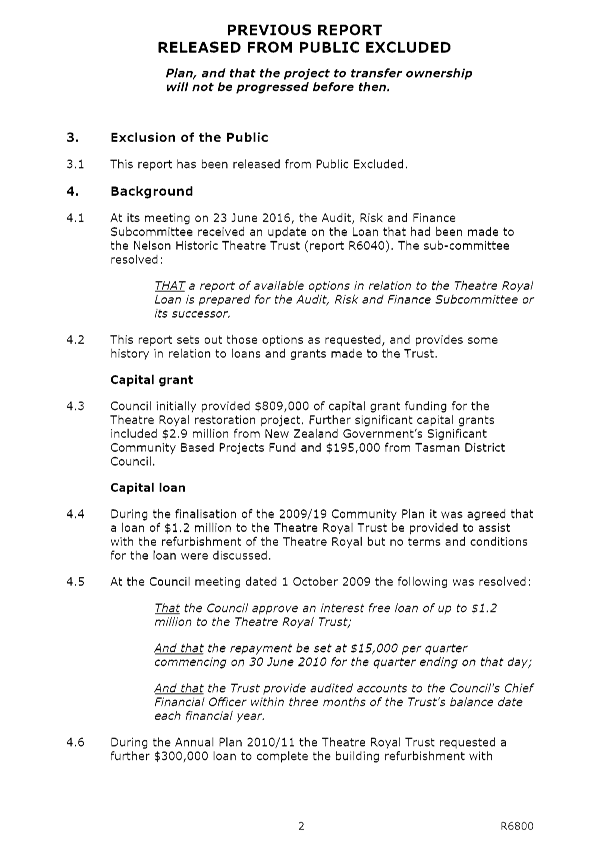

4. Background

4.1 At

its meeting on 23 June 2016, the Audit, Risk and Finance Subcommittee received

an update on the Loan that had been made to the Nelson Historic Theatre Trust

(report R6040). The Trust had not been making repayments on its loan to

Council, pending long term resolution of the planned transfer of ownership of

the facility.

4.2 The

sub-committee resolved:

THAT a report of

available options in relation to the Theatre Royal Loan is prepared for the

Audit, Risk and Finance Subcommittee or its successor.

4.3 A

further report (R6800, attachment 1) was presented to the Governance Committee

on 9 March 2017 where the Committee requested that a workshop be held to

consider all options, and to allow the Committee to hear from the Chairperson

of the Trust. That workshop took place on 14 September 2017.

4.4 The

Committee heard that the Trust was in a stable financial position

operationally, but faced continuing uncertainty due to the loan position.

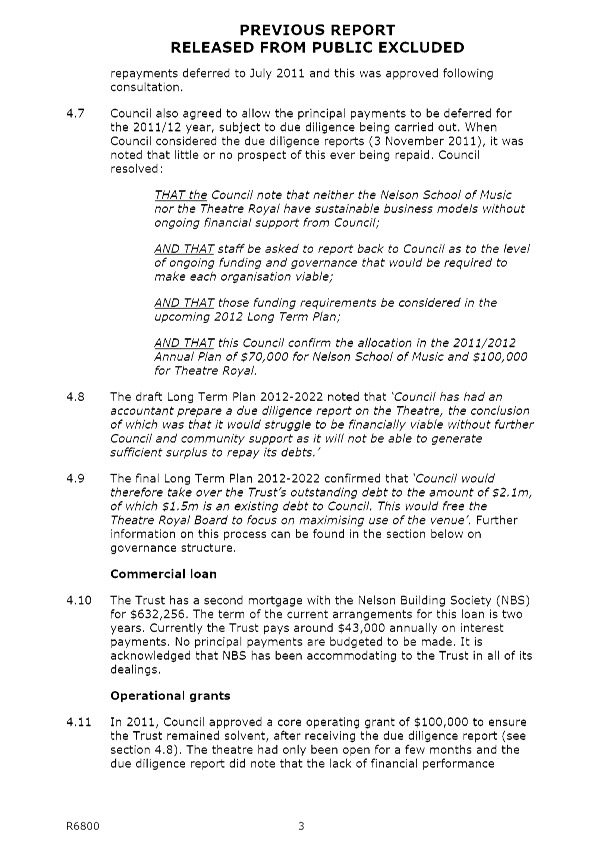

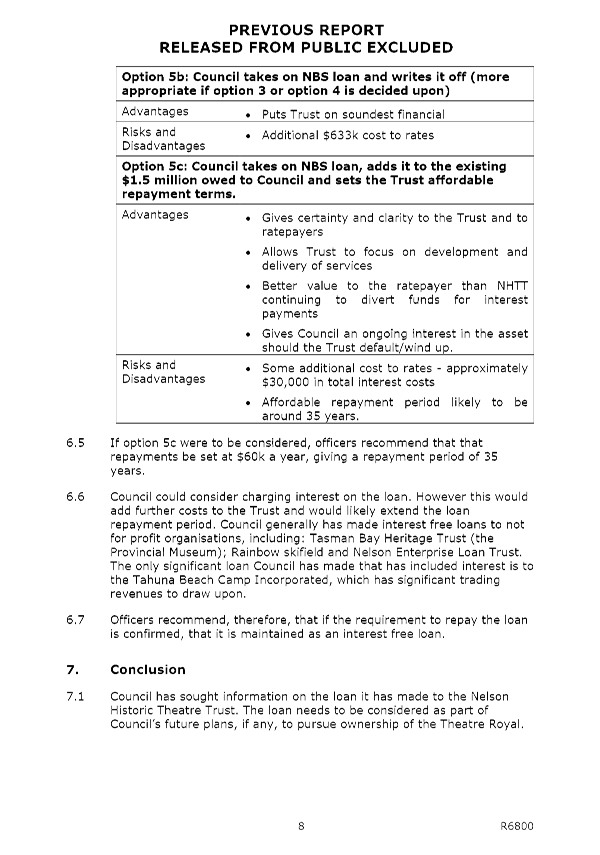

5. Discussion

5.1 The

Trust continues to operate with a small net surplus. The Trust has a renewal

programme that requires significant investment in the next few years and has

identified the need to deliver surpluses in order to fund those renewals.

The total expected over the next 15 years is approximately $890,000.

5.2 The

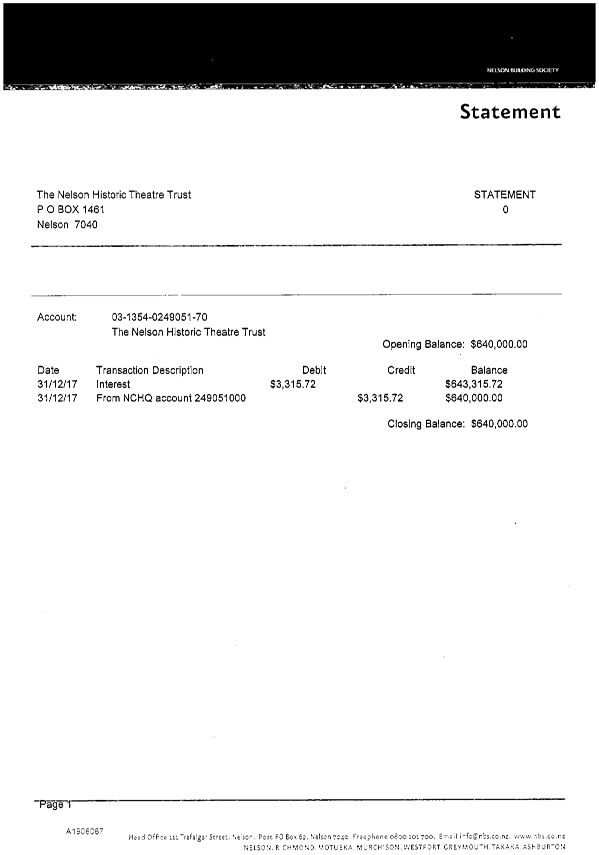

Trust owes Council $1.5 million and also has a loan of $632,256 with the NBS.

It currently pays around $40,000 interest to the NBS, but has not been able to

afford repayments on capital.

5.3 The

Trust has confirmed that its preferred course of action is as recommended in

this report. Repayments of $60,000 per year, payable quarterly, are manageable

and will allow the Trust to fund the renewal programme. There is a risk that

asking the Trust to fund more than $60,000 per annum would be financially

unsustainable or would lead to assets not being maintained/renewed

appropriately. The Trust is not seeking additional operating grant increases

over and above CPI.

5.4 The

Trust has agreed to five-yearly reviews in order that Council can be assured

that repayments will increase if the Trust is in a financial position to do so.

5.5 The

increased cost to Council from providing the additional loan ($632,256) at an

interest free rate is likely to be around $30,000 per year.

Comparison of

Grant funding

5.6 The

Committee asked for further information on the level of grant funding received

by the Trust.

|

Project

|

NCC grant

|

Other grants/ fundraising

|

Loans

|

|

Suter

|

$6 million

|

$6 million

|

Nil

|

|

Nelson School of Music

|

$3.15 million

|

$3.4 million

|

Nil

|

|

Theatre Royal

|

$0.805 million

|

$3.675 million

|

$2.14 million

|

5.7 When

Council initially received the refurbishment proposal from the Trust, the

estimated project cost was $2 million. The combined grants made available from

Nelson City and Tasman District Councils at that time added up to $1 million.

Subsequent decisions of Council were to loan fund rather than grant fund as the

project costs escalated.

5.8 On

that basis it is not recommended that prior loans made be converted into

grants.

6. Options

6.1 A

wide range of options were presented in report R6800. These have been condensed

based on prior feedback. The recommended option is for Council to take on the

NBS loan and require repayment of $15,000 each quarter, $60,000 total each

year. It is also recommended that this arrangement be reviewed every five years

to enable the Trust to increase its repayments if its finances allow.

|

Option 1: Council takes on NBS

loan, adds it to the existing $1.5 million owed to Council and sets the Trust

affordable repayment terms.

|

|

Advantages

|

· Gives

certainty and clarity to the Trust and to ratepayers

· Allows

Trust to focus on development and delivery of services

· Better

value to the ratepayer than NHTT continuing to divert funds for interest

payments

· Gives

Council an additional interest in the building asset should the Trust

default/wind up.

|

|

Risks and Disadvantages

|

· Some

additional cost to rates - approximately $30,000 p.a. in total interest costs

· The

repayment period likely to be around 35 years (at the suggested repayment

amount).

|

|

Option 2: Council seeks to

enforce current loan repayment terms and conditions

|

|

Advantages

|

· Adheres

to the original agreement

|

|

Risks and Disadvantages

|

· Does

not resolve NBS loan issues

· The

Trust may not be able to afford the payment schedule leading to either cuts

in service or loan defaults

· May

result in significant unbudgeted costs to Council if the Trust were to decide

to wind up

|

|

Option 3: Council writes off

part or all of the loan

|

|

Advantages

|

· Gives

certainty and clarity to the Trust and to ratepayers

· Allows

Trust to focus on development and delivery of services

|

|

Risks and Disadvantages

|

· Additional

cost to rates (up to $2.1 m)

· Runs

counter to previous Council decisions

· Sets

precedent to other community groups that Council may write off loan funding.

|

7. Conclusion

7.1 Council

has requested further information to enable it to make a decision on how it

will treat the Nelson Historic Theatre Trust’s outstanding loans. A

recommended way forward is presented.

Chris

Ward

Group

Manager Community Services

Attachments

Attachment 1: A1898640 - Previous report

- Theatre Royal Loan ⇩

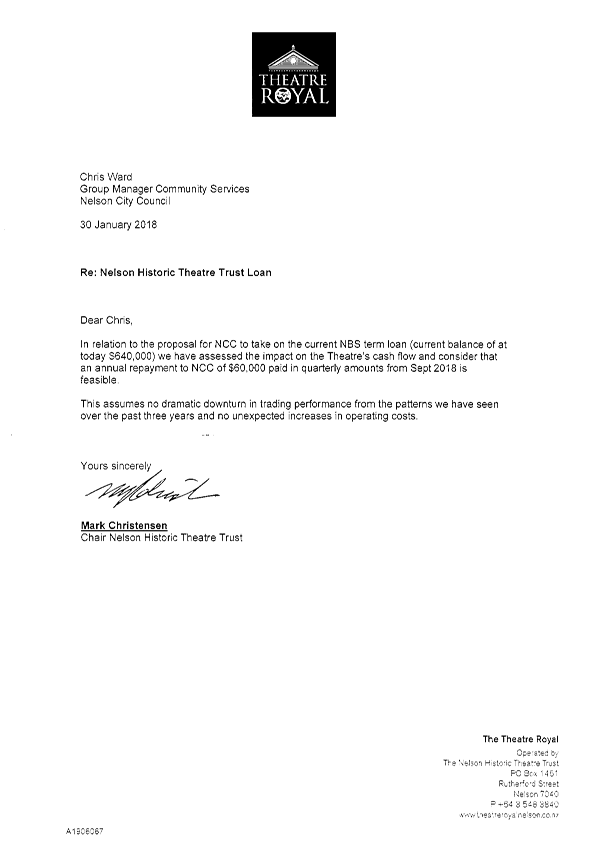

Attachment 2: A1906067

- Theatre Royal Loan - Letter of Support and Nelson Building Society Statement

- Mark Christensen - 30Jan2018 ⇩

|

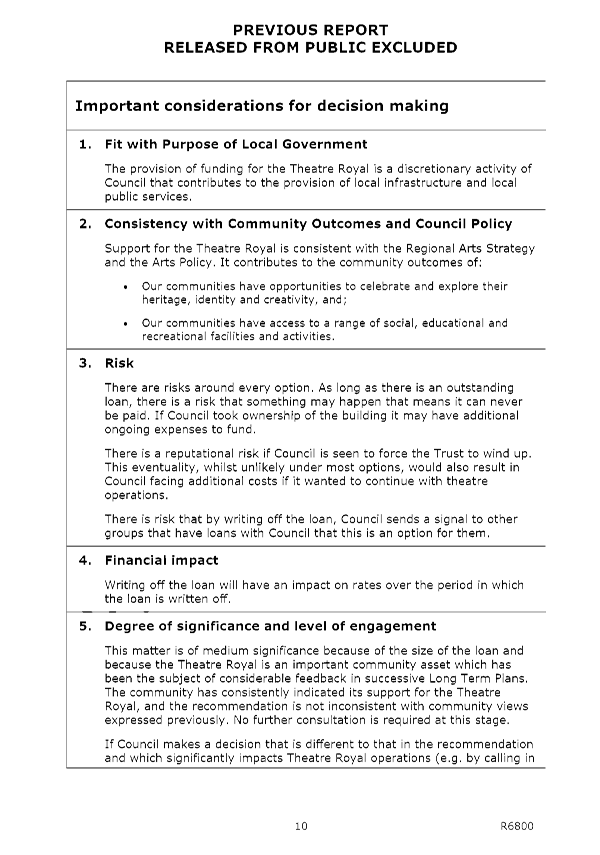

Important considerations for decision making

|

|

1. Fit

with Purpose of Local Government

The provision of funding for the Theatre Royal is a

discretionary activity of Council that contributes to the provision of local

infrastructure and local public services.

|

|

2. Consistency

with Community Outcomes and Council Policy

Support for the Theatre Royal is consistent with the

Regional Arts Strategy and the Arts Policy. It contributes to the community

outcomes of:

· Our communities have opportunities to

celebrate and explore their heritage, identity and creativity, and;

· Our communities have access to a range of

social, educational and recreational facilities and activities.

|

|

3. Risk

There are risks around every option. As long as

there is an outstanding loan, there is a risk that something may happen that

means it will not be paid. If Council took ownership of the building it may

have additional ongoing expenses to fund.

There is a reputational risk if Council is seen to

force the Trust to wind up. This eventuality, whilst unlikely under most

options, would also result in Council facing additional costs if it wanted to

continue with theatre operations.

There is risk that by writing off the loan, Council

sends a signal to other groups that have loans with Council that this is an

option for them.

|

|

4. Financial

impact

Writing off the loan will have an impact on rates

over the period in which the loan is written off.

|

|

5. Degree

of significance and level of engagement

This matter is of medium significance because of the

size of the loan and because the Theatre Royal is an important community

asset which has been the subject of considerable feedback in successive Long

Term Plans. The community has consistently indicated its support for the

Theatre Royal, and the recommendation is not inconsistent with community

views expressed previously. No further consultation is required at this

stage.

If Council makes a decision that is different to

that in the recommendation and which significantly impacts Theatre Royal

operations (e.g. by calling in the loan) or Council debt (e.g. by writing off

the loan) then further public consultation may be required.

|

|

6. Inclusion

of Māori in the decision making process

Māori have not been specifically consulted on

in the development of this report.

|

|

7. Delegations

The Audit Risk and Finance Subcommittee has the

responsibility for considering Audit processes and management of financial

risks. The Subcommittee has the power to make a recommendation to Council on

this matter.

|

Item

8: Theatre Royal Loan: Attachment 1

Item

8: Theatre Royal Loan: Attachment 2

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

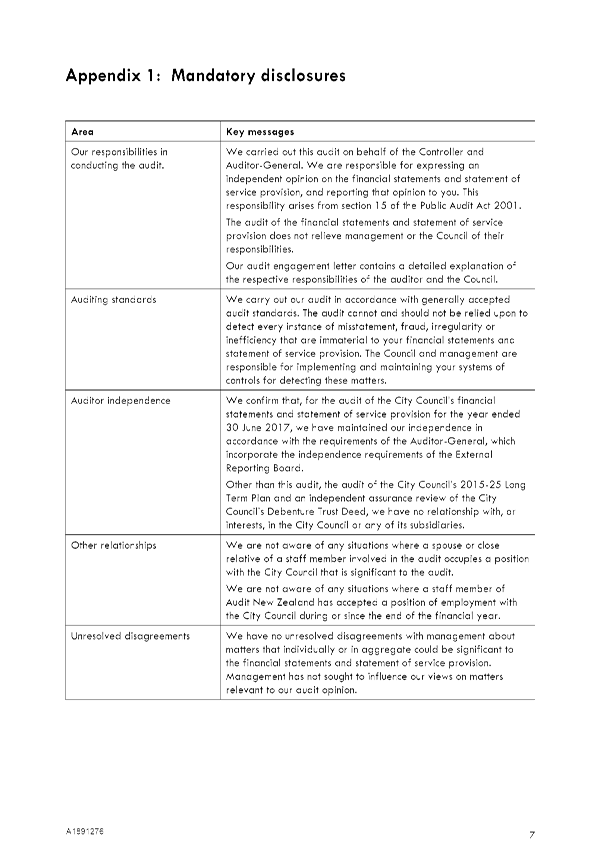

REPORT R8222

Audit

NZ - Letter to the Council on the audit for year ending 30 June 2017

1. Purpose

of Report

1.1 To

provide the letter to the Council on the audit for the year ending 30 June 2017

from Audit NZ.

2. Recommendation

1.

|

That the Audit, Risk and Finance Subcommittee

Receives the report Audit NZ -

Letter to the Council on the audit for year ending 30 June 2017 (R8222) and its attachment (A1891276).

|

3. Discussion

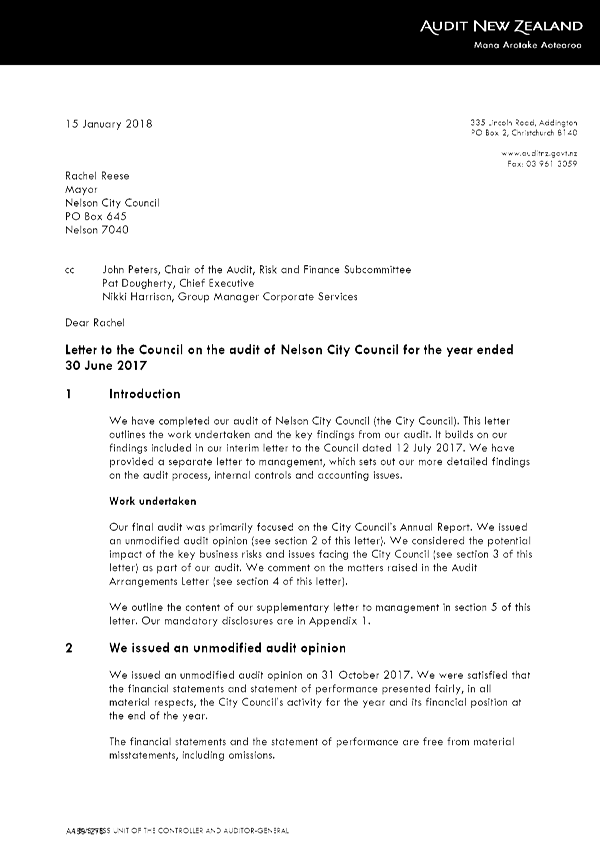

3.1 Audit

New Zealand (Audit NZ) issued an unmodified audit opinion on 31 October 2017

for the financial year ending 30 June 2017. This means that it was satisfied

that the financial statements fairly reflected Council's activities for the

year and its financial position at the end of the financial year.

3.2 After

the audit is completed, Audit NZ issues a management letter to Council

outlining the findings of the audit.

3.3 In

the letter to Council issued on 15 January 2018 (Attachment 1) Audit NZ comment

on the matters raised in the Audit arrangements letter including:

· rates

· regional landfill

business unit

· elected members

– remuneration and allowances

· asset management

plans

· legislative

reporting disclosures

· the separate audit

of the Debenture Trust Deed.

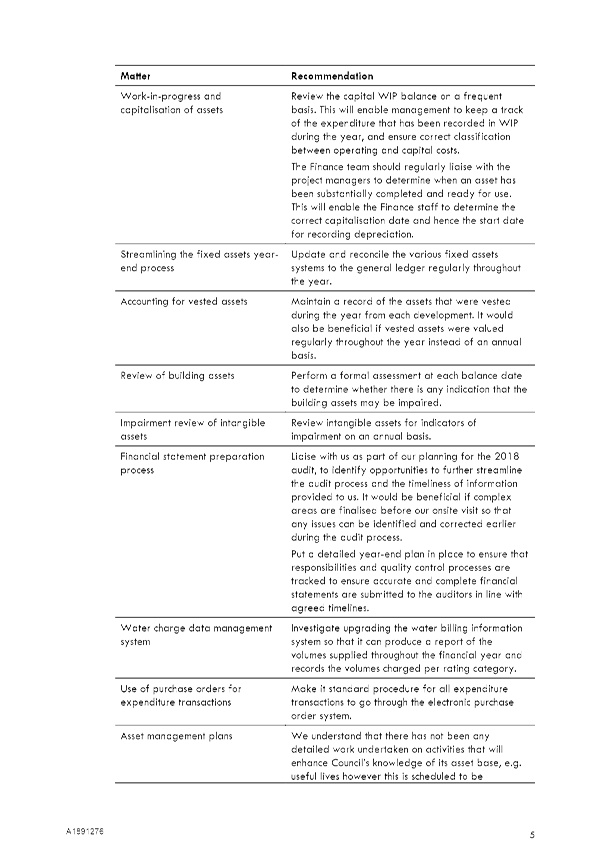

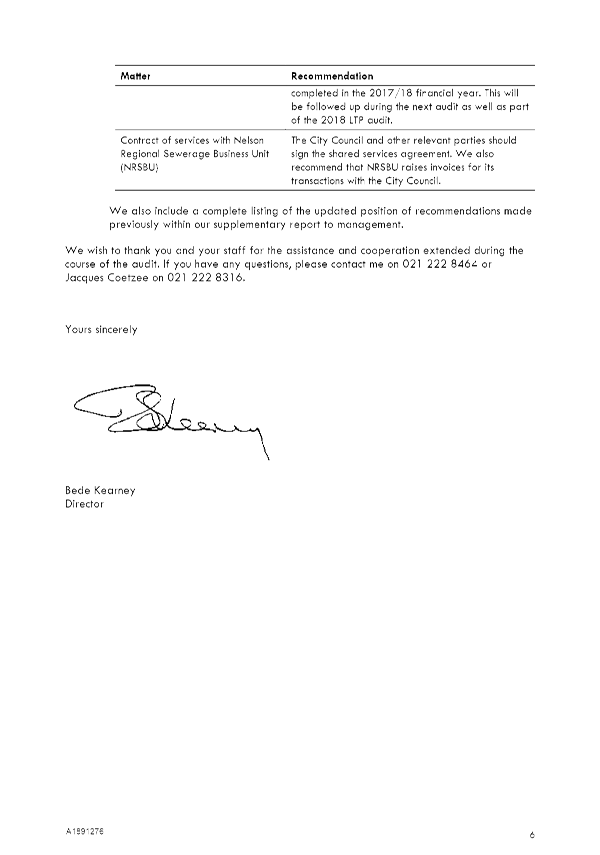

Supplementary

letter

3.4 Audit

NZ notes the matters raised in the supplementary letter to management in

Section 5 of the attached letter. The Chief Executive accepts these

comments and will address these matters prior to the 2017/18 Annual Report.

Nikki

Harrison

Group

Manager Corporate Services

Attachments

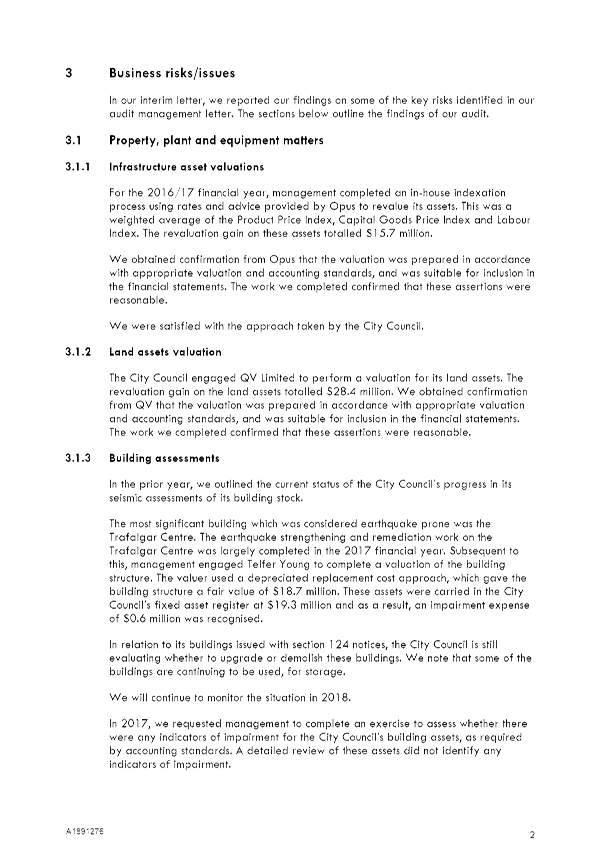

Attachment 1: A1891276 - Letter to the

Council on the audit of Nelson City Council for the year ⇩

Item

9: Audit NZ - Letter to the Council on the audit for year ending 30 June 2017:

Attachment 1

Item 10: Tendering

Processes - Follow Up Report

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

REPORT R8832

Tendering

Processes - Follow Up Report

1. Purpose

of Report

1.1 To

provide the subcommittee with the follow up external report requested at the

Governance Committee on 9 March 2017.

1.2 To

provide the subcommittee with assurance that the recommendations, resulting

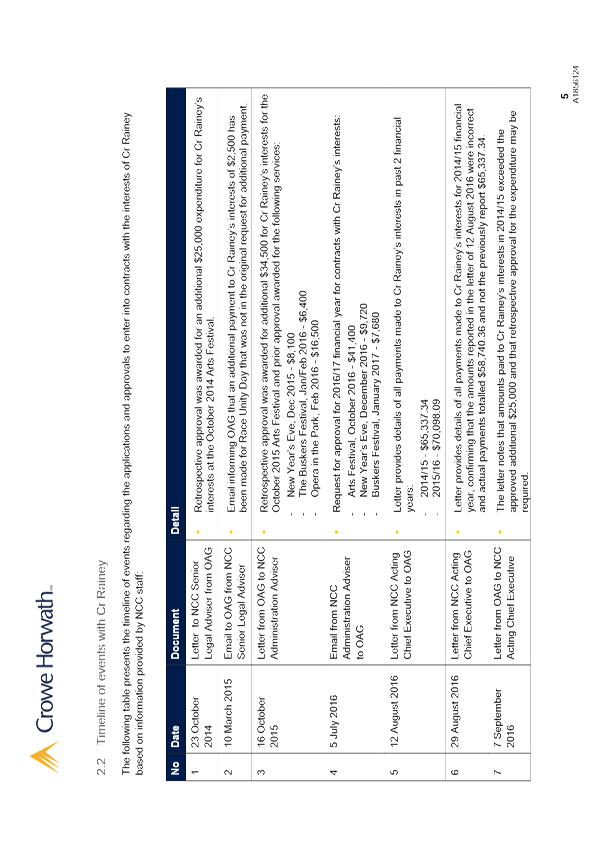

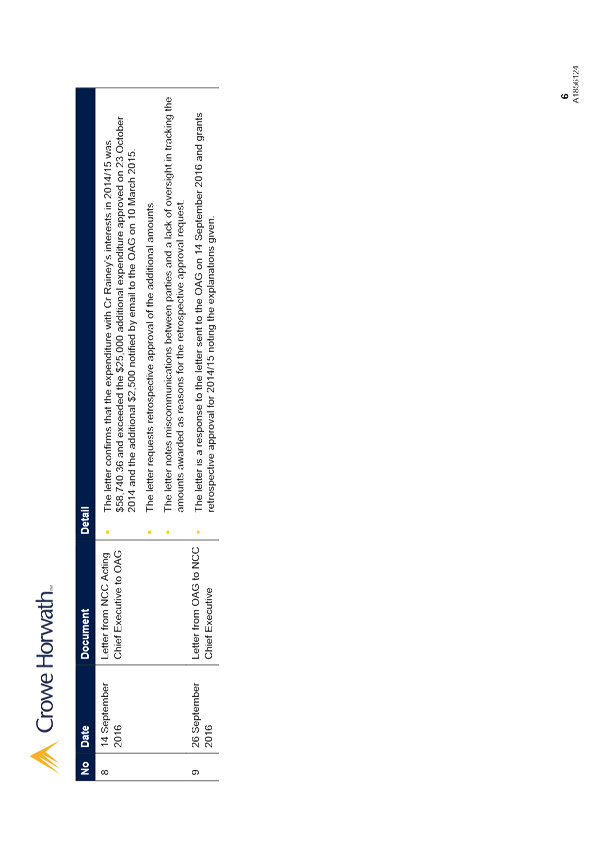

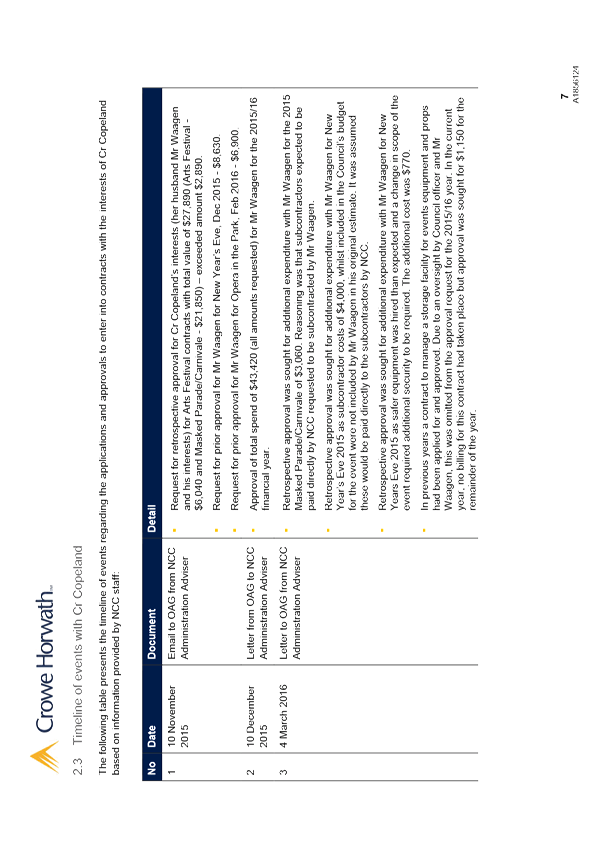

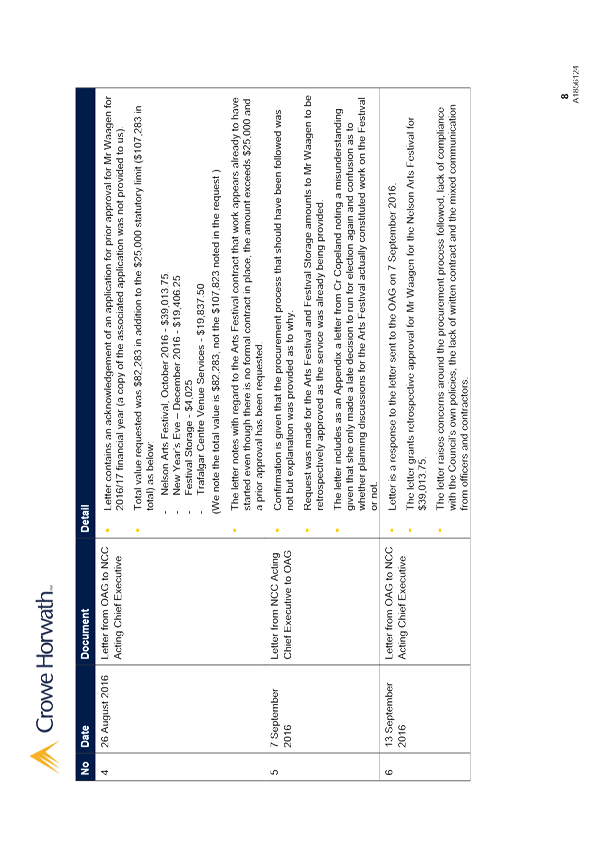

from the 2016 Crowe Horwath audit relating to Members’ Interests, have

been actioned.

2. Summary

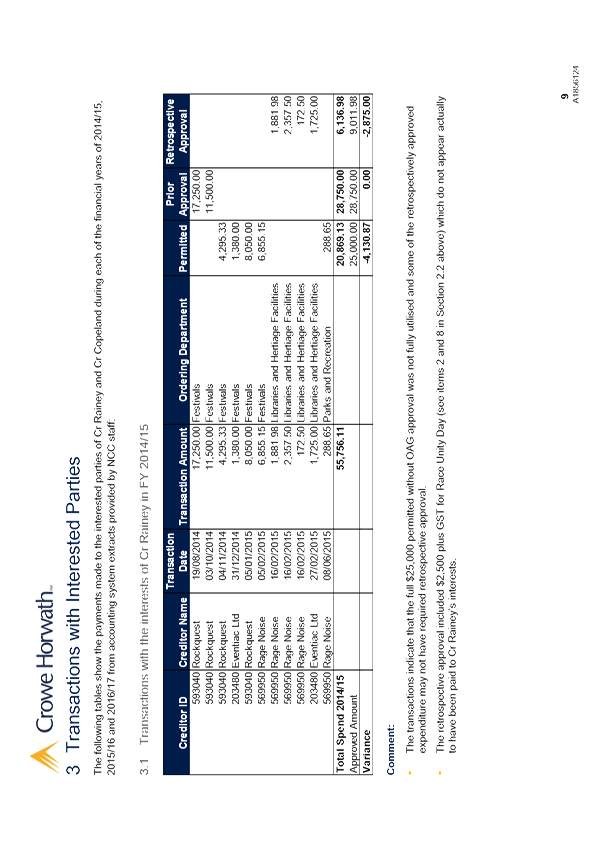

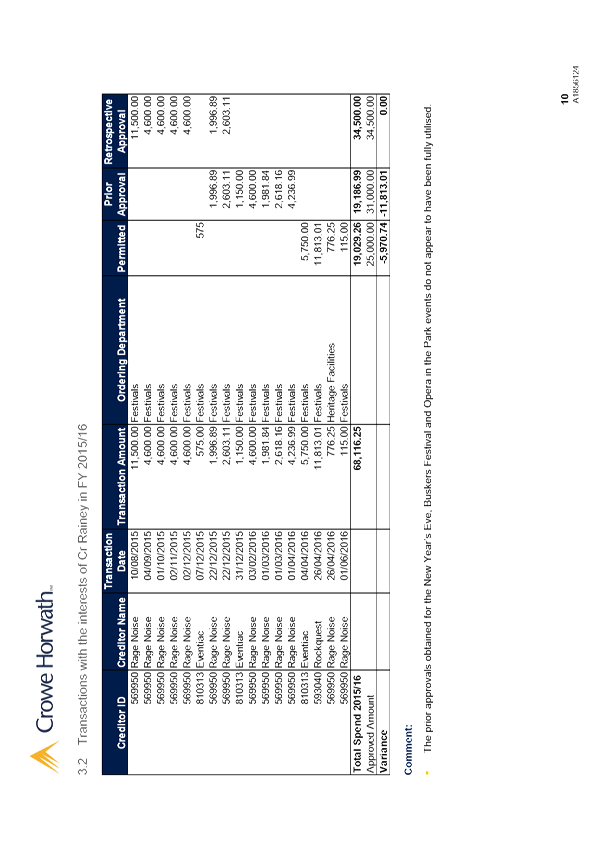

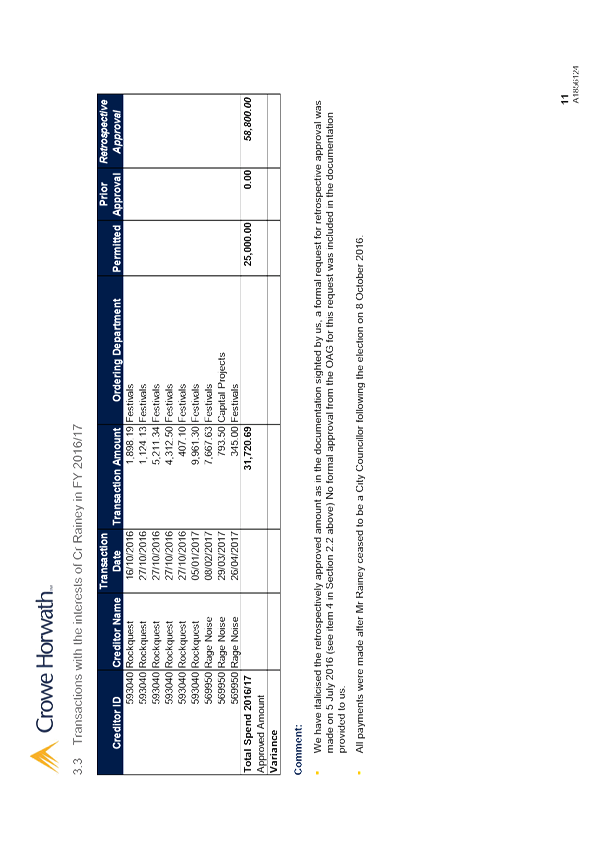

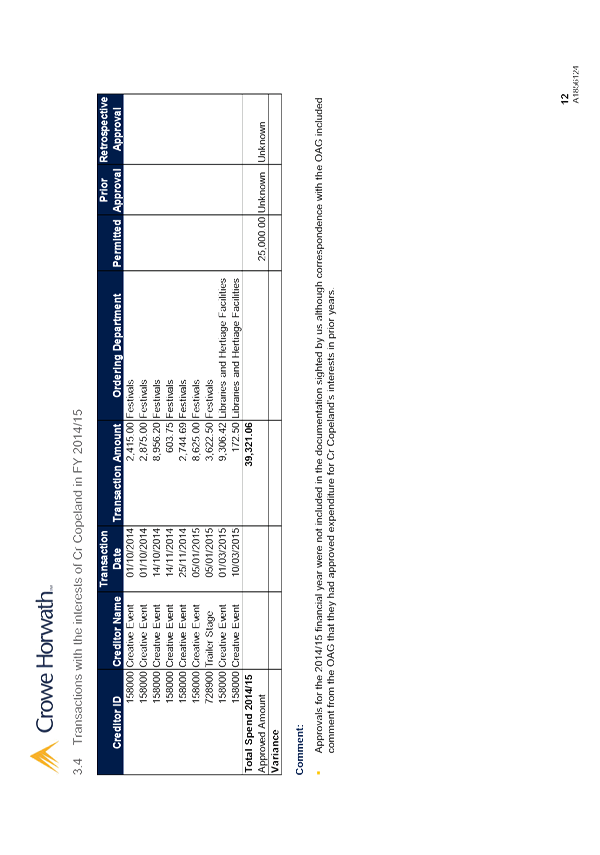

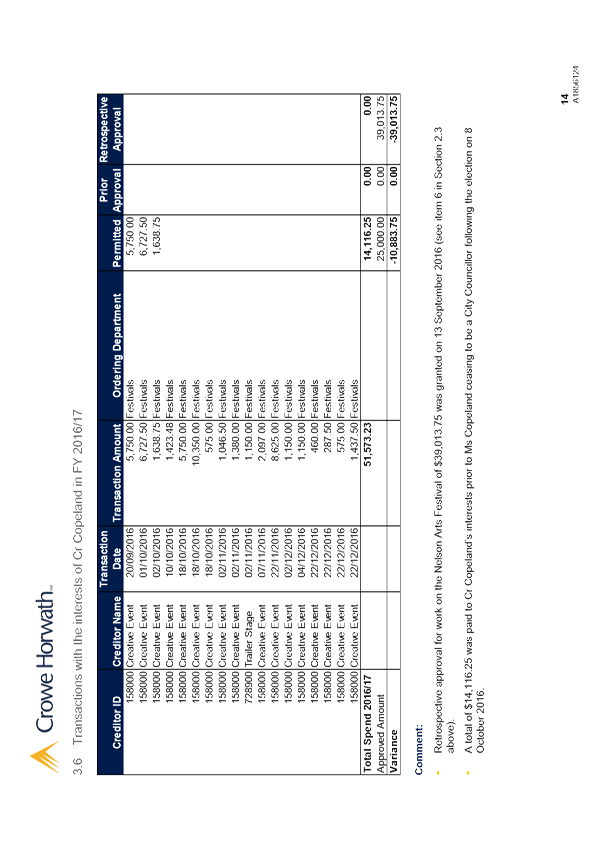

2.1 All

recommendations rated as high from the 2016 Crowe Horwath Report have been actioned.

2.2 Council

now has a full set of written procedures describing Members’ Interest

activities which must be followed for all levels of procurement.

3. Recommendation

1.

|

That the Audit, Risk and Finance

Subcommittee

Receives the report Tendering

Processes - Follow Up Report (R8832)

and its attachments (A1856124 and A1897197); and

Notes

that all recommendations rated as high from the 2016 Crowe Horwath Report

have been actioned.

|

4. Background

4.1 The

Governance Committee received advice of concerns raised by the Office of the

Auditor-General (OAG) at its 1 December 2016 meeting. This item was left to lie

on the table.

4.2 The

letter raised a number of concerns about Council’s processes for awarding

contracts for events and festivals, particularly as they related to approvals

for contracts involving previous councillors.

5. Discussion

5.1 A

further report was presented to the Governance Committee on 9 March 2017 on the

outcome of the external audit report undertaken by Crowe Horwath, in response

to concerns raised by the Office of the Auditor-General.

5.2 The

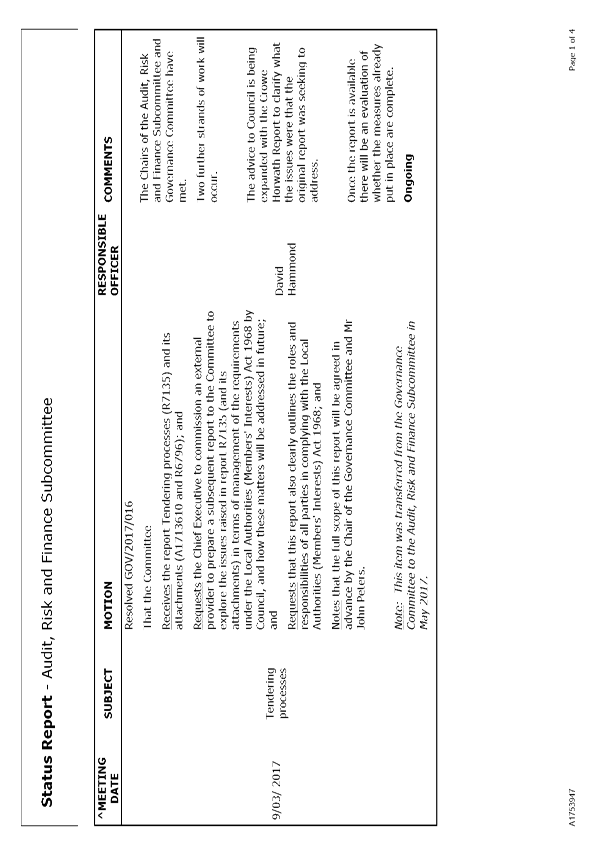

Governance Committee passed the following resolution:

That

the Governance Committee

Requests

the Chief Executive to commission an external provider to prepare a subsequent

report to the Committee to explore the issues raised in report R7135 (and its

attachments) in terms of management of the requirements under the Local

Authorities (Members' Interests) Act 1968 by Council, and how these matters

will be addressed in future; and

Requests

that this report also clearly outlines the roles and responsibilities of all

parties in complying with the Local Authorities (Members' Interests) Act 1968;

and

Notes

that the full scope of this report will be agreed in advance by the Chair of

the Governance Committee and Mr John Peters.

5.3 The

subsequent external report is included as Attachment 1. This report provides

additional information on the specific issues and timeline that occurred

between 2014 and 2016 relating to the approvals required from the Office of the

Auditor-General for entering into contracts with members.

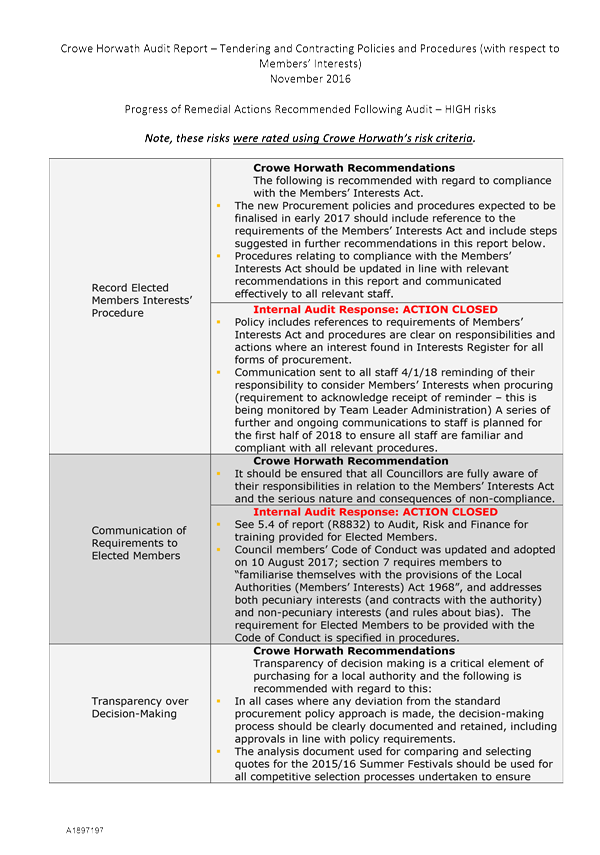

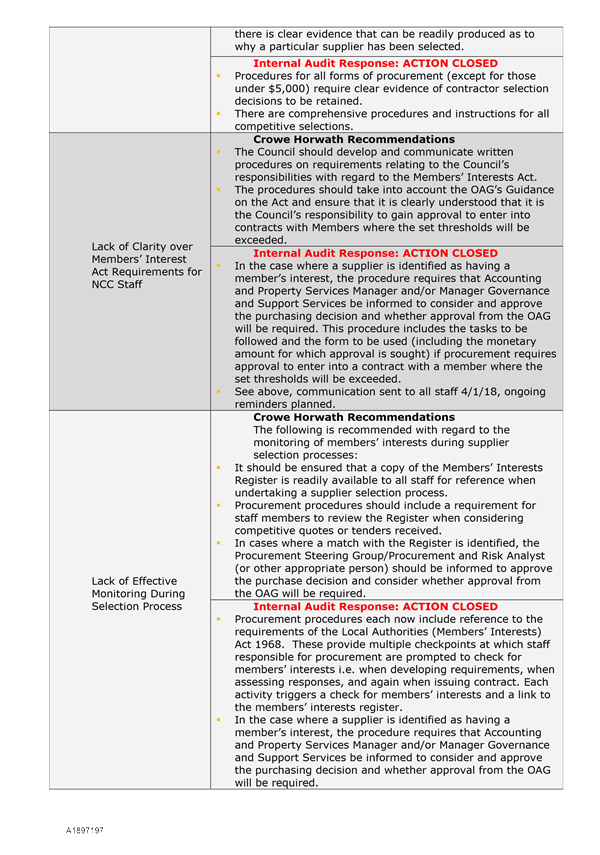

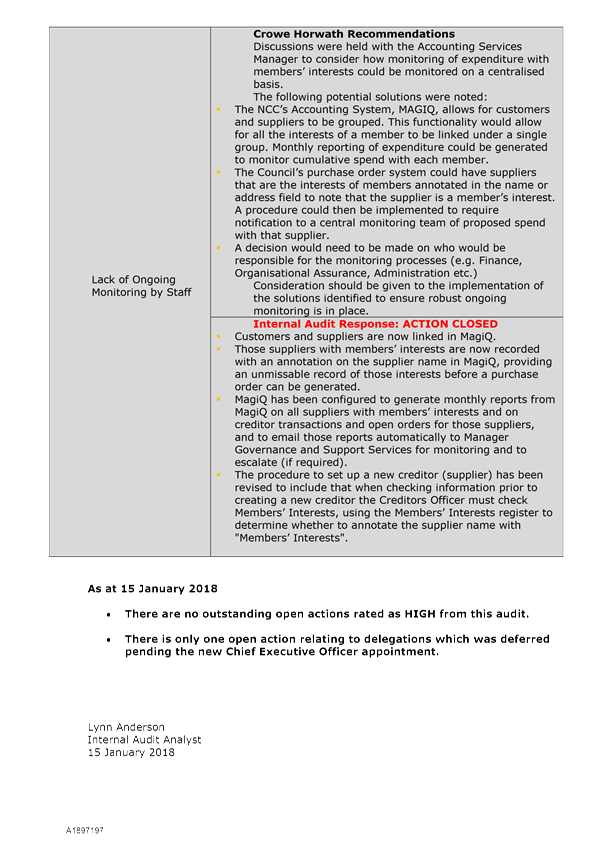

5.4 Members’

interests training was undertaken by Jonathon Salter from Simpson Grierson with

elected members on 30 November 2017 which clearly outlines the roles and

responsibilities of all parties.

5.5 A

progress report on the HIGH corrective actions is included as Attachment 2.

5.6 All

recommendations rated as high from the Crowe Horwath Report have been

actioned. There is one outstanding action item (rated medium) which

relates to delegations which was deferred pending the new Chief Executive

appointment.

5.7 Council

now has a full set of written procedures describing Members’ Interest activities

which must followed for all levels of procurement.

6. Options

6.1 The

subcommittee can receive the report; decline to receive the report; and/or ask

for further information.

7. Conclusion

7.1 The

Office of the Auditor-General expressed concern around Council’s

procurement, contract and tendering policies with particular reference to

festivals funded by Council.

7.2 An

audit of the activity was undertaken and a follow up external report was

requested. The follow up report is attached, along with progress on the

HIGH corrective actions.

Nikki

Harrison

Group

Manager Corporate Services

Attachments

Attachment 1: A1856124 - Tendering and

Contracting Policies - Nelson City Council prepared by Crowe Horwath ⇩

Attachment 2: A1897197

- Progress on High Corrective Actions from Crowe Horwath Report - Members'

Interests ⇩

|

Important considerations for decision making

|

|

1. Fit

with Purpose of Local Government

Ensuring robust processes for issuing contracts

allows cost-effective procurement of services.

|

|

2. Consistency

with Community Outcomes and Council Policy

Reviewing contract processes supports the community

outcome that our Council provides leadership.

|

|

3. Risk

There is limited risk from receiving this report,

noting that the recommendations from the external audit report have been

actioned by management.

|

|

4. Financial

impact

The costs of the follow up report and training were

met within existing budgets.

|

|

5. Degree

of significance and level of engagement

This matter is of low significance because it

relates to internal processes. No consultation is required.

|

|

6. Inclusion

of Māori in the decision making process

Maori have not been consulted on this matter.

|

|

7. Delegations

The Audit, Risk and Finance subcommittee has the

responsibility for monitoring of Council’s financial and service

performance.

|

Item

10: Tendering Processes - Follow Up Report: Attachment 1

Item

10: Tendering Processes - Follow Up Report: Attachment 2

Item 11: Audit NZ -

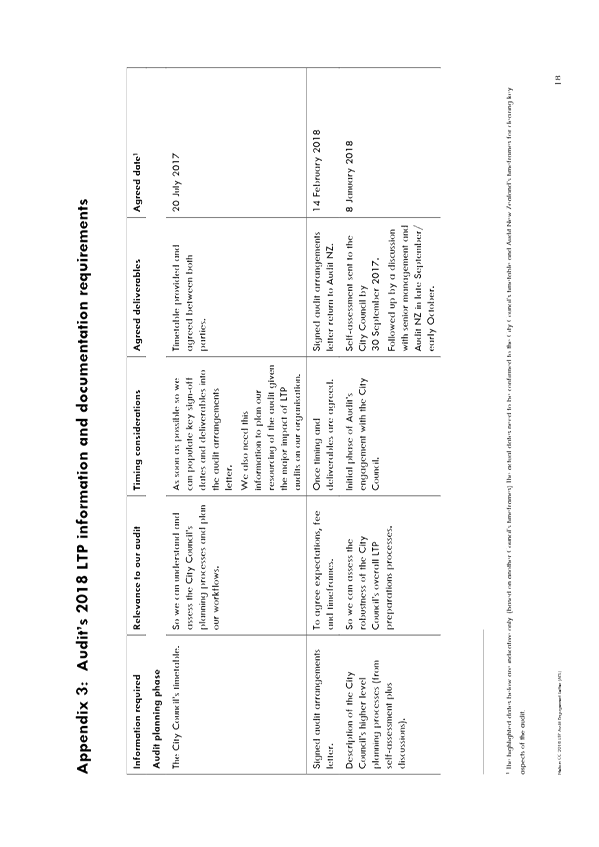

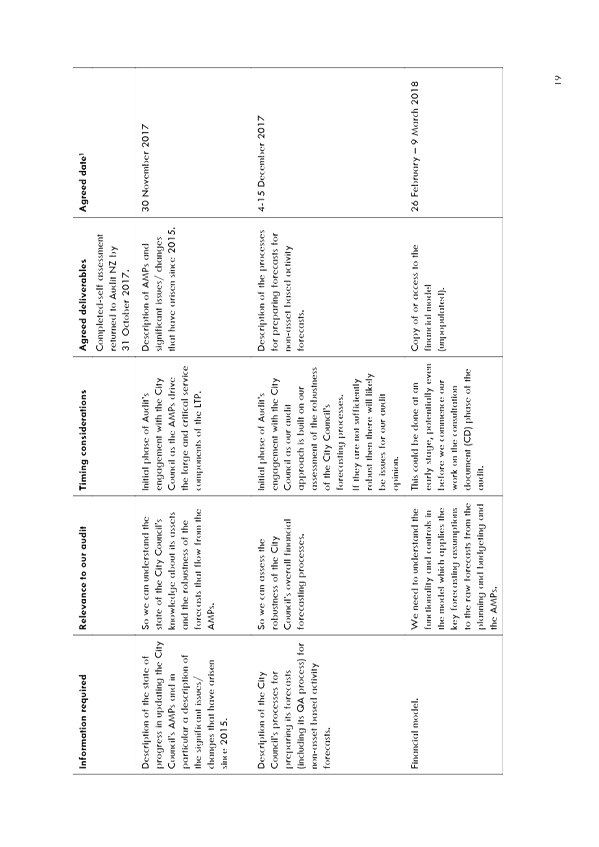

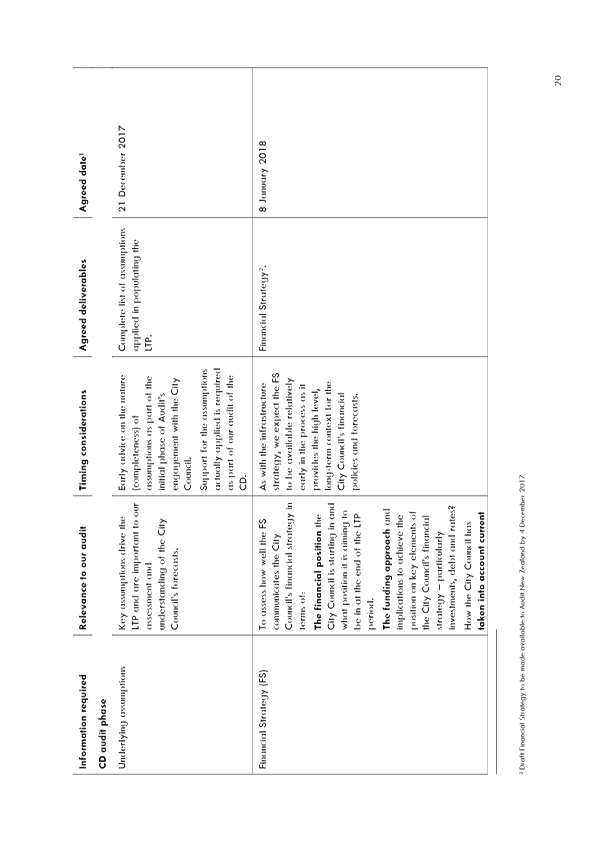

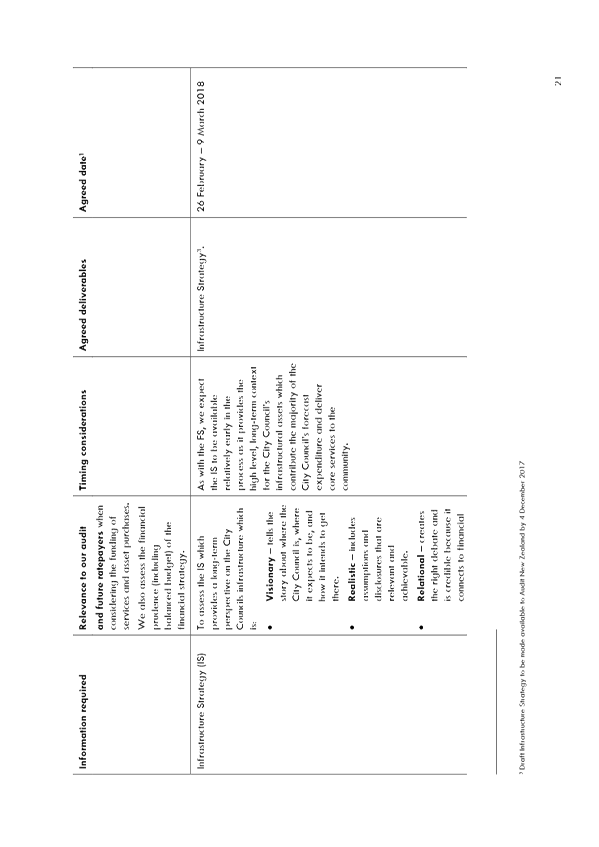

Audit Engagement Letter for the Long Term Plan 2018-28

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

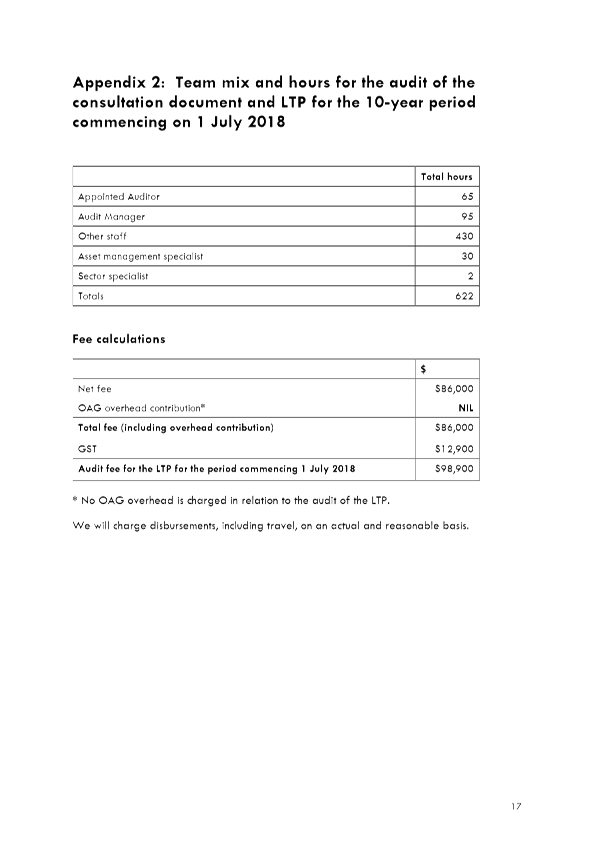

|

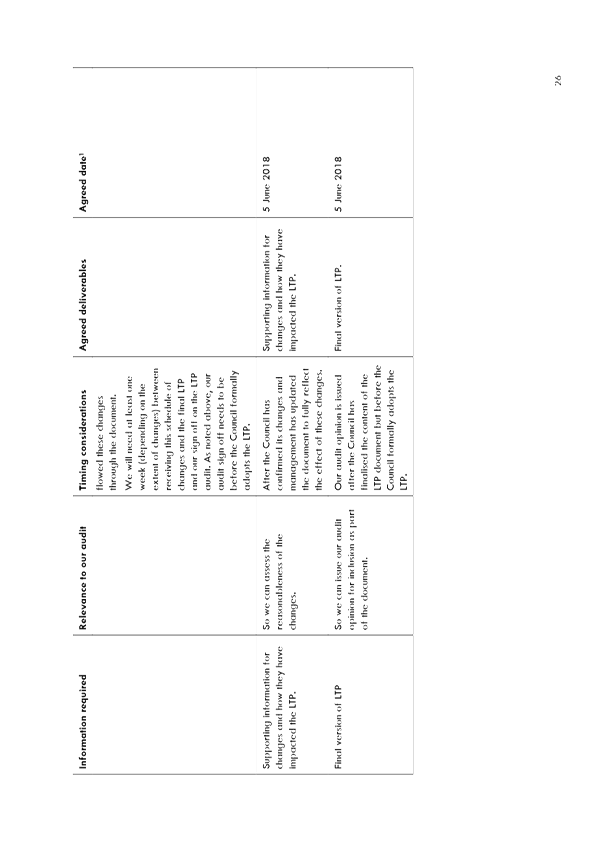

REPORT R8865

Audit

NZ - Audit Engagement Letter for the Long Term Plan 2018-28

1. Purpose

of Report

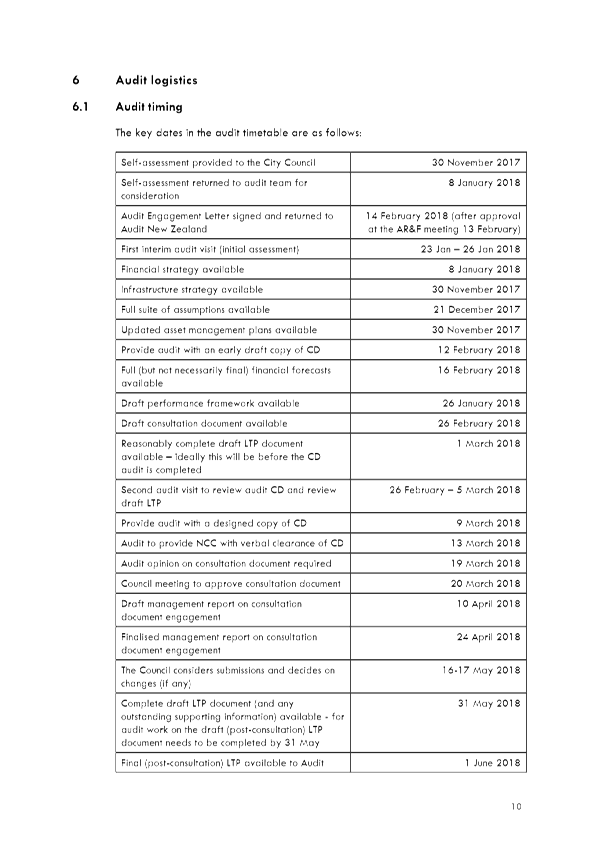

1.1 To provide the subcommittee with

the Audit Engagement Letter for the audit of the consultation document and Long

Term Plan 2018-28 and ask for any feedback before the letter is signed by the

Mayor.

2. Recommendation

1.

|

That the Audit, Risk and Finance

Subcommittee

Receives the report Audit NZ -

Audit Engagement Letter for the Long Term Plan 2018-28 (R8865) and its attachment (A1894901); and

Notes the subcommittee can provide

feedback on the Audit Engagement Letter to Audit NZ if required and that the

Mayor will sign the letter once the subcommittee’s feedback (if any)

has been incorporated.

|

3. Discussion

3.1 The Audit Engagement Letter

(Attachment 1) relates to the audit of the consultation document and LTP 2018 -

28.

3.2 The letter sets out the terms of

the audit engagement and the respective responsibilities of Council and Audit

New Zealand. The letter also outlines the audit scope and objectives, the

approach taken to complete the audit, the areas of audit emphasis, the audit

logistics and the professional fees.

3.3 The letter is to be signed by the

Mayor to confirm that the details of the audit match Council’s

understanding of the arrangements.

4. Options

The options available to the

subcommittee are to provide feedback to Audit NZ prior to the letters being

signed, or not to provide feedback.

Michelle

Joubert

Executive

Officer

Attachments

Attachment 1: A1894801 - Audit

Engagement Letter ⇩

|

Important considerations for decision making

|

|

1. Fit

with Purpose of Local Government

Section 93C(4) of the Local Government Act 2002

requires an auditor’s report on the consultation document and section

94 requires a separate opinion on the Long Term Plan.

|

|

2. Consistency

with Community Outcomes and Council Policy

This contributes to all the community outcomes as

the Long Term Plan covers all the work of Council.

|

|

3. Risk

The recommendations contained in this report pose no

material risk.

|

|

4. Financial

impact

There is no financial impact from the

recommendations contained in this report.

|

|

5. Degree

of significance and level of engagement

This matter is of low significance as it does not

affect the level of service provided by Council or the way in which services

are delivered. Therefore, no consultation has been undertaken.

|

|

6. Inclusion

of Māori in the decision making process

Māori have not been consulted on this report.

|

|

7. Delegations

The Audit, Risk and Finance Subcommittee has

responsibility for audit processes and management of financial risks.

|

Item

11: Audit NZ - Audit Engagement Letter for the Long Term Plan 2018-28:

Attachment 1

Item 12: Corporate

Report to 31 December 2017

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

REPORT R8857

Corporate

Report to 31 December 2017

1. Purpose

of Report

1.1 To

inform the members of the Subcommittee of the financial results

of activities for the six months ending 31 December 2017, compared to the

approved operating budget, and to highlight and explain any permanent and

material variations.

2. Recommendation

|

That the Audit, Risk and Finance

Subcommittee

Receives the report Corporate

Report to 31 December 2017 (R8857)

and its attachments (A1903395 and A1904902).

|

3. Background

3.1 The financial reporting focuses on the six month performance

compared with the year to date approved operating budget.

3.2 Unless

otherwise indicated, all measures are against approved operating budget, which

is 2017/18 Annual Plan budget plus any carry forwards, plus or minus any other

additions or changes as approved by Council throughout the year.

3.3 Officers have assessed budgets and applied a range of phasing

mechanisms to reflect the timing of anticipated actual income and expenditure.

4. Discussion

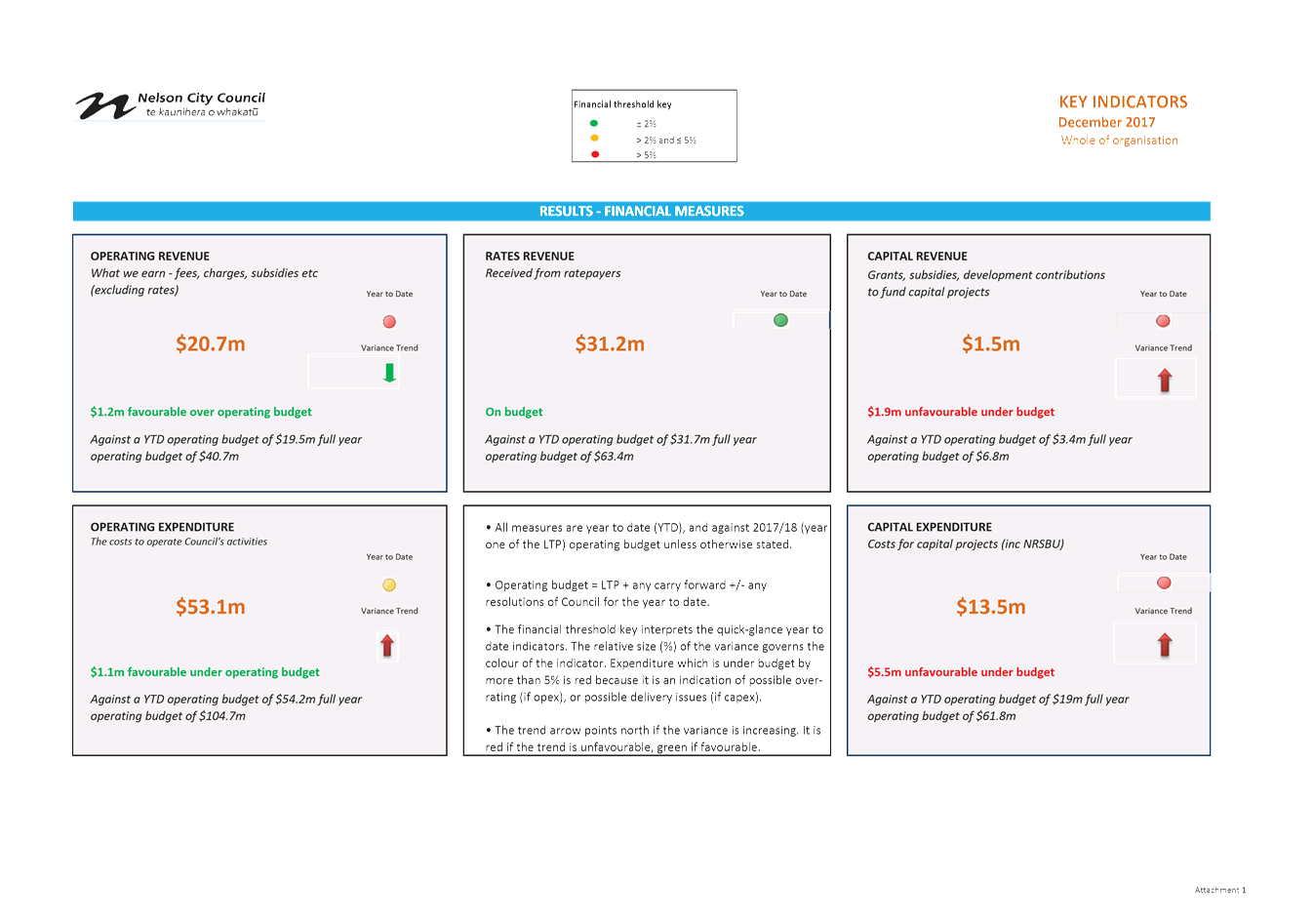

4.1 For the six months ending 31 December 2017, the activity

surplus/deficits are $3.3 million favourable to budget.

4.2 Financial information provided in Attachment 1 to this report

includes:

4.2.1 A financial measures dashboard with information on rates revenue,

operating revenue and expenditure, and capital revenue and expenditure. The

arrow icon in each applicable measure indicates whether the variance is

increasing or decreasing and whether that trend is favourable or unfavourable

(green or red).

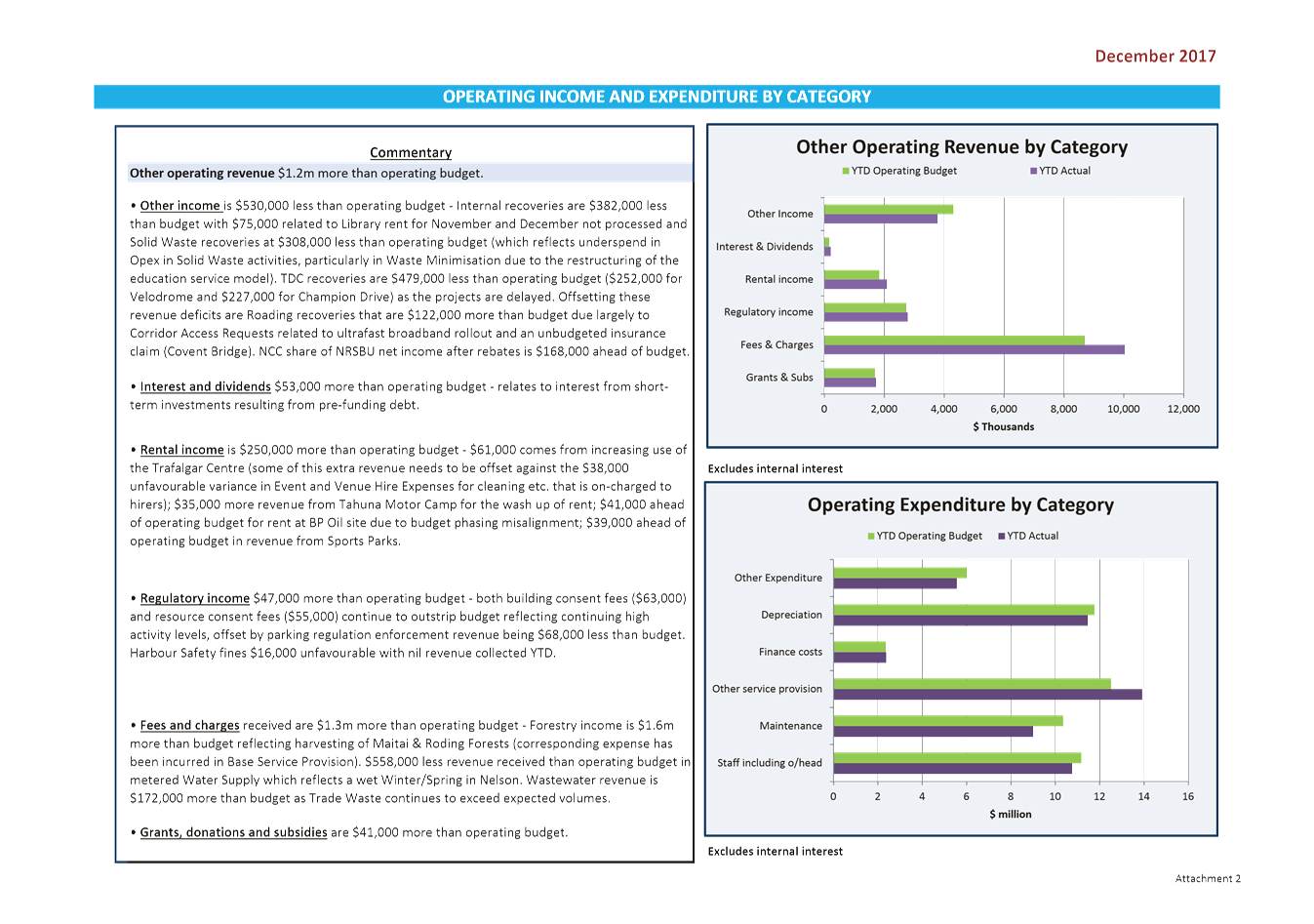

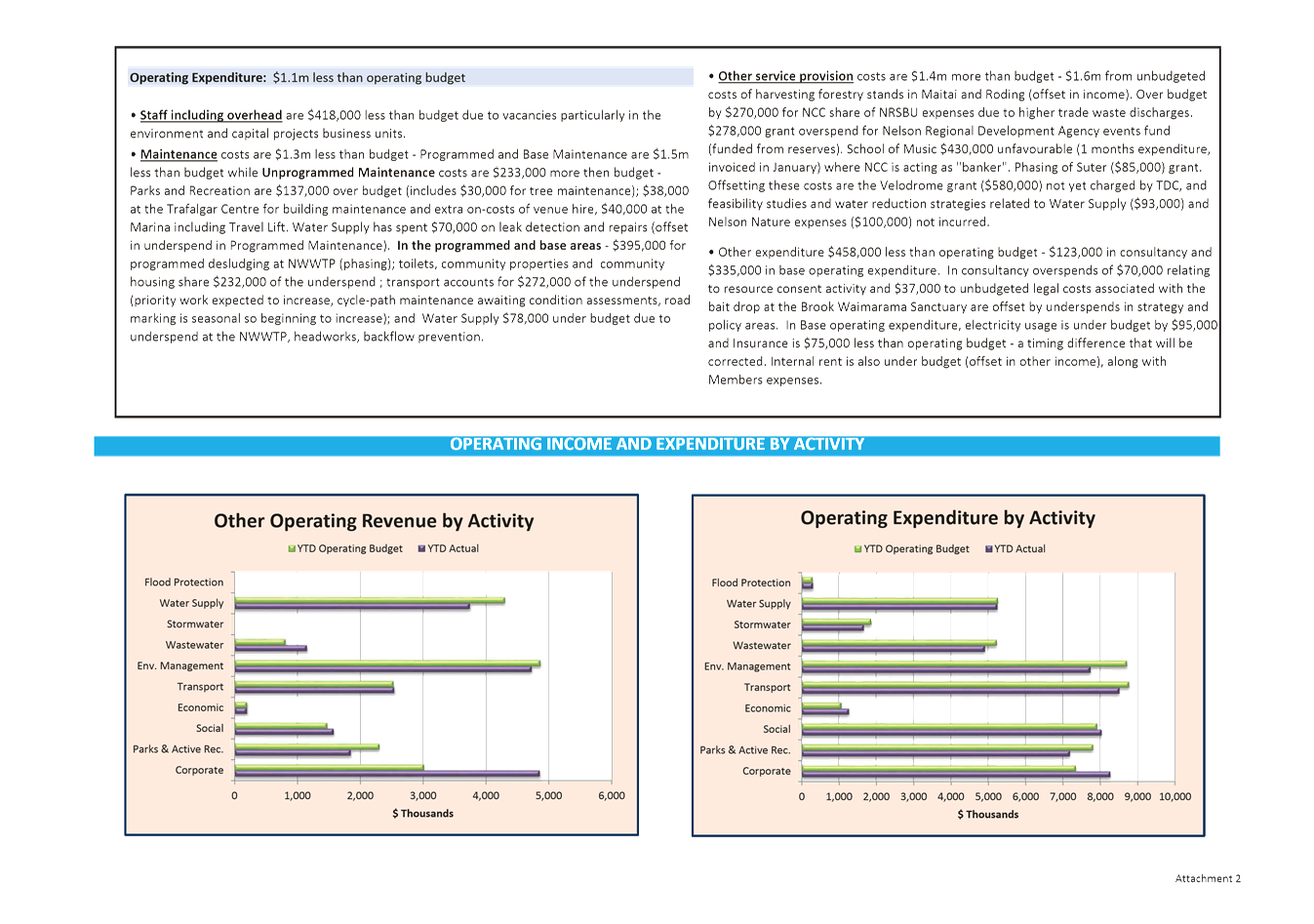

4.2.2 A grouping of more detailed graphs and commentary for operating

income and expenditure. The first set of charts and commentary is by category

(as in the annual report) and highlights significant permanent differences and

items of interest. Variances due to timing will not be itemised unless they

become permanent. The second set of charts is by activity.

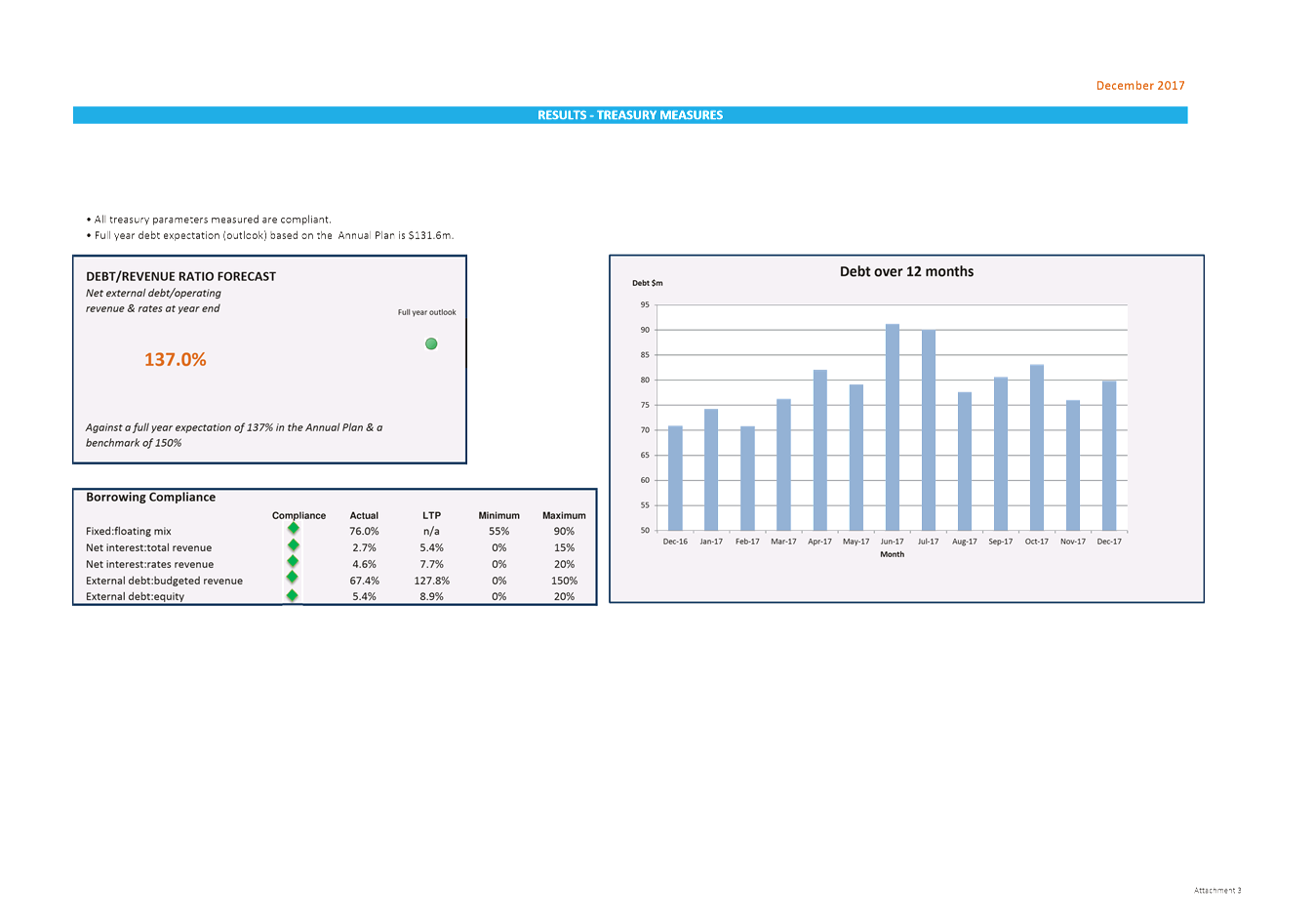

4.2.3 A treasury measures dashboard with a compliance table (green =

compliant), a forecast of the debt/revenue ratio for the year where available,

and a graph showing debt levels over a rolling 13 month period.

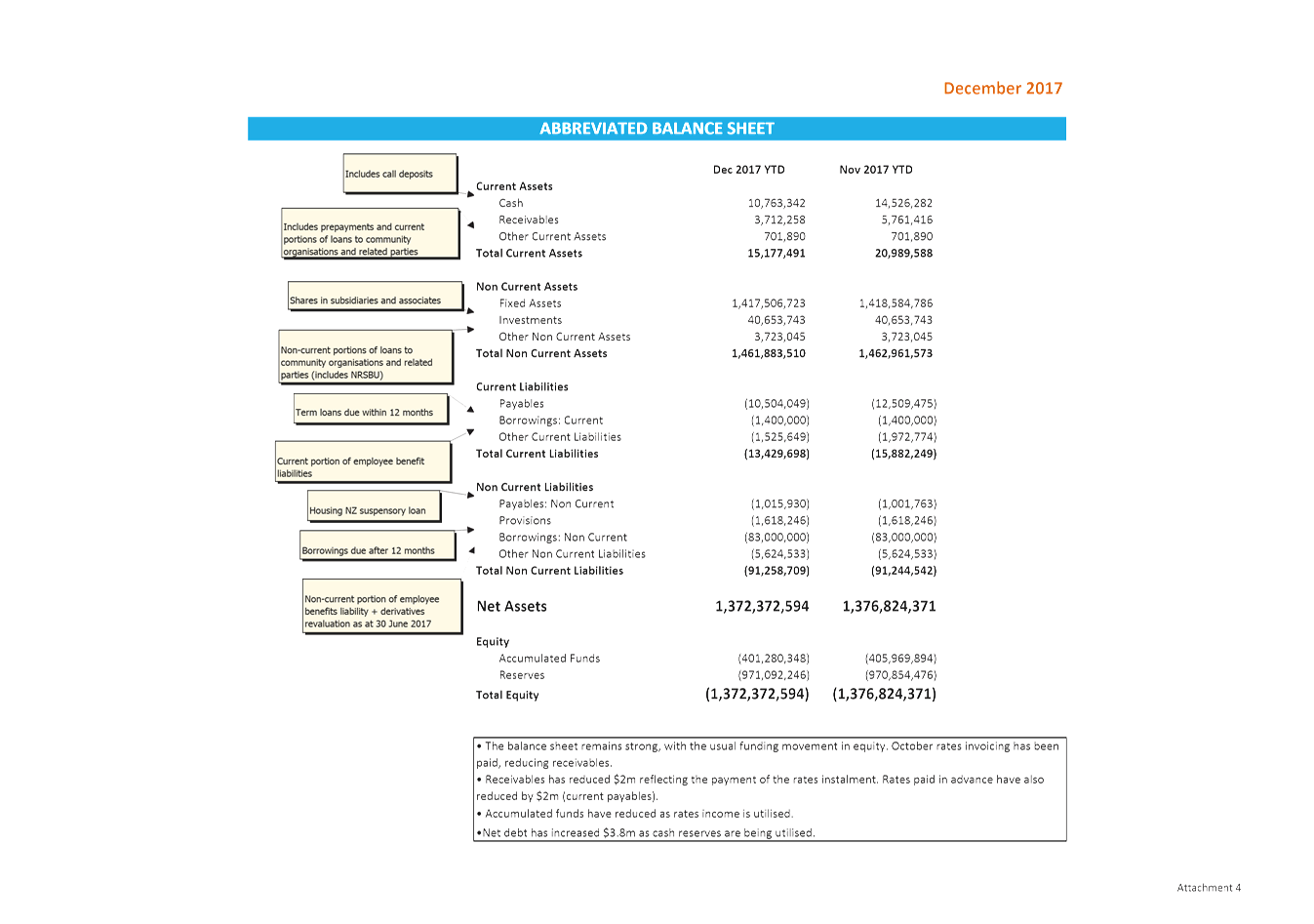

4.2.4 High level balance sheet. This does not include any consolidations.

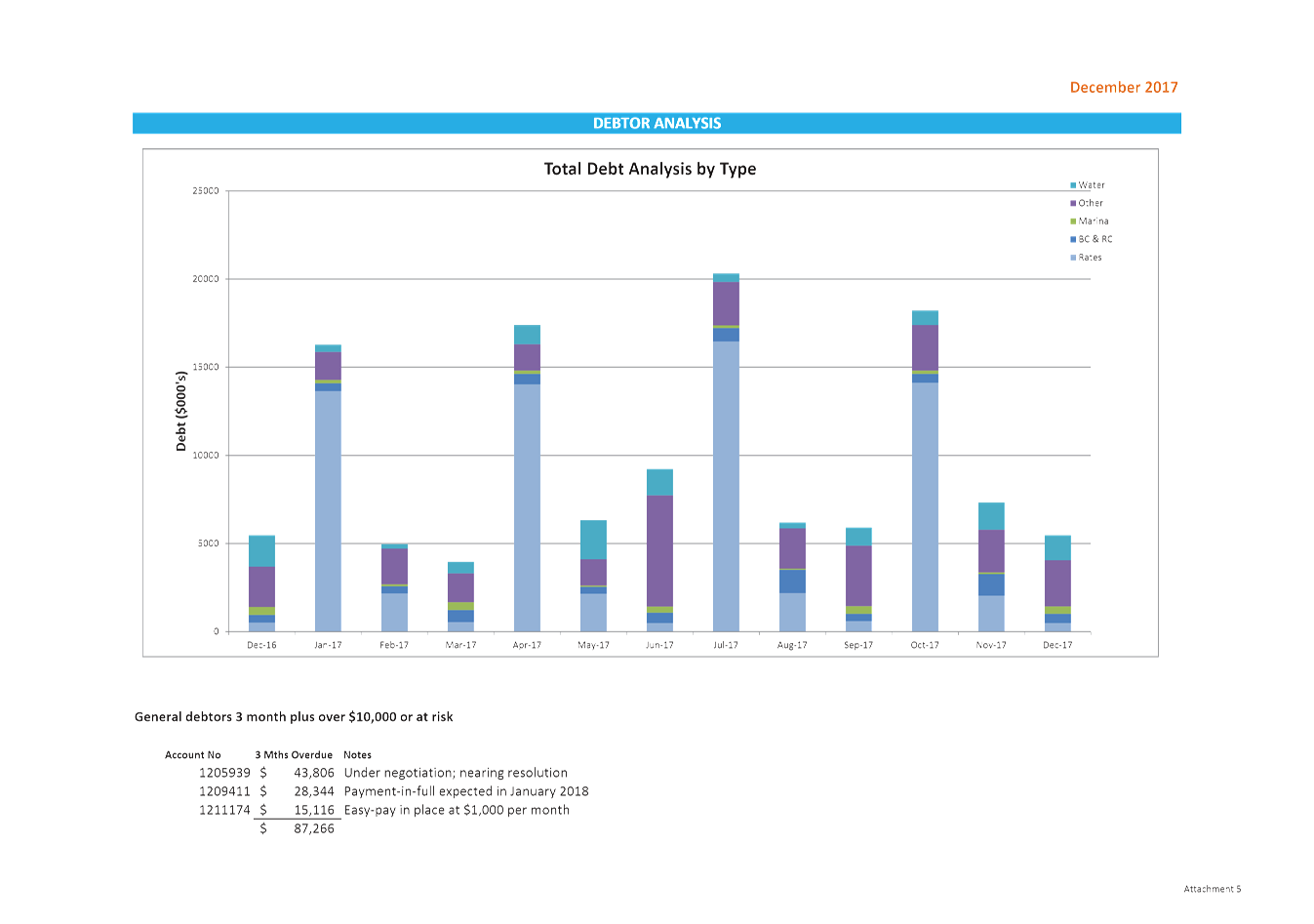

4.2.5 A debtor analysis graph over 12 months, clearly showing outstanding

debt levels and patterns for major debt types along with a summary of general

debtors > 3 months and over $10,000 and other debtors at risk.

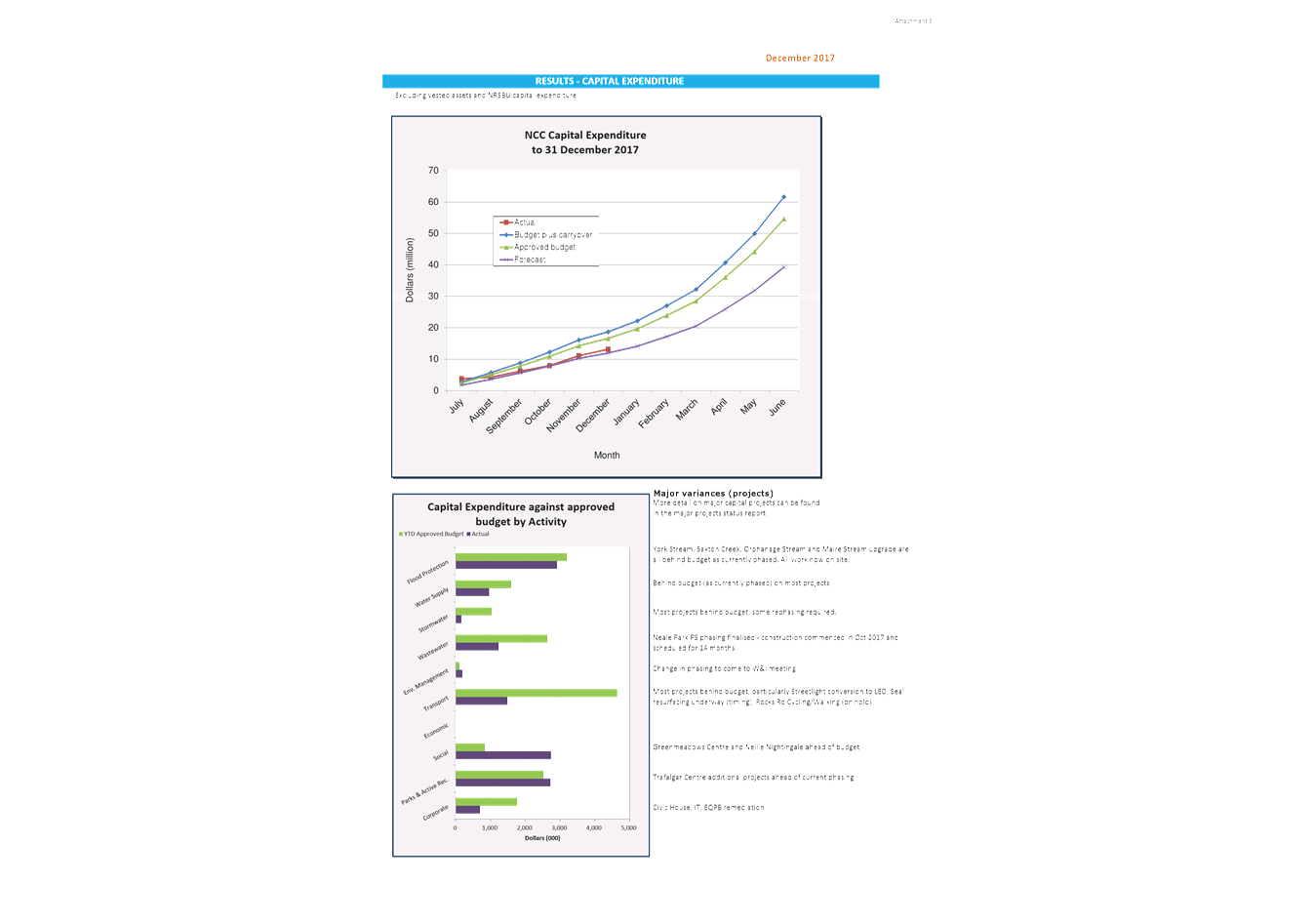

4.2.6 Two capital expenditure graphs – The line graph records actual

expenditure against budget plus carryover (the initial budget), approved budget

(as amended by subsequent Council decisions), and forecast (current

understanding of most likely outcome). The bar graph records year to date

expenditure against approved operating budget by activity.

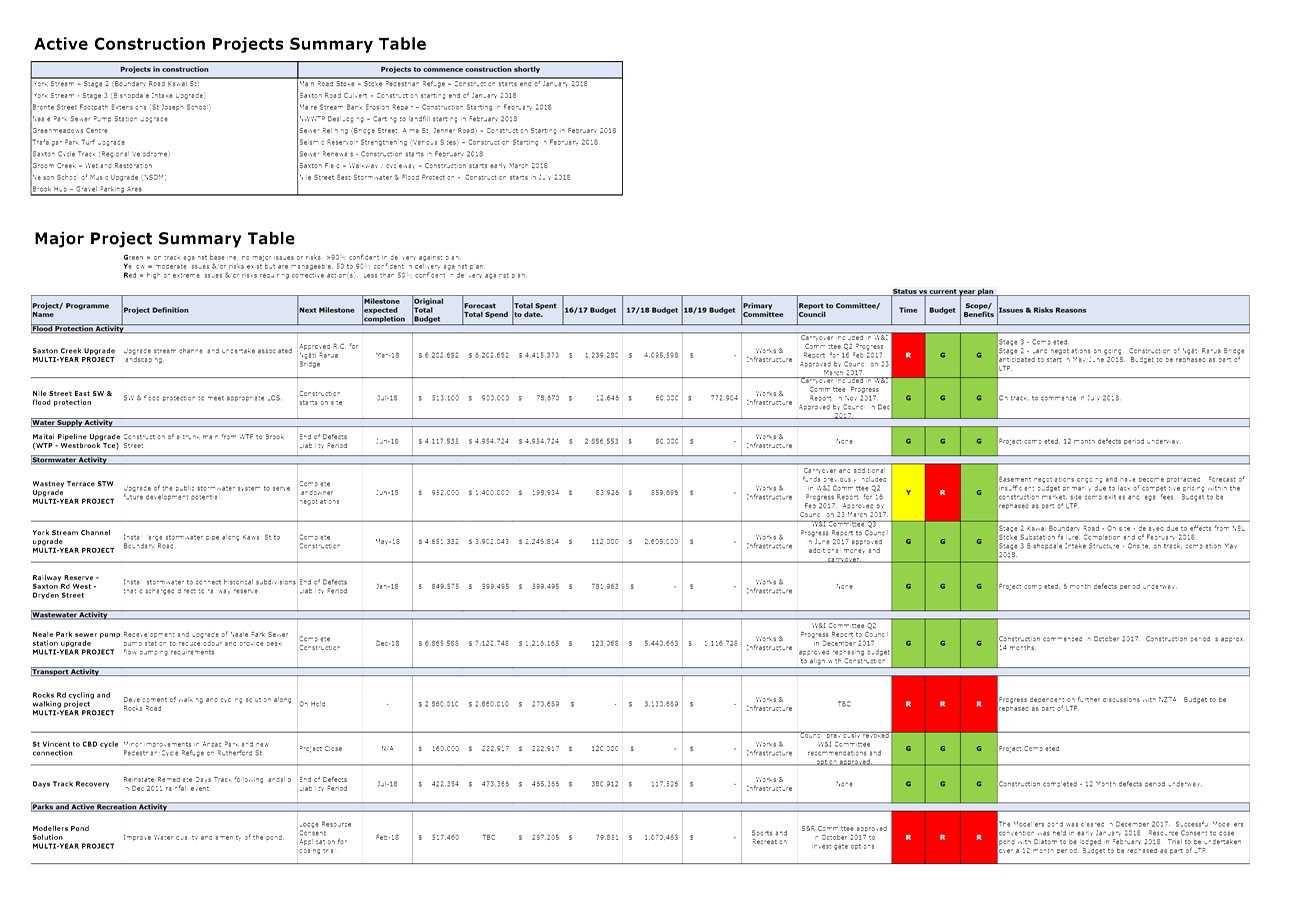

4.2.7 A major projects summary including milestones, status, issues and

risks.

4.3 Capital expenditure is $5.4 million under approved budget and $1m

more than current forecast for the Long Term Plan 2018-28 presented to Council

workshops in late January (including vested assets and NRSBU capital).

Tracey Hughes

Senior

Accountant

Attachments

Attachment 1: A1904902 Financial

information ⇩

Attachment 2: A1903395

Major Projects summary ⇩

Item

12: Corporate Report to 31 December 2017: Attachment 1

Item

12: Corporate Report to 31 December 2017: Attachment 2

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

REPORT R8869

Internal

Audit Quarterly Report to 31 December 2017

1. Purpose

of Report

1.1 To

update the Audit, Risk and Finance Subcommittee on the internal audit activity

for the quarter to 31 December 2017.

2. Recommendation

|

That the Audit, Risk and Finance Subcommittee

Receives the report Internal

Audit Quarterly Report to 31 December 2017 (R8869) and its attachment (A1894689).

|

3. Background

3.1 The

Internal Audit Charter was approved by Council on 15 October 2015.

3.2 Under

the Internal Audit Charter, the Audit, Risk and Finance Subcommittee requires a

periodic update on the progress of internal audit activities relative to any

current Internal Audit Plan approved by Council, and to be informed of any

significant risk exposures and control issues identified from internal audits

completed.

3.3 The

current Annual Audit Plan period is to 30 June 2018 which was approved by

Council on 9 November 2017.

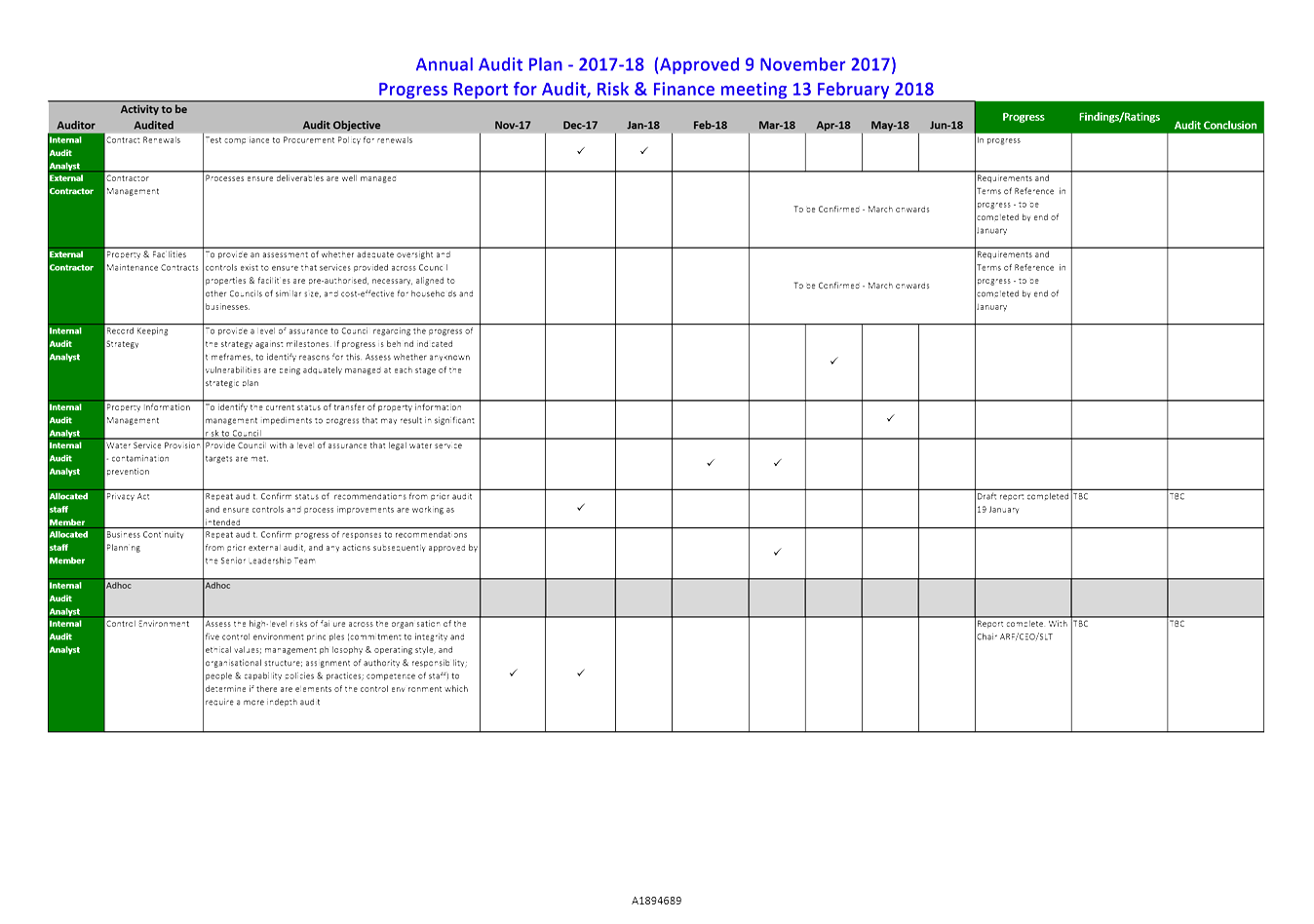

4. Progress Against

Annual Audit Plan During the Quarter

4.1 The

attached report (A1894689) shows the progress against all audits planned for

the financial year to 30 June 2018.

4.2 In

addition to these audits, during the quarter a request was received to perform

an additional minor compliance audit for the Building business unit. This was

agreed to as it is expected to be of short duration (one day) and will be

undertaken by an officer who performed a similar audit last year.

4.3 There

are currently no concerns with meeting the resourcing requirements of the Audit

Plan.

5. Recommendation

Options

5.1 The

acceptance of the recommendation to receive the Internal Audit Quarterly Report

to 31 December 2017 outlining internal audit’s activity demonstrates

Council’s commitment to improving controls and practices that ensure the

prudent, effective and efficient management of Council resources. No advantage

could be identified from not receiving this report.

Lynn

Anderson

Internal

Audit Analyst

Attachments

Attachment 1: A1894689 - Internal Audit

Quarterly Progress Report to 31 December 2017 ⇩

Item

13: Internal Audit Quarterly Report to 31 December 2017: Attachment 1

Item 14: Key

Organisational Risks Calendar 2017 - 4th Quarterly Report

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

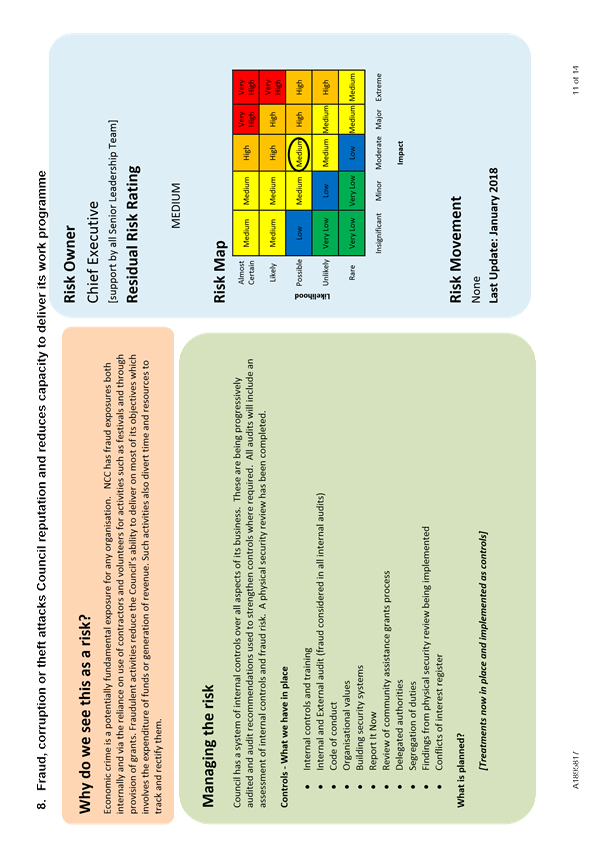

REPORT R8797

Key

Organisational Risks Calendar 2017 - 4th Quarterly Report

1. Purpose

of Report

1.1 To

update the Subcommittee on progress with identifying and managing key risks to

the organisation’s objectives. The report is intended to assist the

governance role of the Subcommittee in overseeing the organisation’s risk

management.

2. Recommendation

|

That the Audit, Risk and Finance

Subcommittee

Receives the report Key

Organisational Risks Calendar 2017 - 4th Quarterly Report (R8797) and its attachment A1895817.

|

3. Background

3.1 At

its meeting on 14 November 2017, the Audit Risk and Finance Subcommittee

received and considered the previous quarterly report on key organisational

risks to Council’s objectives. In doing so it specifically considered a

number of matters including the level of risk to the organisation’s

overall objectives caused by the difficulty in maintaining required levels of

staff expertise across the Council’s many functions.

3.2 The

Subcommittee requested a separate report on this matter which is on the agenda

for this meeting. Accordingly no change has been made to the relevant page in

the attached key risk summary.

3.3 As

with previous reports, this report is based on the organisation’s

existing business model – that is, as far as possible on risk management

processes within each business unit. While most business units have reasonably

well established risk management processes, some catch up for new units (e.g.

City Development) and for newer senior staff and managers is still in progress.

There is therefore still an element of estimation from Organisational Assurance

observations and conversations in the attached.

4. Key

risk reporting

4.1 The

process of managing risks is forward looking. This involves identifying,

assessing and acting on risks. Risks are defined by events which may happen and

may in future affect the achievement of Council objectives. To estimate the

consequence (how big an impact) and likelihood (how certain or uncertain), we

use information about events which have previously affected our objectives.

4.2 This

report, in common with most risk reporting, sets out the level of risk

estimated in a previous period. This is because it takes time to assemble this

information so, in reports such as this, there will always be an element of

reporting estimates made in a past period.

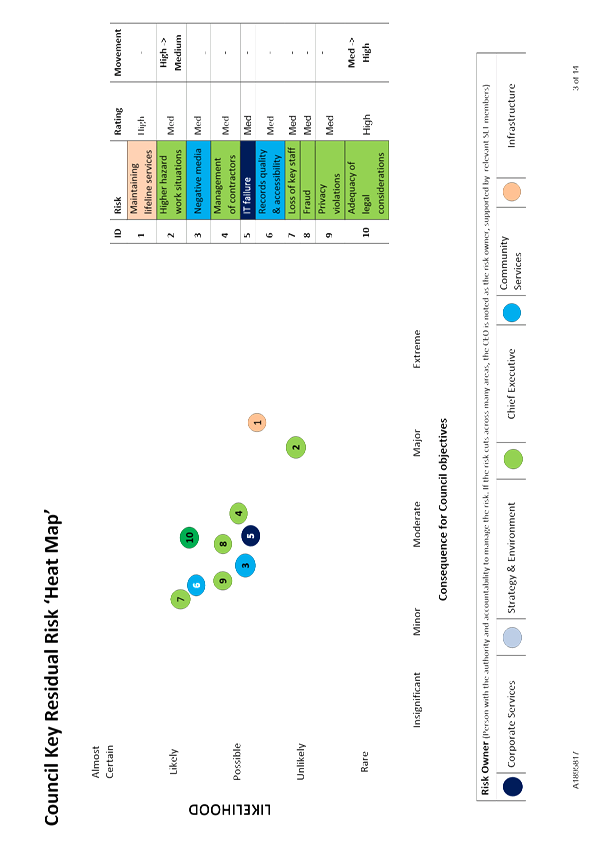

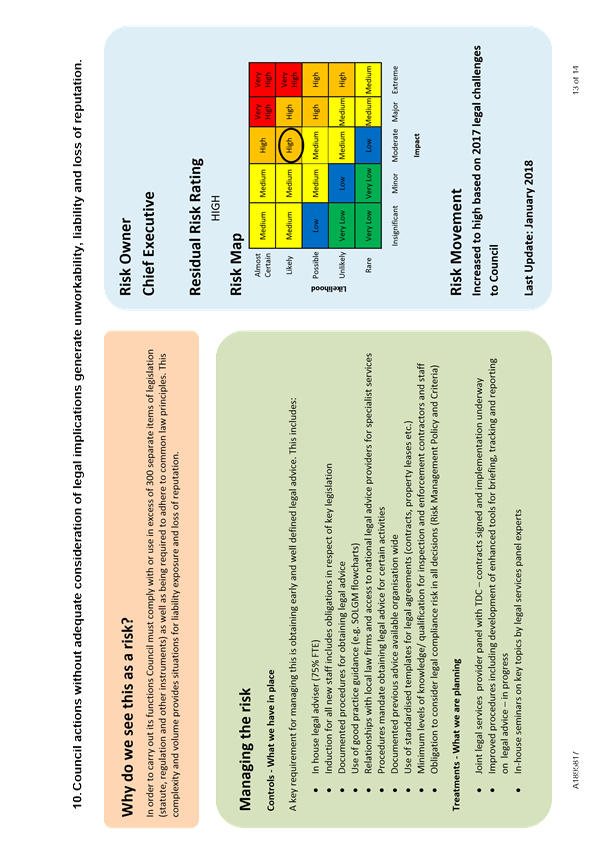

4.3 As

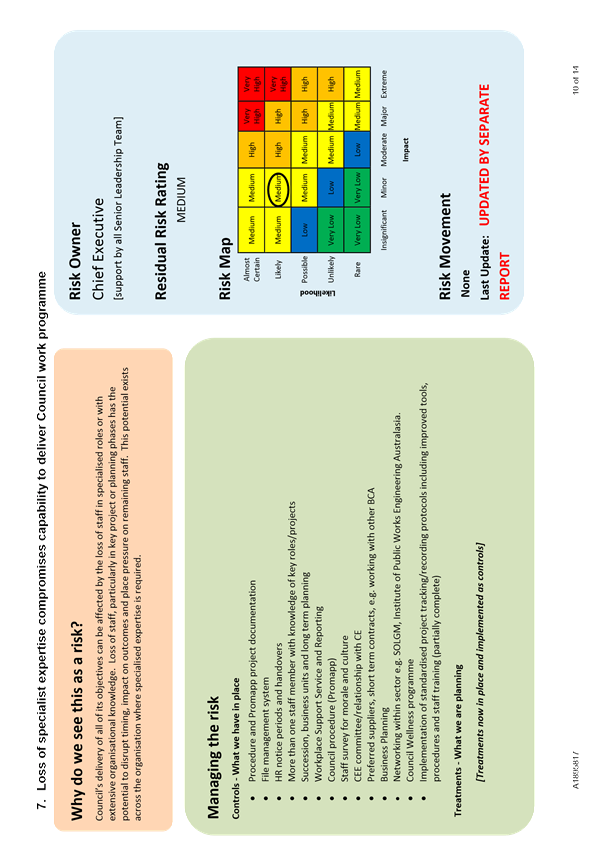

an example, the estimated risk level for key risk 10 (Council actions without

adequate consideration of legal implications…) has been increased in this

report. This is based on improved information about incidents where events

actually occurred during 2017 (some from internal audit work). The report also

notes the actions in progress to improve controls in this area (called

treatments in risk management jargon). It is therefore likely that the next

forward estimate of this risk will change again as these planned actions

actually occur.

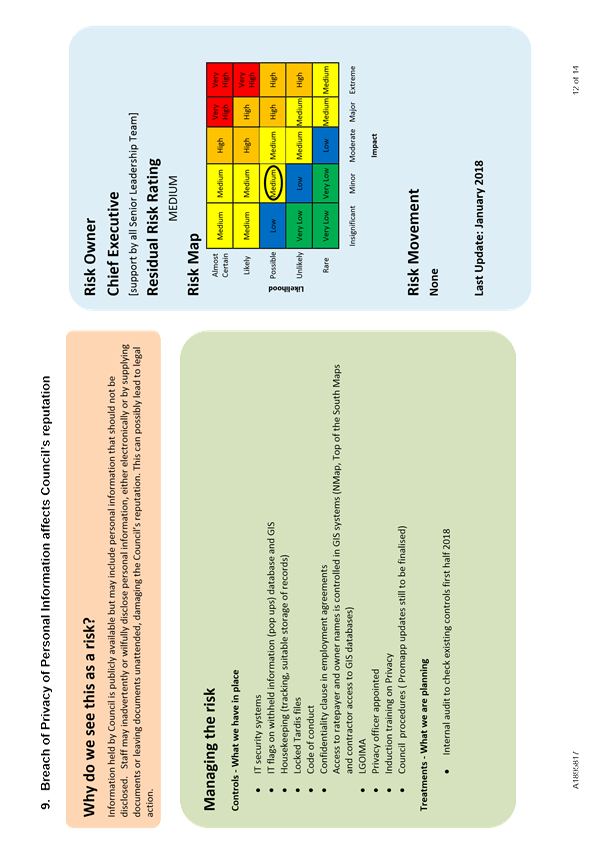

Other risk level

changes

4.4 Two

other changes in risk level are shown in the attachment. However, both of these

changes do not affect the risk ranking in relation to that area. In one case,

review of available information shows that the projected likelihood of damage

to the Council’s reputation from negative public perceptions has

decreased. The resulting risk ranking does not however change – i.e. it

remains at medium.

4.5 A

similar situation occurs with the IT failure risk area. For the reporting

period the likelihood of these failures affecting the organisation has

increased. But again the risk ranking remains at medium, and again action is

underway to address this risk.

Summary of

control changes since last report

4.6 The

table below summarises areas where controls on key risks have changed (both

progress on implementation and delays).

|

Key risk area

|

Progress on risk treatments since last report

|

|

1 Maintaining lifeline

services …

|

· Exercise to test and improve

responding to major disruptions re scheduled, now due 23 February

· Ongoing programme through to 2020

of work from regional lifelines review now underway

|

|

4.

Contracts management …

|

· Contracts management database development contract

signed –implementation of required software scheduled for June quarter

· Upgrade of NZS3910 (large civil works) contract

template delayed by lack of technical capacity in Council – now

scheduled for next financial year

|

|

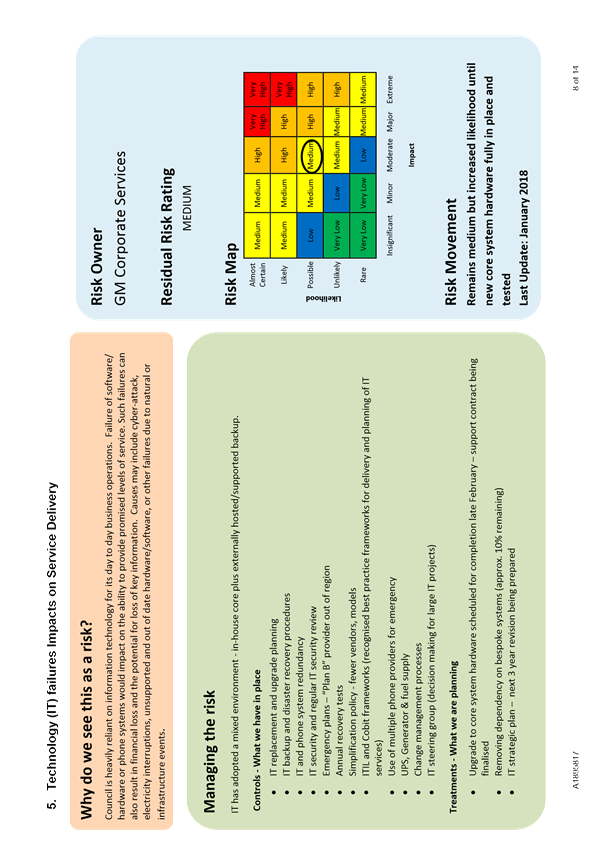

5. IT

failure impacts on service delivery

|

· Upgrade of core hardware and backup systems underway

– Scheduled for completion late February

|

|

10.

Lack of adequate consideration of legal implications

|

· Legal panel contracts signed but set up of support

procedures still in progress.

|

5. Options

5.1 It

is recommended that this report be received as it will further improve the

Subcommittee’s understanding of the risks faced by Council and the

actions being taken to manage them.

5.2 There

can be value from a discussion of the factors contributing to risks and the

Subcommittee may consider such a discussion useful.

Steve

Vaughan

Risk

& Procurement Analyst

Attachments

Attachment 1: A1895817 - Key

Organisational Risks Quarter 4 Calendar 2017 ⇩

|

Important considerations for decision making

|

|

1. Fit

with Purpose of Local Government

This report describes risk management activity. Risk

management is a tool to enable more efficient and effective provision of

services as set out in section 10(1)(b) of the LG Act.

|

|

2. Consistency

with Community Outcomes and Council Policy

This report describes risk management activity. Risk

management at its most fundamental is about achieving an organisation’s

objectives (in this case as set out in Nelson City Council’s planning

documents) with increased clarity, efficiency and effectiveness.

|

|

3. Risk

The report does not recommend a particular goal or

objective to which risks may be considered. It serves to provide information

about Council’s work in addressing those risks judged to be key to the

organisation achieving its objectives.

|

|

4. Financial

impact

This is a report on work already underway as part of

Council’s regular management activity. Therefore there are no

additional funding implications.

|

|

5. Degree

of significance and level of engagement

This matter is of low significance under the

Council’s Significance and Engagement Policy. Therefore no external

consultation has been undertaken in the preparation of this report.

|

|

6. Inclusion

of Māori in the decision making process

There has been no consultation with Māori in

the preparation of this report, which deals with internal Council processes.

|

|

7. Delegations

The Audit, Risk and Finance Subcommittee has

responsibility for overseeing the Council’s risk management systems.

|

Item

14: Key Organisational Risks Calendar 2017 - 4th Quarterly Report: Attachment 1

Item 15: Health, Safety

and Wellbeing Performance Report, October - December 2017

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

REPORT R8871

Health,

Safety and Wellbeing Performance Report, October - December 2017

1. Purpose

of Report

1.1 To

provide the Subcommittee with a quarterly report of health, safety and

wellbeing data collected over the October to December quarter of 2017.

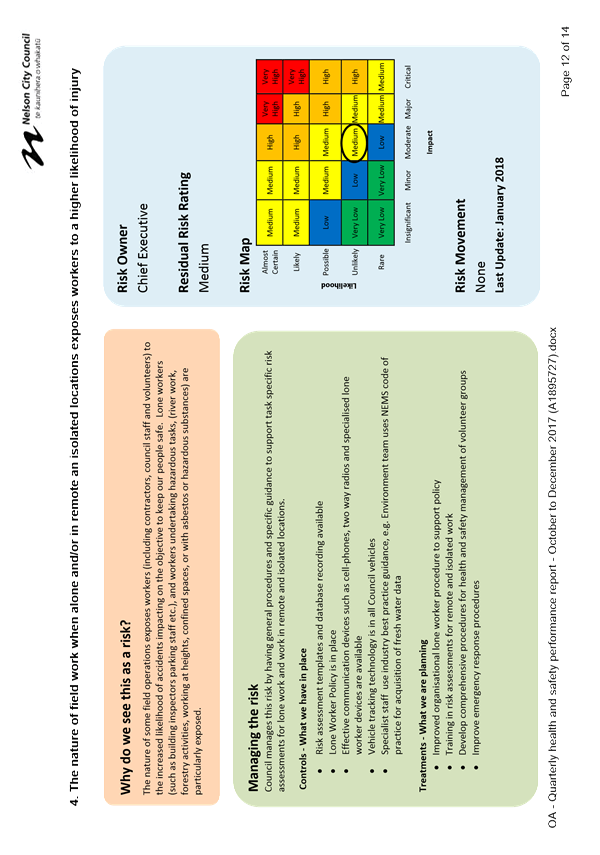

1.2 To

update the Subcommittee on key health and safety risks, including controls and

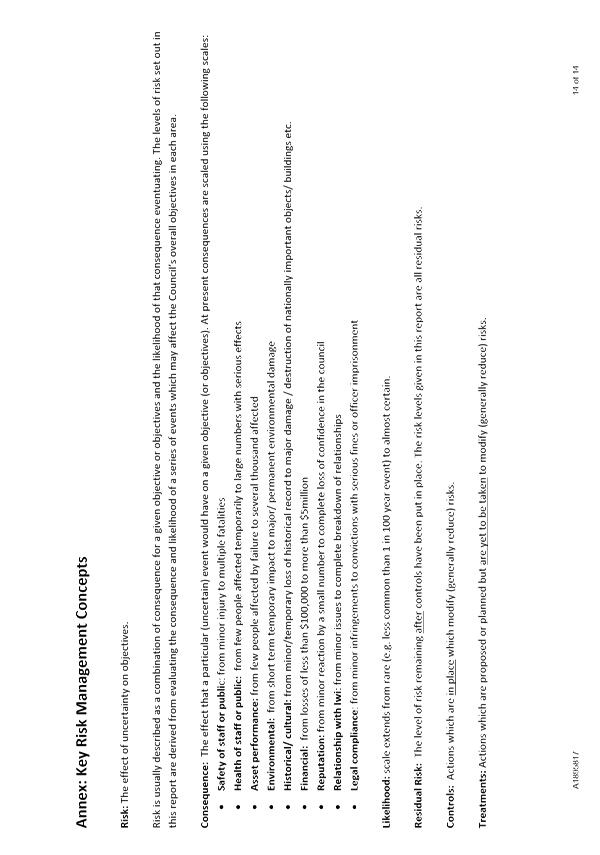

treatments.

2. Summary

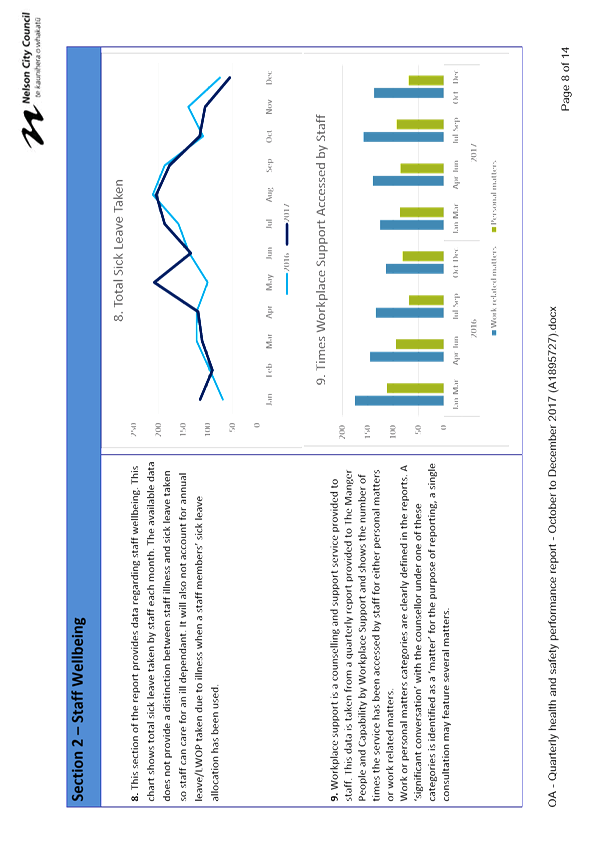

2.1 Health,

safety and wellbeing performance data reports provide an overview of health and

safety performance based on key lead and lag indicators. Where a concerning

trend is identified more detail is provided in order to better understand

issues and implement appropriate controls.

2.2 Reporting

on key health and safety risks provides further depth and detail to the health

and safety risks reported in the organisational risk report.

3. Recommendation

|

That the Audit, Risk and Finance

Subcommittee

Receives the report Health,

Safety and Wellbeing Performance Report, October - December 2017 (R8871) and its attachment (A1895727).

|

4. Background

4.1 Councillors, as

‘Officers’ under the Health and Safety at Work Act 2015 (HSWA), are

expected to undertake due diligence on health and safety matters.

Council’s Health and Safety Governance Charter states that Council will

receive quarterly reports regarding implementation of health and safety.

Council has delegated the responsibility for health and safety to the Audit,

Risk and Finance Subcommittee.

5. Discussion

Data Reports

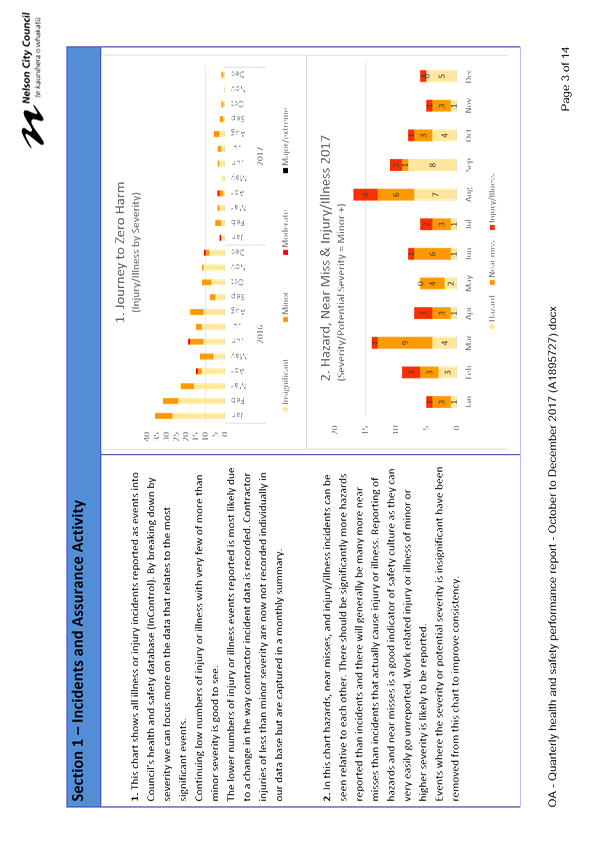

5.1 Incident

data of particular note in this report relates to security incidents, which

have primarily been groups of young people causing disruption at Stoke Library,

and disorder by a resident at the Brook Camp.

5.2 A

particularly concerning incident during November was when two elderly customers

at the Elma Turner Library received needle stick injuries from sewing machine

needles believed to have been fired as blow darts through a straw or similar.

5.3 Recent

work in the area of contractor health and safety management has resulted in

more contractor health and safety plan reviews being completed.

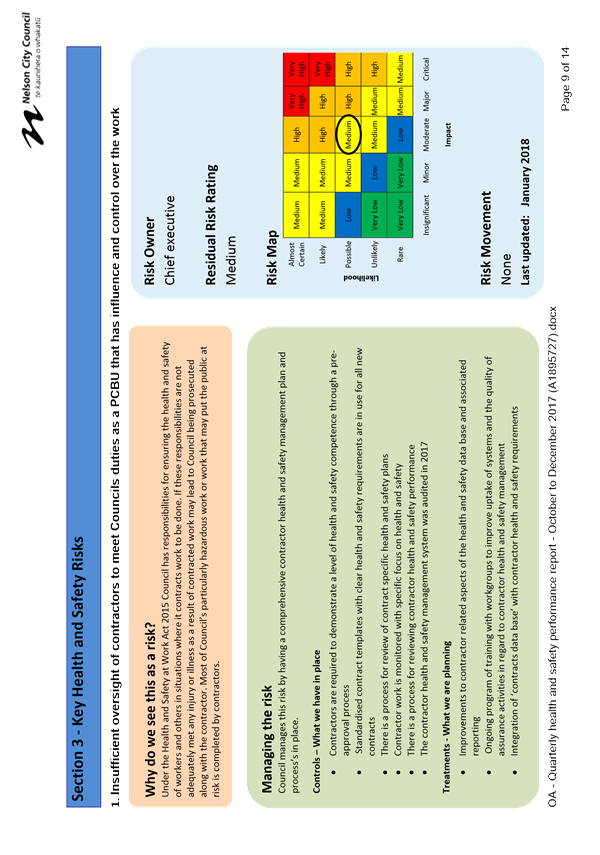

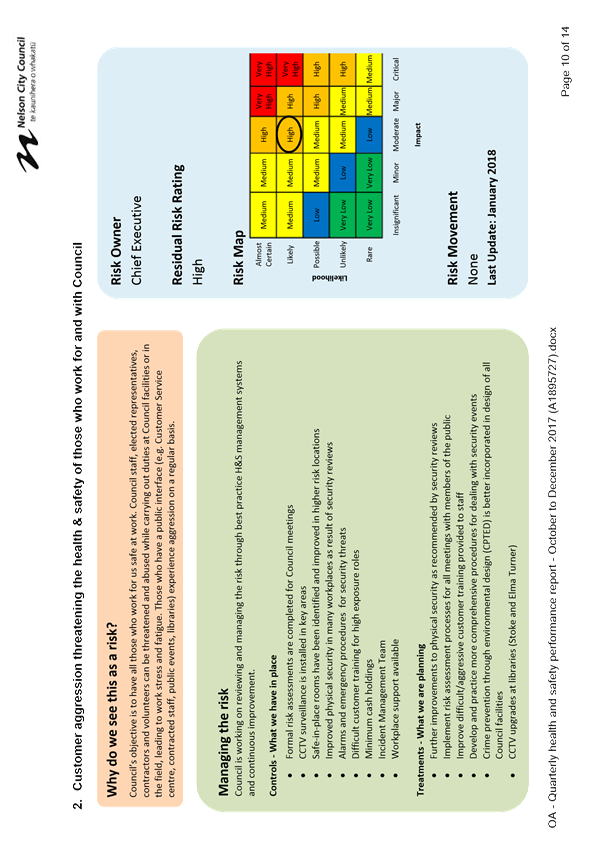

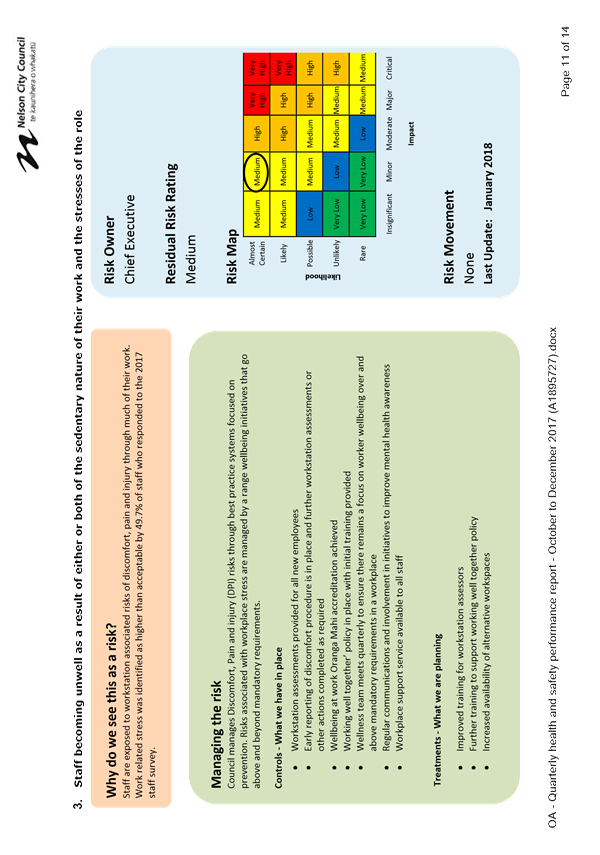

Key Health and Safety Risk

Review

5.4 Key

health and safety risks were comprehensively reviewed in November 2017. This

has resulted in some changes to the risk headings reported on and a change in

format to align with the organisational risk reporting.

5.5 A

risk labelled ‘Harm to the public from Council or contractor work’

has been removed as a key risk heading. Such risks are addressed by the

controls relating to oversight of contractors or customer aggression.

5.6 The

risk labelled ‘Lone work’ has been amended to include ‘remote

and isolated work’ as many of the controls overlap and there are specific

requirements required by regulations for remote and isolated work.

5.7 ‘Work

in high hazard environments’ has been removed as such situations will

relate to contractor work or remote and isolated work. Health and safety

management requirements for high hazard environments are well integrated within

contractor management processes.

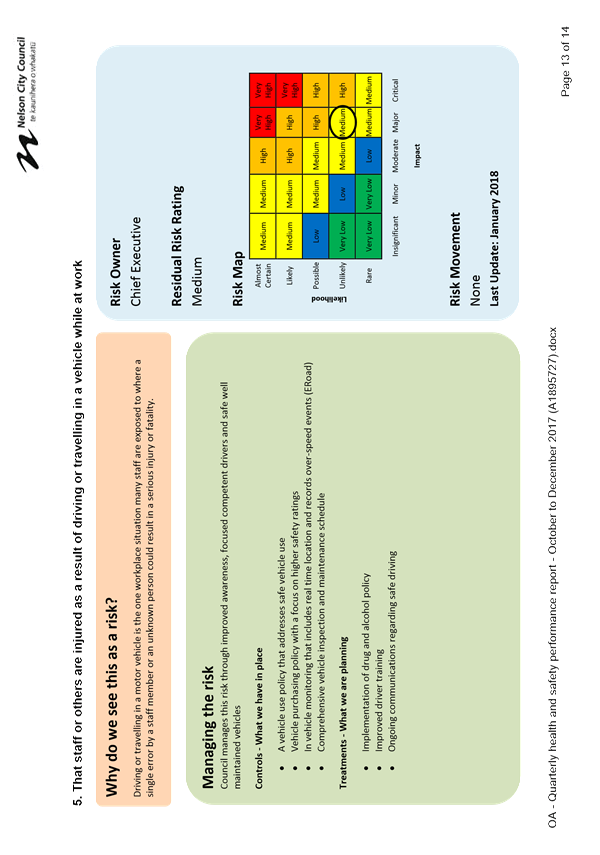

5.8 Motor

vehicle travel at work has been included in the key risks. Although this risk

has always been present, there has been significant recent development in

regard to acceptance of this risk in workplaces.

Key

Health and Safety Risk Update

5.9 Although

the risk headings have changed all key health and safety risks have been

assessed as remaining at medium apart from ‘Security – Customer

Aggression’ which continues to be assessed as a High risk.

5.10 There

has not been one particular area where customer aggression has been assessed as

a high risk, however it has been assessed as a medium risk in a number of areas

which increases the overall likelihood of a higher consequence event.

5.11 The

recent incidents at Stoke Library provide further evidence that this risk area

requires treatments to be prioritised. As further controls are implemented it

is expected that this will move to a Medium risk.

General work

programme

Governance activities

5.12 During

this reporting period Mayor Reese participated in site visits to the Nellie

Nightingale Library, York Stream upgrade and Saxton Velodrome projects.

Councillor Walker visited the Neale Park Pump Station Upgrade construction

site.

Other activities

5.13 Addressing

the increase in security incidents at Stoke Library was a significant focus

during November and December. The response involved staff from multiple

business units across Council who prioritised this work and is further outlined

in a separate report on security at Council Libraries.

5.14 There

has been a significant increase in focus on health and safety for library staff

resulting from this work.

5.15 Procedures

to address health and safety requirements for events and venue hire have been

developed.

Malcolm

Hughes

Health

and Safety Adviser

Attachments

Attachment 1: A1895727 - Quarterly

Health, Safety and Wellbeing Performance Report, October - December 2017 ⇩

Item

15: Health, Safety and Wellbeing Performance Report, October - December 2017:

Attachment 1

Item 16: Security

Incidents at Council Libraries

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

REPORT R8872

Security

Incidents at Council Libraries

1. Purpose

of Report

1.1 To

provide the Subcommittee with a report on security incidents at Council

Libraries.

1.2 To

update the Subcommittee on security risk at Council Libraries and controls

taken.

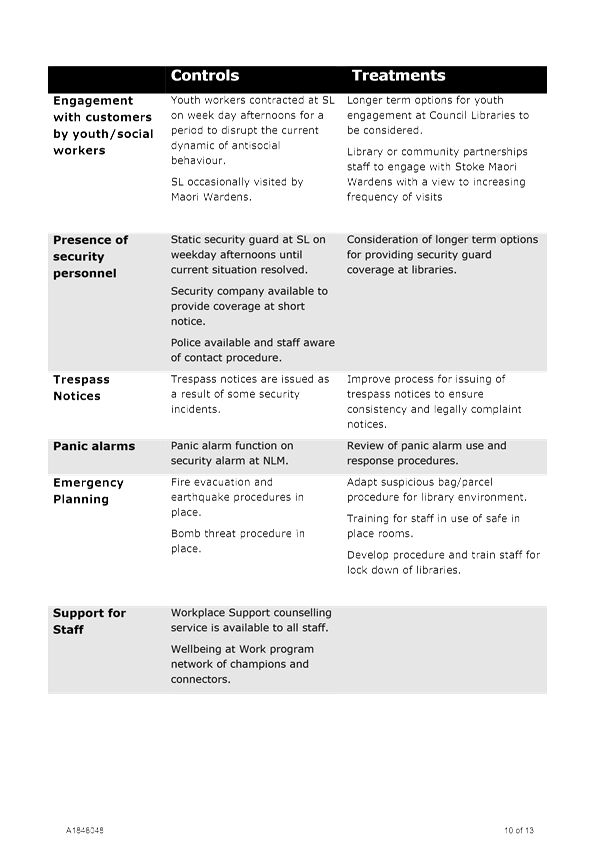

2. Summary

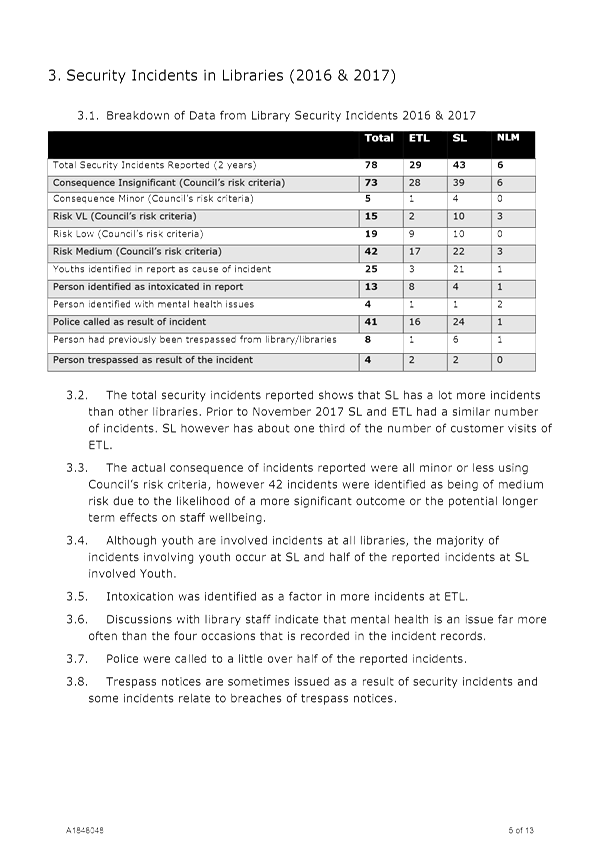

2.1 Council

Libraries have experienced security incidents for some time and this report

covers a period for which we have considerable data, January 2016 - December

2017.

2.2 In

September 2017 the Audit Risk and Finance Subcommittee requested that officers

report back to the subcommittee on security related events at Council libraries

including details of controls and treatments.

2.3 Groups

of youths engaging in antisocial and criminal behaviour while present in and

around Stoke Library (SL) increased significantly during November 2017.

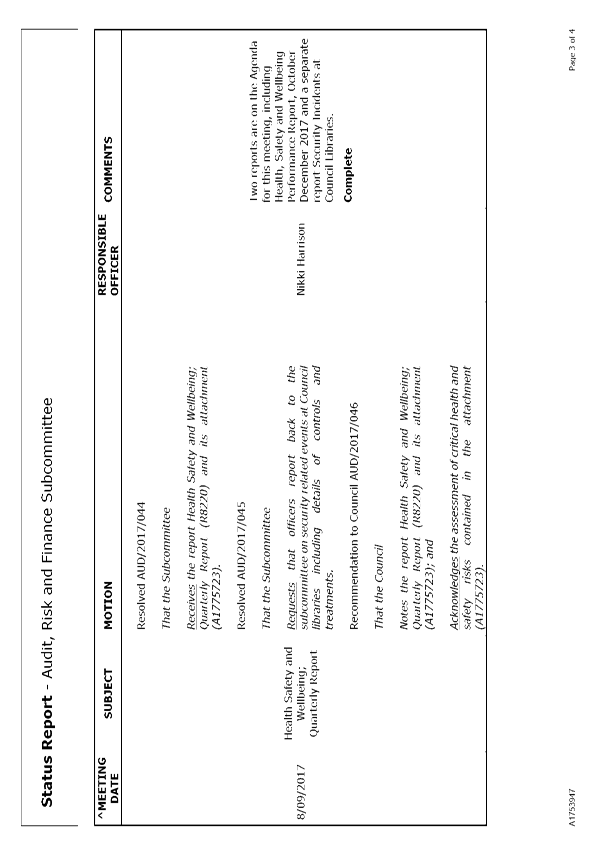

3. Recommendation

|

That

the Audit, Risk and Finance Subcommittee

Receives

the report Security Incidents at Council Libraries (R8872) and its attachment (A1848048).

|

4. Background

4.1 Organisational

Assurance has included an overview of security incidents on Council premises in

quarterly Health and Safety performance data reports since March 2017.

4.2 An

independent security risk assessment survey was carried out in September 2016

on 11 Council workplace facilities including all three Council libraries.

4.3 Actions

resulting from the independent security risk assessment recommendations were

assigned to business unit managers in February 2017.

4.4 In

September 2017 the Audit Risk and Finance Subcommittee passed the following

resolution:

Requests that

officers report back to the subcommittee on security related events at Council

libraries including details of controls and treatments.

5. Discussion

5.1 Data

relating to security incidents at Council Libraries for the last two years has

been summarised and key observations outlined in the attachment.

5.2 An

overview of the recent increase in security incidents at Stoke Library is provided

in the attachment. The response to this situation has been significant, has

involved staff from across various parts of Council, and is still

evolving. Engagement with external parties has included Police and youth

workers. Initial controls have been effective at separating staff from

many unpleasant interactions. Longer term preventative controls and treatments

are being introduced in a staged manner with ongoing review.

5.3 Controls

and treatments including those recommended in the 2016 security risk assessment

survey are included in the controls and treatments section of the attachment.

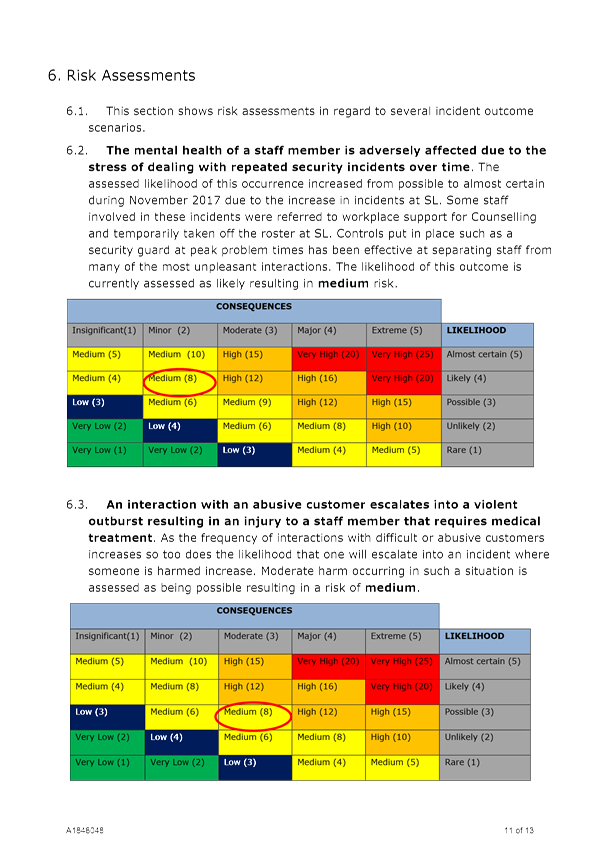

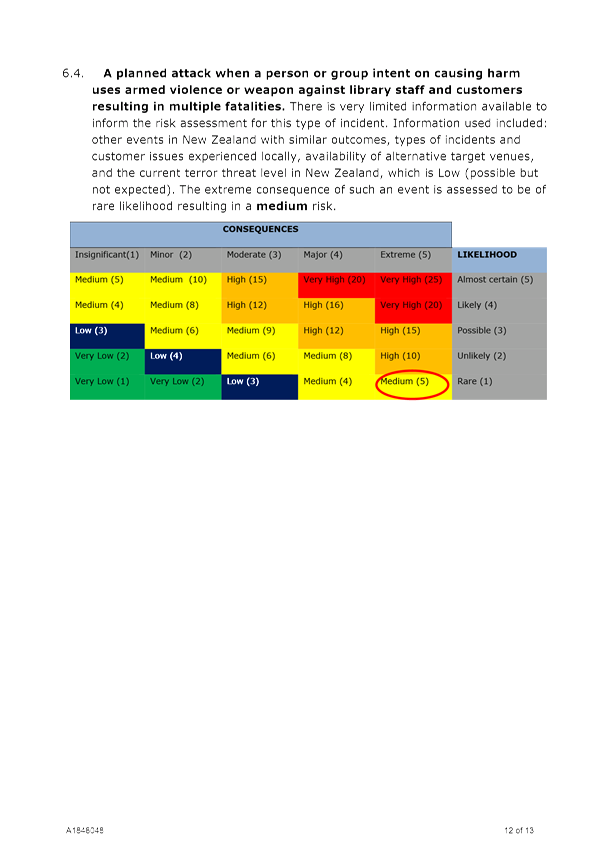

5.4 Risk

assessments for a range of scenario outcomes using Council’s risk

criteria are also included in the attachment.

5.5 There

are wider issues at play, which go beyond Health and Safety. This

includes consideration of longer term solutions to the underlying causes of

youth issues at Stoke Library. A more detailed report

will go to the Community Services committee outlining actions as to how issues

with youth will be addressed.

Malcolm

Hughes

Health

and Safety Adviser

Attachments

Attachment 1: A1848048 - Security at

Council Libraries ⇩

Item

16: Security Incidents at Council Libraries: Attachment 1

Item 17: Recruitment in

a Tight Labour Market

|

|

Audit, Risk and Finance Subcommittee

13 February 2018

|

REPORT R8885

Recruitment

in a Tight Labour Market

1. Purpose

of Report

1.1 At

its meeting on 14 November 2017, the Audit, Risk and Finance Subcommittee

requested a report on how the organisation is managing the risk to the

organisation’s objectives arising from increased difficulty in finding

and retaining the right staff expertise.

2. Recommendation

|

That the Audit, Risk and Finance

Subcommittee

Receives the report Recruitment

in a Tight Labour Market (R8885)

and its attachment (A1896279).

|

3. External

Context

3.1 New

Zealand’s unemployment rate has returned to levels previously seen prior

to the Global Financial Crisis (4.6% in September 2017, Statistics NZ), and the

rate of unemployment is even lower in the top of the south (2.2% September

2017). In the year prior to November 2017, online advertised vacancies rose by

8.5% (Ministry of Business, Innovation and Employment Jobs Online monthly

report November 2017). MBIE’s Labour Market Scorecard in March 2017 noted

that, while unemployment varied across regions, in

Nelson/Marlborough/Tasman/West Coast it had decreased more than other regions.

3.2 MBIE

also produces a quarterly Labour Market Report. The September 2017 quarterly

report (attached) shows that organisations across New Zealand are reporting

decreased ease of finding labour at present (figure 2, page 4 of the

attachment).

3.3 Demographic

data shows that Nelson’s population is ageing faster than the New Zealand

average, and while this is expected, in time, to have an impact on the ability

of employers to retain and recruit the skills needed, it is likely that other

external factors are for the present having a greater impact.

3.4 Labour

market conditions fluctuate over time as a result of external factors such as

unemployment rates, labour force participation, economic conditions, business

confidence, migration policy etc, and that impacts not only the ease with which

the organisation recruits but also significantly affects employee retention and

turnover. One yardstick which provides at least a partial measure of the degree

of increased difficulty is the number of roles which Council has had to

advertise more than once in order to find the right person – in 2016

Council re-advertised seven vacancies, and in 2017 Council re-advertised nine

vacancies.

4. Organisational

responses to the conditions

4.1 In

the past 12 months Nelson City Council has responded in a number of ways in

order to manage the current increased challenge of recruitment:

· a number of

initiatives (e.g. recognition, communication) relating to culture, wellbeing

and employee engagement in order to retain its existing employees in an

environment where there is an increased range of employment opportunities for

them outside the organisation;

· increased use of

recruitment agencies;

· increased use of

contractor and temp resources to fill gaps between one employee leaving and the

next one commencing;

· seconding people

from within the organisation to fill resource gaps in other parts of the

organisation;

· taking a more

flexible approach to the experience level of the appointee – i.e. hiring

at more senior or more junior levels than initially envisaged;

· specific retention

actions in a small number of individual cases (e.g. job re-design in order to

retain a skilled employee).

4.2 Nelson

City Council also has in place a number of longer-term initiatives which aim to

even out the impact of periodic tightening in labour market conditions and

skill shortages in specific areas, including:

· a Flexible Work

Policy to ensure we provide flexible work options for our employees whenever

possible, so reducing the risk of losing people with good skills;

· succession

planning for key roles to ensure we are growing our own people for progression

within the organisation;

· a range of

leadership development opportunities are provided to ensure we have a pipeline

of capable people leaders;

· a performance

management framework which includes consideration of development needs for each

staff member to ensure the organisation keeps building the capability of our

people;

· cadet and graduate

positions in specific areas to ensure the development of a pipeline of

individuals with good skills and relevant experience and qualifications;

· maintenance of

accredited employer status with Immigration NZ to make it easier to hire

skilled migrants;

· monitoring market

remuneration rates to ensure Council continues to pay competitive rates;

· upgrade of Civic

House interiors (beginning with Level 1 in 2018) to ensure that Council is able

to retain and attract people through providing modern workspaces which are

adequately lit, ventilated and furbished.

5. Planned

actions in 2018

5.1 Projects

planned in 2018 to build on Nelson City Council’s ability to retain,

develop and attract the right people include a refresh of its leadership

development learning opportunities, continued focus on employee engagement and

ongoing initiatives focusing on wellbeing and improving communication within

the organisation, and a refresh of its employer brand via a new careers portal

and e-recruitment technology.

6. Summary

6.1 Nelson

City Council continues to retain, attract, and hire very good people. The

current tight labour market conditions mean that in some instances recruitment

of those people is taking longer than when the labour market is less

constrained. This leads to some increased costs, specifically in filling short

term gaps with more expensive contractor and temporary resources. However while

a proportion of vacancies take longer to fill, most are filled in the usual

timeframes. Most importantly, Council has not compromised on the calibre of

those it hires – during 2017, despite the more challenging context,

Council has hired individuals it can be proud of having in the organisation.

6.2 No

organisation however can afford to be complacent, especially given the

complexity that an ageing demographic will add to the external factors

(unemployment rates, economic buoyancy, government migration policy, etc)

affecting labour supply. It is therefore critical that Council continues to

focus on engaging and developing its current employees, providing an inclusive

and productive work environment, and managing its employer brand and reputation

so that it continues to attract and hire high calibre new employees.

Stephanie

Vincent

Manager

People and Capability

Attachments

Attachment 1: A1896279 - MBIE Quarterly

Labour Market Report, Nov 2017 ⇩

Item

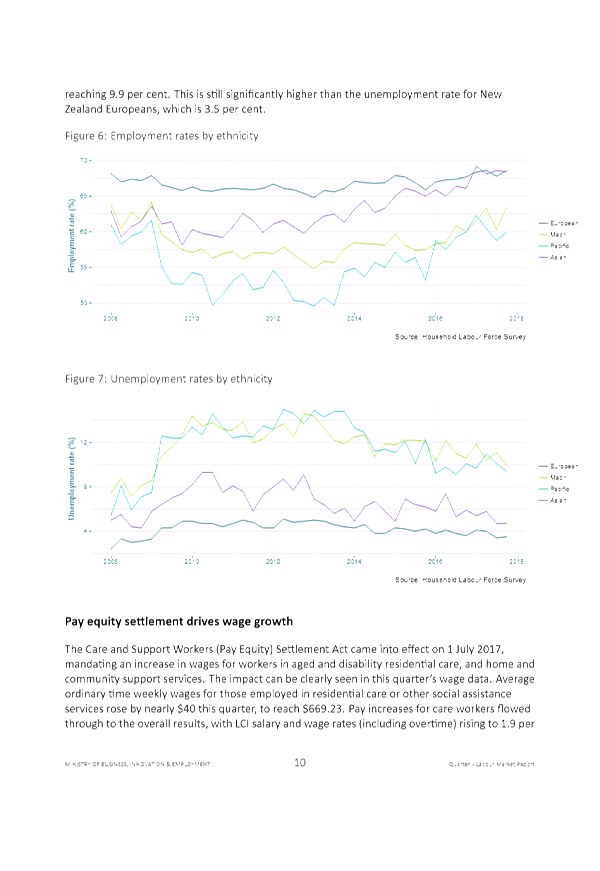

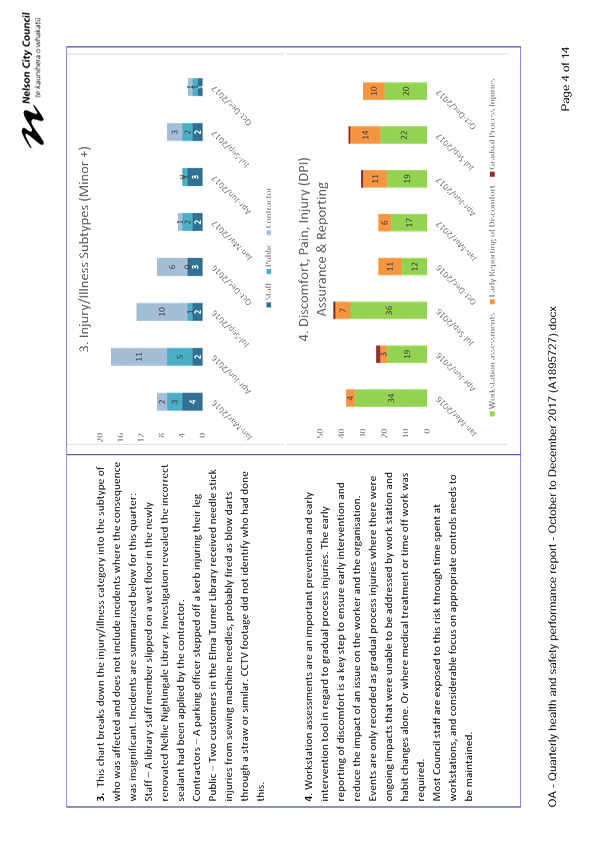

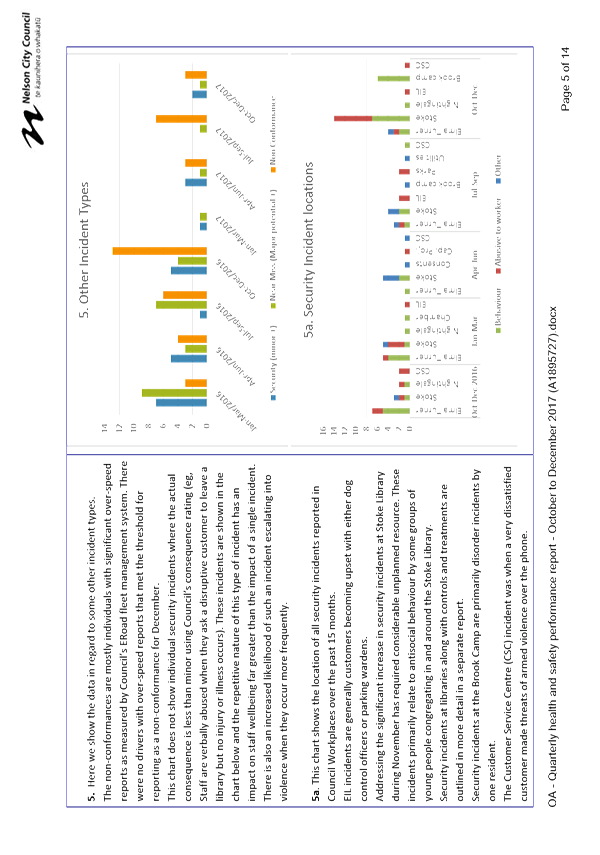

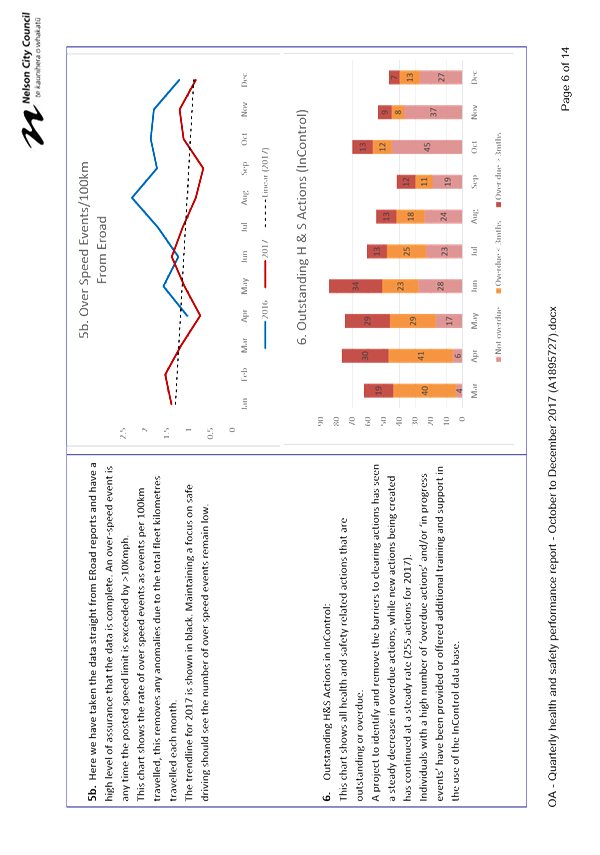

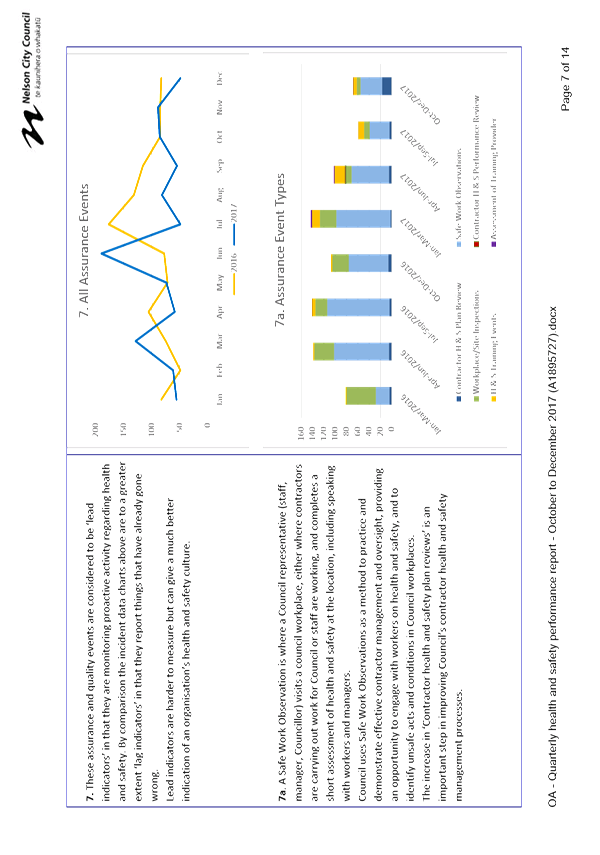

17: Recruitment in a Tight Labour Market: Attachment 1