AGENDA

Ordinary meeting of the

Audit, Risk and Finance Subcommittee

Thursday 10 September 2015

Commencing at 1.00pm

Ruma Mārama

Level 2A, Civic House

110 Trafalgar Street, Nelson

Membership: Mr John Peters (Chairperson), Her Worship the

Mayor Rachel Reese, Councillors Ian Barker and Brian McGurk, and Mr John Murray

Guidelines for councillors

attending the meeting, who are not members of the Committee, as set out in

Standing Orders:

·

All councillors, whether or not they are members of the

Committee, may attend Committee meetings (SO 2.12.2)

·

At the discretion of the Chair, councillors who are not Committee

members may speak, or ask questions about a matter.

·

Only Committee members may vote on any matter before the

Committee (SO 3.14.1)

It is good practice for both Committee members and

non-Committee members to declare any interests in items on the agenda.

They should withdraw from the table for discussion and voting on any of these

items.

Audit, Risk and Finance

Subcommittee

Audit, Risk and Finance

Subcommittee

10

September 2015

Page

No.

1. Apologies

1.1 An

apology has been received from Mr John Peters.

2. Confirmation

of Order of Business

3. Interests

3.1 Updates

to the Interests Register

3.2 Identify

any conflicts of interest in the agenda

4. Public

Forum

5. Confirmation

of Minutes

5.1 30

July 2015 5 - 12

Document number M1385

Recommendation

THAT

the minutes of the meeting of the Audit, Risk and Finance Subcommittee, held

on 30 July 2015, be confirmed as a true and correct record.

6. Status

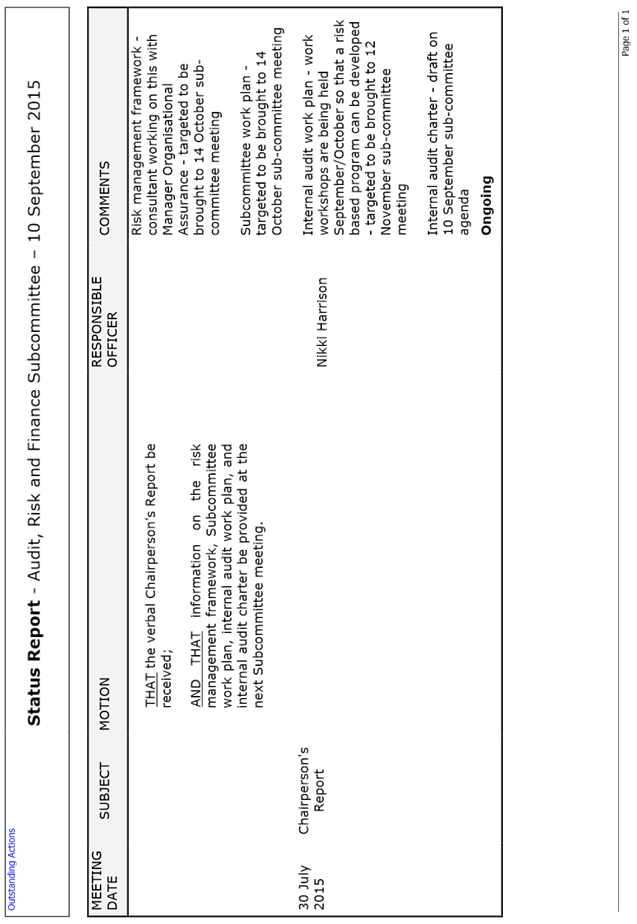

Report - Audit, Risk and Finance Subcommittee - 10 September 2015 13 - 14

Document number R4799

Recommendation

THAT the Status Report Audit, Risk

and Finance Subcommittee 10 September 2015 (R4799) and its attachment (A1324298) be received.

7. Chairperson's

Report

8. Draft

Annual Report 30 June 2015 15 - 83

Document number R4210

Recommendation

THAT the report Draft Annual

Report 30 June 2015 (R4210) and

its attachments (A1417003 and A1396738) be

received.

9. Carry

Forwards from 2014/15 84 - 88

Document number R4211

Recommendation

THAT the report Carry Forwards

from 2014/15 (R4211) be received.

Recommendation to Governance

Committee and Council

THAT

$4,233,000 of unspent capital budget from 2014/15 be carried forward for use in

2015/16;

AND

THAT $403,000 of capital spent in 2014/15 be offset against

2015/16 budgets;

AND

THAT an amount of $107,000 operating budget be carried

forward for use in 2015/16.

10. Draft

Internal Audit Charter 89 - 95

Document number R4777

Recommendation

THAT the report Draft Internal

Audit Charter (R4777) and its

attachment (A1395134) be

received.

Recommendation to Governance

Committee and Council

THAT

the Draft Internal Audit Charter (A1395134) be approved.

Minutes of a meeting of the

Audit, Risk and Finance Subcommittee

Held in Ruma Mārama,

Level 2A, Civic House, 110 Trafalgar Street, Nelson

On Thursday 30 July 2015,

commencing at 1.00pm

Present: Mr

J Peters (Chairperson), Councillors I Barker and B McGurk, and Mr J Murray

In Attendance: Chief

Executive (C Hadley), Group Manager Infrastructure (A Louverdis), Group Manager

Community Services (C Ward), Group Manager Corporate Services (N Harrison),

Accounting Services Manager (L Anderson), and Administration Adviser (S McLean)

Apology: Her

Worship the Mayor Rachel Reese

1. Apology

|

Resolved AUD/2015/018

THAT an apology be

received and accepted from Her Worship the Mayor Rachel Reese.

Barker/McGurk Carried

|

2. Confirmation of Order of Business

The

Chairperson advised of one late item for the public part of the meeting, and

that the following resolution needed to be passed for the items to be

considered:

2.1 Capital

Projects 2014/15

|

Resolved AUD/2015/019

THAT

the item regarding Capital Projects 2014/15 be considered at this meeting as

a major item not on the agenda, pursuant to Section 46A(7)(a) of the Local

Government Official Information and Meetings Act 1987, to enable a timely

decision to be made.

Barker/McGurk Carried

|

3. Interests

There were no updates to the

Interests Register, and no interests with items on the agenda were declared.

4. Public Forum

There was no public forum.

5. Confirmation of Minutes

5.1 18

June 2015

Document number M1286, agenda

pages 6 - 12 refer.

It was noted that as the only

business transacted in public excluded on 18 June 2015 was to confirm the

minutes, this business has been recorded in the public minutes. In accordance

with the Local Government Official Information Meetings Act, no reason for

withholding this information from the public existed.

|

Resolved AUD/2015/020

THAT the minutes of

the meeting of the Audit, Risk and Finance Subcommittee, held on 18

June 2015, be confirmed as a true and correct record.

Murray/McGurk Carried

|

6. Status Report - Audit Risk and

Finance Subcommittee - 30 July 2015

Document number R4596, agenda

pages 13 - 14 refer.

In response to questions, the

Chief Executive, Clare Hadley, advised that only resolutions containing actions

were included in the status report.

|

Resolved AUD/2015/021

THAT the Status Report Audit,

Risk and Finance Subcommittee 30 July 2015 (R4596) and its attachment (A1324298) be received.

McGurk/Barker Carried

|

7. Chairperson's Report

The Chairperson asked for

further information to be provided to the Subcommittee on matters such as

internal audit and risk management framework.

In response to a request from

the Chairperson, the Chief Executive, Clare Hadley, advised that an internal

appointment had been made to the Internal Audit position. She said there had

not been any suitable applications to the Risk Management Analyst position, and

alternative arrangements for that role were being looked into. Mrs Hadley added

she was very pleased with the experience the new Manager Organisational

Assurance brought to the organisation.

Group Manager Corporate

Services, Nikki Harrison, said an internal audit charter was being prepared for

the 10 September 2015 Subcommittee meeting.

|

Resolved AUD/2015/022

THAT

the verbal Chairperson’s Report be received;

AND

THAT information on the risk management framework,

Subcommittee work plan, internal audit work plan, and internal audit charter

be provided at the next Subcommittee meeting.

Peters/Murray Carried

|

8. Update on charging interest on

general debtors

Document number R4579, agenda

pages 15 - 22 refer.

Group Manager Corporate Services,

Nikki Harrison, presented the report.

In response to a question, Ms

Harrison advised that penalties charged on rates and water were lump sum

charges and this was a different process to charging interest.

There was discussion on the Draft

Debt Management Policy and the allowance for charging interest at the

discretion of the Group Manager Corporate Services.

In response to a suggestion that

spreadsheets could be a viable alternative, the Chief Executive, Clare Hadley,

cautioned the Subcommittee that running a manual workaround process to charge

interest would increase the risk of error. She said Council would either need

to invest in additional technology or determine that a process for charging

interest was not warranted.

Mrs Hadley highlighted that

general debtor levels were low and outstanding debts were only a small portion

of debtors.

There was discussion on penalties

set by local government legislation, which were integrated into the current

accounting software.

Ms Harrison confirmed

Council’s terms of trade would reflect the ability to charge

discretionary interest.

|

Resolved AUD/2015/023

THAT the report Update on

charging interest on general debtors (R4579)

and its attachment (A1353429) be

received;

AND

THAT Council do not proceed with charging interest on all

overdue general debtors at this time.

Barker/McGurk Carried

|

Mrs Harrison tabled the debt

collection process used by officers (A1396334).

Accounting Services Manager,

Lynn Anderson, provided detail on the debt collection process after 60 and 90

days.

In response to a question, Ms

Anderson said marina debt was managed by Nelmac to a certain extent.

Ms Harrison confirmed the debt

collection process would be included in the Draft Debt Management Policy.

|

Recommendation to Governance

Committee and Council AUD/2015/024

THAT

the Draft Debt Management Policy (A1353429) be approved.

Barker/McGurk Carried

|

|

Attachments

1 A1396334 - Tabled

Document - Action and Collect Debtors Overdue Accounts Process

|

9. Update on business case approach

Document number R4454, agenda

pages 23 - 27 refer.

In response to questions, Mrs

Hadley confirmed the capital expenditure projects listed in Attachment 1 to the

report (A1331113) were reported to Council in various ways. She advised the

Civic House Renewal Programme would be reported to the Commercial Subcommittee

as and when there was any information to report within the delegations for the

Subcommittee.

|

Resolved AUD/2015/025

THAT the report Update on

business case approach (R4454)

and its attachment (A1331113) be received.

Murray/Barker Carried

|

10. Corporate Report to 31 May

2015

Document number R4523, agenda

pages 28 - 48 refer.

Group Manager Corporate Services,

Nikki Harrison, presented the report and tabled an updated NCC Variance to

Projection 31 May 2015 table (A1396340).

It was noted that information on

Maitai Walkway financials had been requested at the 18 June 2015 Subcommittee

meeting and would need to be included in the Corporate Report to the 10

September 2015 Subcommittee meeting.

Ms Harrison highlighted there

would be a larger carry forward than expected this financial year. In response

to a question, she confirmed the carry forward figure did not include gifted or

vested land. Concern was raised that carry forwards could appear to the

community that Council had rated for work which was not carried out.

In response to a question, Ms

Harrison clarified that carry forwards were a separate issue to surplus funds,

and were related to funding policy decisions. Ms Harrison added that the Long

Term Plan 2015/25 had reduced contingency funding in order to avoid overrating.

She said a portion of future carry forwards would be allocated to paying down

debt.

In response to a question, the

Chief Executive, Clare Hadley, advised the criteria for allocating funding for

economic development projects and events was tight and was focussed on

extending the shoulders of peak seasons in Nelson. She said there were few

applications that matched the criteria. Group Manager Community Services, Chris

Ward, confirmed this matter was being considered with the economic services

review.

There was discussion on the

Ridgeways Joint Venture. Ms Harrison advised she would be looking into ways to

reduce holding costs on the Ridgeways land.

|

Resolved AUD/2015/026

THAT

the report Corporate Report to 31 May 2015 (R4523) and its attachments (A1376070, A1384382, A1384389,

A1375171, A1366415, A793514) be

received and the variations noted.

Murray/McGurk Carried

|

|

Attachments

1 A1396340 - Tabled

Document - NCC Variance to Projection 31 May 2015

|

11. Capital Projects 2014/15

Document number R4646, late item

M1381 pages 2 - 4 refer.

Group Manager Corporate Services,

Nikki Harrison, presented the report.

|

Resolved AUD/2015/027

THAT the report Capital Projects

2014/15 (R4646) be received.

Barker/McGurk Carried

|

|

Recommendation to Governance

Committee and Council AUD/2015/028

THAT Council approves continuing work on 2014/15 capital

projects within the 2014/15 approved budgets, noting a report on carry

forwards will come to the Audit, Risk and Finance Subcommittee meeting on 10

September 2015.

Barker/McGurk Carried

|

12. Rates Remissions for 2014/15

Document number R4204, agenda

pages 49 - 60 refer.

Group Manager Corporate Services,

Nikki Harrison, presented the report.

In response to a question, Ms

Harrison said there were occasions where a level of judgement was required for

rates remissions, and peer reviews often took place.

|

Resolved AUD/2015/029

THAT the report Rates Remissions

for 2014/15 (R4204) and its

attachments (A1383906 and A1222068) be

received.

Murray/McGurk Carried

|

13. Insurance Renewal for

2015/16

Document number R4245, agenda

pages 61 - 64 refer.

Group Manager Corporate Services,

Nikki Harrison, presented the report.

|

Resolved AUD/2015/030

THAT the report Insurance

Renewal for 2015/16 (R4245) be

received.

McGurk/Barker Carried

|

14. Bad debt report to 30 June

2015

Document number R4206, agenda

pages 65 - 66 refer.

The Subcommittee congratulated

officers on the low level of bad debts.

|

Resolved AUD/2015/031

THAT the report Bad debt report

to 30 June 2015 (R4206) be

received.

Murray/Barker Carried

|

15. 2014/15 Audit New Zealand

Letters

Document number R4433, agenda

pages 67 - 87 refer.

Group Manager Corporate Services,

Nikki Harrison, presented the report and tabled the interim Audit New Zealand

letter to management (A1371564).

There was discussion on the

Subcommittee’s future involvement on audit matters. Ms Harrison confirmed

the Subcommittee would receive the draft Annual Report at its meeting on 10

September 2015.

It was agreed that Ms Harrison

would arrange a meeting between the auditor and the members of the Subcommittee

in September or October 2015.

In response to questions, it was

confirmed there was an internal interests register for the Senior Leadership

Team, which was soon to be rolled out to other levels of the organisation. It

was also confirmed that Council had a Procurement Policy which was clear on

conflicts of interest, and there was a ‘whistle-blowing’ service

available.

There was discussion on the

reference to independent quality assurance reviews in the audit letter. The

Chief Executive, Clare Hadley said this would be considered as and when

appropriate.

Questions were raised on fraud

protection measures used by Council. Ms Harrison highlighted that the

Subcommittee work programme due to be presented on 10 September would provide

clarity on this.

|

Resolved AUD/2015/032

THAT the report 2014/15 Audit

New Zealand Letters (R4433) and

its attachments (A1371563 and A1372353)

be received.

AND

THAT the Subcommittee support the engagement letter being

signed by Her Worship the Mayor.

Murray/McGurk Carried

|

|

Attachments

1 A1371564 - Tabled

Document - Management Letter, Interim audit of NCC - Audit New Zealand

|

There being no further business the meeting

ended at 3.12pm.

Confirmed as a correct record of proceedings:

Chairperson

Date

Chairperson

Date

|

|

Audit, Risk and Finance Subcommittee

10 September 2015

|

REPORT R4799

Status

Report - Audit, Risk and Finance Subcommittee - 10 September 2015

1. Purpose

of Report

1.1 To

provide an update on the status of actions requested and pending.

2. Recommendation

|

THAT the Status Report Audit,

Risk and Finance Subcommittee 10 September 2015 (R4799) and its attachment (A1324298) be received.

|

Gayle

Brown

Administration

Adviser

Attachments

Attachment 1: Status

Report - Audit, Risk and Finance Subcommittee - September 2015

|

|

Audit, Risk and Finance Subcommittee

10 September 2015

|

REPORT R4210

Draft

Annual Report 30 June 2015

1. Purpose

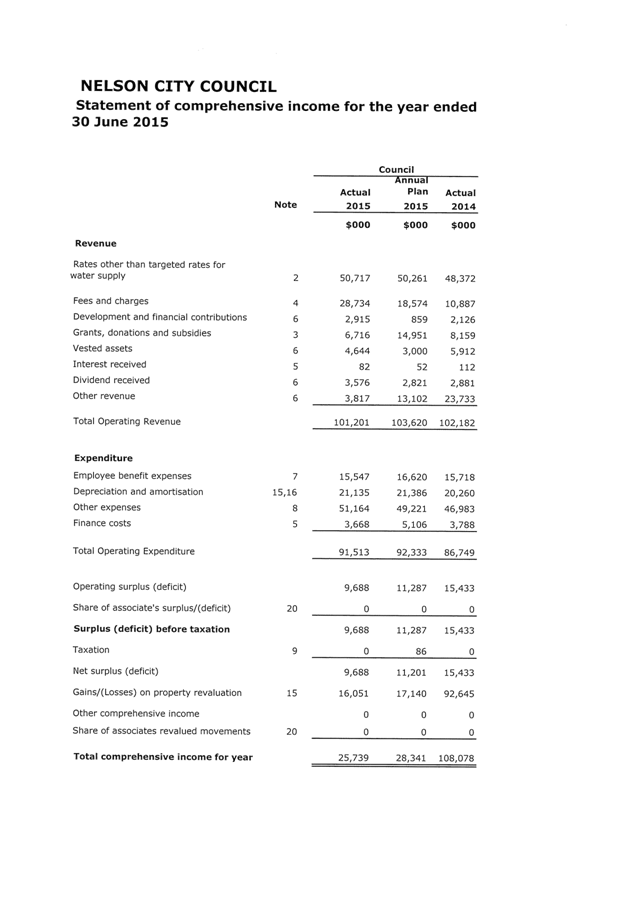

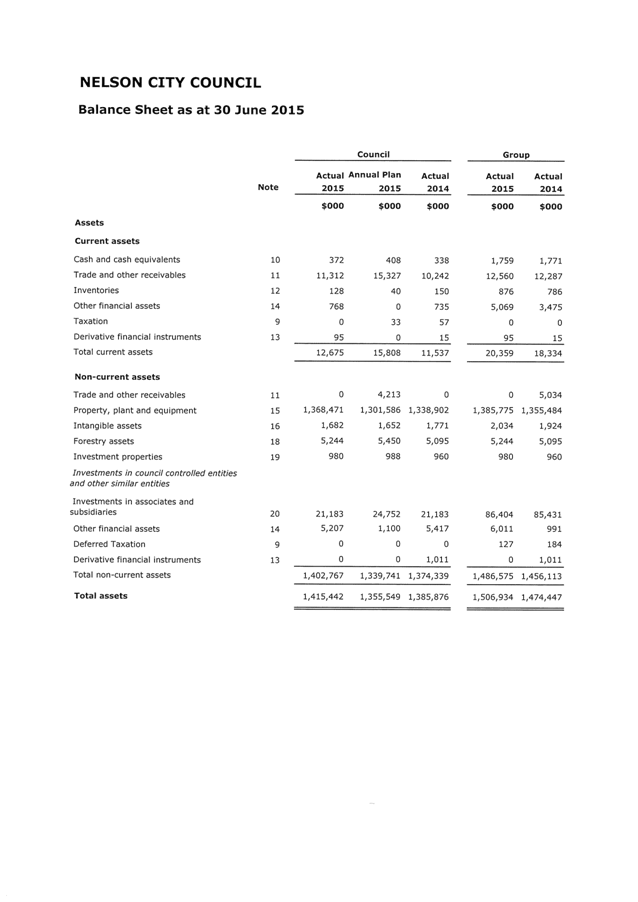

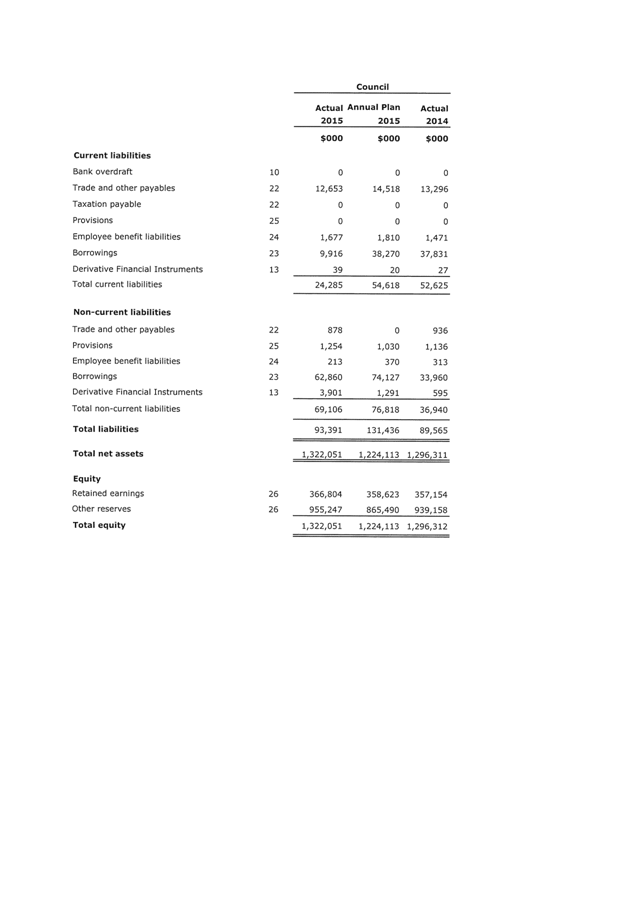

1.1 To receive the draft Annual Report 2014/15.

2. Delegations

2.1 The

Audit, Risk and Finance Committee has the delegations for monitoring

Council’s financial and service performance.

3. Recommendation

|

THAT the report Draft Annual

Report 30 June 2015 (R4210) and

its attachments (A1417003 and A1396738)

be received.

|

4. Background

4.1 The

purpose of an Annual Report is to compare the actual activities and performance

of the local authority with those intended, as set out in the applicable Annual

Plan. It also aims to promote the local authority’s accountability to the

community for the decisions made throughout the year. An Annual Report is

required under section 98 of the Local Government Act 2002.

5. Discussion

5.1 The

attached draft Annual Report 2014/15 is intended to provide Committee members

with all the information officers have obtained to date and to allow the

opportunity to provide feedback. The intention is not to present a completed

Annual Report at this stage, but rather to provide as complete a picture as

possible for consideration. This draft has not yet been audited by Audit New

Zealand, and is likely to require some modification through the auditing

process. Some notes to the accounts have yet to be prepared pending that work.

5.2 The

financial statements in the 2014/15 annual report are prepared under the new

Public Benefit Entity International Public Sector Accounting Standards (PBE

IPSAS). This has required a small number of prior year re-statements and

re-categorisations. There is also likely to be additional explanatory notes to

the financial statements, and some disclosure requirements have changed.

5.3 The

final Annual Report 2014/15 is required to be adopted by Council within four months

of the financial year’s end (by the end of October) and is proposed to be

brought to Council for adoption at all Council meeting on 15 October 2015.

6. Options

6.1 As

the Draft Annual Report is provided for information, the options are to receive

the report or not as well as provide any feedback to officers.

7. Alignment with relevant Council policy

7.1 The

annual report is the method by which Council compares it’s activities

against the relevant annual or long-term plan.

8. Assessment of Significance against the

Council’s Significance and Engagement Policy

8.1 This

is not a significant decision under the Council’s significance and

engagement policy.

9. Consultation

9.1 There

is no consultation required.

10. Inclusion of Māori in the decision making process

10.1 There

is no consultation required.

11. Conclusion

11.1 An

Annual Report is required to be completed under the Local Government Act 2002.

11.2 The purpose of this report is to provide Councillors

with a draft version of the Annual Report 2014/15 to allow any feedback to

officers.

Tracey

Hughes

Senior

Accountant

Attachments

Attachment 1: A1417003 -

Annual Report 2014-15 Draft Financials and activity statements

Attachment 2: A1396738

- Draft Annual Report 2014-15 Statement of Service Performance (Circulated

separately)

|

|

Audit, Risk and Finance Subcommittee

10 September 2015

|

REPORT R4211

Carry

Forwards from 2014/15

1. Purpose of Report

1.1 To

inform the Committee of the process followed, and request approval of the

resulting carry forward of unspent budget.

2. Delegations

2.1 The

Audit, Risk and Finance Committee has oversight of the management of financial

risk and makes recommendations to the Governance Committee and to Council.

3. Recommendation

|

THAT the report Carry Forwards

from 2014/15 (R4211) be

received.

|

Recommendation

to Governance Committee and Council

|

THAT

$4,233,000 of unspent capital budget from 2014/15 be carried forward for use

in 2015/16;

AND THAT

$403,000 of capital spent in 2014/15 be offset against 2015/16 budgets;

AND THAT

an amount of $107,000 operating budget be carried forward for use in 2015/16.

|

4. Background

4.1 The

capital programme for 2014/15, as agreed in the Annual Plan 2014/15, totalled

$54.9 million including staff costs of $2.1 million and excluding NRSBU (all

figures quoted in this report do not include vested assets).

4.2 Carry

forwards totalling $1.7 million from 2013/14 were added to this giving a new

total capital programme of $56.6 million.

4.3 The

last budget projections were completed by officers in early May 2015, as part

of the Long Term Plan 2015-25 process. This process revised the 2014/15 capital

programme down to $35.0 million.

4.4 Capital

expenditure for 2014/15 totalled $30.7 million, a variance of $4.3 million

against the projection.

4.5 The

organisation delivered 84% of the approved physical works programme for the

year. Physical works is essentially asset construction and does not include

other capital items such as design and consenting.

4.6 Of

the total $24.2 million variance against original budget, $11.4 million is

attributable to not acquiring the Nelson School of Music and the Theatre Royal.

A further $4.4 million relates to scheduling changes for the Trafalgar Centre

and Saxton Creek upgrade.

4.7 Capital

projects that were budgeted in 2014/15 but subsequently removed through the

projections were then reconsidered for the Long Term Plan 2015-25.

4.8 The

2015/16 Annual Plan has a capital programme of $55.3 million including projects

carried over from 2014/15 through the LTP process.

4.9 Once

the 2014/15 year was closed for processing, officers collated data relating to

the capital projects undertaken during the year, identifying variances against

the last projection. Project managers were asked to identify which variances

represented savings, and where they wished to carry forward budget into 2015/16

they were asked to support their request. Senior Leadership Team reviewed the

resulting information with the project managers against agreed criteria.

4.10 Reasons

for carry forwards being requested include: expenditure committed but suppliers

unable to deliver before financial year end, delays related to vendors or other

stakeholders, and construction delays.

5. Discussion

Savings

5.1 Officers

identified $451,000 of savings in capital expenditure against projection. This

will have a positive impact on interest, depreciation and debt levels, in

excess of that already identified through the 2015/16 Annual Plan.

5.2 Savings

represent renewals budgets, land purchases budgets and staff time not required

along with savings against completed projects or stages of projects.

Capital

carry forwards

5.3 For

renewals budgets and multi-year projects, any spend over the 2014/15 projection

is considered a timing variance and is offset against the 2015/16 budget,

thereby reducing it in the amount of $403,000.

5.4 Officers

have requested that $4.2 million be carried forward into 2015/16, revising the

total capital programme to $59.5 million. Interest, depreciation, and debt

relating to these amounts was already built into the 2015/16 Annual Plan.

5.5 Totals

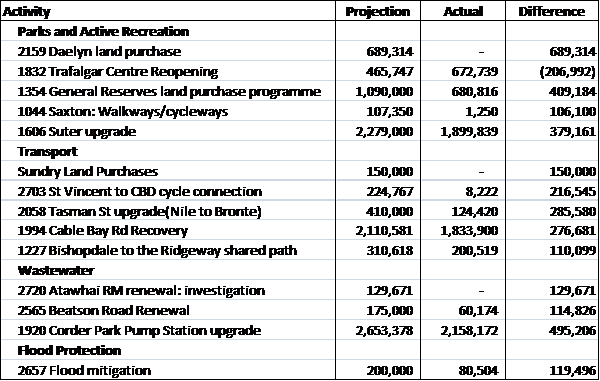

by activity are as follows:

Projects

with differences against projection greater than $100,000 are as follows:

Operating

expenditure carry forwards

5.6 It

is not normal practise to carry forward operating expenditure. The items below

represent specific projects that cross the 2014/15 and 2015/16 financial years,

and were budgeted/projected on a whole of project basis. In these cases,

anticipated spend did not occur in 2014/15 and it is recommended that the

budget remaining be added to that already approved for 2015/16. This treatment

means that the whole of project budget remains the same.

|

Activity

|

Project

|

2015/16 Budget Reduction $000

|

Carry forward to 2015/16 $000

|

|

Corporate

|

Councillor training

|

|

42

|

|

Corporate

|

Condition assessments

|

|

27

|

|

Corporate

|

Property assets review

|

|

38

|

6. Options

6.1 Work

has continued on 2014/15 capital projects following the resolution at the

Audit, Risk and Finance committee on 30 July 2015 and costs will have been

incurred. There is therefore no viable option other than to accept the

officers’ recommendation.

7. Alignment with relevant Council policy

7.1 The

amounts proposed to be carried forward to 2015/16 were approved spending in the

Annual Plan 2014/15.

8. Assessment of Significance against the

Council’s Significance and Engagement Policy

8.1 This

is not a significant decision under the Council’s significance and

engagement policy.

9. Consultation

9.1 The

amounts proposed to be carried forward were already consulted on through the

Annual Plan 2014/15.

10. Inclusion of Māori in the decision making

process

10.1 No

specific consultation with Maori has been undertaken in preparation of this

report.

11. Conclusion

11.1 An

analysis of capital expenditure against projection for 2014/15 and subsequent

review by Senior Leadership Team indicates:

11.2 There

are savings from the capital budget of $0.5 million;

11.3 Renewals

and multi-year projects overspent by $0.4 million should be offset against

2015/16 budgets;

11.4 $4.2

million of capital budget not spent should be carried forward into 2015/16.

11.5 $107,000

of operating expenditure not spent should be carried forward into 2015/16.

Tracey

Hughes

Senior

Accountant

Attachments

Nil

|

|

Audit, Risk and Finance Subcommittee

10 September 2015

|

REPORT R4777

Draft

Internal Audit Charter

1. Purpose

of Report

1.1 To approve the Draft Internal Audit Charter.

2. Delegations

2.1 The

Audit, Risk and Finance Subcommittee has responsibility for internal audit.

3. Recommendation

|

THAT the report Draft Internal

Audit Charter (R4777) and its

attachment (A1395134) be

received.

|

Recommendation

to Governance Committee and Council

|

THAT the

Draft Internal Audit Charter (A1395134) be approved.

|

4. Discussion

4.1 Council

recently established an internal audit role within the Organisational Assurance

team following feedback for Audit NZ. It is appropriate to have an

Internal Audit Charter.

4.2 The

Internal Audit Charter is a formal document that defines the purpose, authority

and responsibility of the internal audit function. The charter establishes the

position of the internal audit function within the organisation; authorises

access to records, staff and physical property relevant to the performance of

internal audit engagements; and defines the scope of work.

4.3 It

is intended that a risk based internal audit plan will be brought to the

Committee at least annually. The intention is to bring this to the 12

November committee meeting after some risk assessments have been undertake

across the organisation.

5. Options

5.1 Accept

the recommendation – approve the Draft Internal Audit Charter.

5.2 Reject

the recommendation – not approve the Draft Internal Audit Charter.

6. Alignment

with relevant Council policy

6.1 This

decision is not inconsistent with any other previous Council decision.

7. Assessment

of Significance against the Council’s Significance and Engagement Policy

7.1 This

is not a significant decision under the Council’s Significance and

Engagement Policy.

8. Consultation

8.1 No

consultation has been undertaken in preparing this charter.

9. Inclusion

of Māori in the decision making process

9.1 No

consultation with Maori has been undertaken in preparing this charter.

Nikki

Harrison

Group

Manager Corporate Services

Attachments

Attachment 1: A1395134 -

Draft Internal Audit Charter

Draft Internal Audit Charter

Effective Date: September

2015

Review Date: September 2018

1.

Contact:

Manager Organisational Assurance

1. Introduction

1.1. Internal Auditing is an independent

and objective assurance and advisory activity. It assists the Council in

accomplishing its objectives by bringing a systematic and disciplined approach

to evaluate and improve the effectiveness of the organisation’s

performance, risk management, internal control and the application of policy

and process.

2. Role

2.1. The internal audit activity is

established by the Audit, Risk and Finance Sub-Committee (AR&F) and the

Manager Organisational Assurance. The internal audit activity’s

responsibilities are defined and approved by the Council (by recommendation

from the Governance Committee) as part of their oversight role.

3. Professionalism

3.1. Professional oversight of the

internal audit activity will be guided by reference to The Institute of

Internal Auditors’ mandatory guidance including the Definition of

Internal Auditing, the Code of Ethics, and the International Standards for

the Professional Practice of Internal Auditing (Standards). This mandatory

guidance constitutes principles of the fundamental requirements for the

professional practice of internal auditing and for evaluating the effectiveness

of the internal audit activity’s performance.

3.2. The Institute of Internal

Auditors’ Practice Advisories, Practice Guides, and Position Papers will

also be adhered to as applicable to guide operations. In addition, the internal

audit activity will adhere to the Council’s relevant policies and

procedures and the internal audit activity’s standard operating

procedures manual.

4. Authority

4.1. The

internal audit activity, with strict accountability for confidentiality and

safeguarding records and information, is authorised to have full, free, and

unrestricted access to any and all of Nelson City Council’s records,

physical properties, and employees pertinent to carrying out any engagement.

All employees are required to assist the internal audit activity in fulfilling

its roles and responsibilities. The internal audit activity will also have free

and unrestricted access to the Chief Executive, the Governance Committee Chair

and the AR&F Committee (through the Chair).

5. Organisation

5.1. The

Internal Audit and Procurement Analyst (IA & PA) will report to the Manager

Organisational Assurance. In order to ensure the internal activity has a

level of organisational independence the internal auditor may from time to time

interact with the Chair of the Audit, Risk and Finance Committee.

5.2. The

AR&F sub-committee will:

· Approve the internal audit charter

and any amendments.

· Approve the risk based internal audit

plan.

· Receive communications from the IA

& PA on the internal audit activity’s performance relative to its

plan and other matters.

· Make appropriate inquiries of

management and the IA & PA to determine whether there is inappropriate

scope or resource limitations.

5.3. The

IA & PA will communicate and interact directly with the ARF Committee

through the Chair of AR&F if required.

6. Independence and Objectivity

6.1. The

internal audit activity will remain free from interference by any element in

the organisation, including matters of audit selection, scope, procedures,

frequency, timing, or report content to permit maintenance of a necessary

independent and objective mental attitude.

6.2. Internal

auditors will have no direct operational responsibility or authority over any

of the activities audited. Accordingly, they will not implement internal

controls, develop procedures, install systems, prepare records, or engage in

any other activity that may impair internal auditor’s judgment.

6.3. Internal

auditors will exhibit the highest level of professional objectivity in

gathering, evaluating, and communicating information about the activity or

process being examined. Internal auditors will make a balanced assessment of

all the relevant circumstances and not be unduly influenced by their own

interest or by others in forming judgments.

6.4. The

IA & PA will confirm to the AF&R sub-committee, if there are concerns

about the organisational independence of the internal audit activity.

7. Responsibility

7.1. The

scope of internal auditing encompasses, but is not limited to, the examination

and evaluation of the adequacy and effectiveness of the organisation’s

performance, risk management, and internal controls as well as the quality of

performance in carrying out assigned responsibilities to achieve the

organisation’s stated goals and objectives. This includes:

· Evaluating risk exposure relating to

achievement of the organisation’s strategic objectives.

· Evaluating the reliability and

integrity of information and the means used to identify, measure, classify, and

report such information.

· Evaluating the systems established to

ensure compliance with those policies, plans, procedures, laws, and regulations

which could have a significant impact on the organisation.

· Evaluating the means of safeguarding

assets and, as appropriate, verifying the existence of such assets.

· Evaluating the effectiveness and

efficiency with which resources are employed.

· Evaluating operations or programs to

ascertain whether results are consistent with established objectives and goals

and whether the operations or programs are being carried out as planned.

· Monitoring and evaluating the

effectiveness of the organisation’s risk management processes.

· Performing investigation and advisory

services related to risk management and control as appropriate for the

organisation

· Liaising with external auditors in

the performance of their duties.

· Performing investigation and advisory

services related to risk management and control as appropriate for the

organisation.

· Reporting periodically on the

internal audit activity’s purpose, authority, responsibility, and

performance relative to its plan.

· Reporting significant risk exposures

and control issues, including fraud risks, and other matters needed or

requested by the AR&F sub-committee.

· Evaluating specific operations at the

request of the AR&F sub-committee or management, as appropriate.

8. Internal Audit Plan

8.1. At

least annually, the IA & PA, Manager of Organisational Assurance and GM Corporate

Services will submit to the Senior Leadership Team (SLT) and the AR&F

sub-committee an internal audit plan for review and recommendation to the

Governance Committee for approval. The internal audit plan will consist of a

work schedule as well as budget and resource requirements for the next fiscal

year. The IA & PA will communicate the impact of resource limitations and

significant interim changes to SLT and the AR&F sub-committee.

8.2. The

internal audit plan will be developed based on a prioritisation of a list of

all potential audit topics[1]

using a risk-based methodology, including input of SLT and the AR&F

sub-committee. The IA & PA will review and adjust the plan, as necessary,

in response to changes in the organisation’s business, risks, operations,

programs, systems and controls. Any significant deviation from the approved

internal audit plan will be considered by AR&F after seeking guidance (if

appropriate) from the Chief Executive and if necessary the Governance

Committee.

9. Reporting and Monitoring

9.1. A

written report will be prepared and issued by the IP & PA following the

conclusion of each internal audit engagement and will be distributed as

appropriate. Internal audit results will, where appropriate, be communicated to

SLT, AR&F sub-committee and the Governance Committee

9.2. The

internal audit report should include management’s response and corrective

action taken or to be taken in regard to the specific findings and

recommendations. Management’s response, whether included within the

original audit report or provided thereafter by management of the audited area

should include a timetable for anticipated completion of action to be taken and

an explanation for any corrective action that will not be implemented.

9.3. The

internal audit activity will be responsible for appropriate follow-up on

engagement findings and recommendations, although it is management’s

responsibility to address. All significant findings will remain in an open

issues file until cleared.

9.4. The

IA & PA will periodically report to SLT and the AR&F sub-committee on

the internal audit activity’s purpose, authority, and responsibility, as

well as performance relative to its plan. Reporting will also include

significant risk exposures and control issues, including fraud risks, and other

matters needed or requested by the Governance Committee, the AR&F

sub-committee or SLT.

10. Quality Assurance and Improvement

Program

10.1. The internal

audit activity will maintain a quality assurance and improvement program that

covers all aspects of the internal audit activity. The program will include an

evaluation of the internal audit activity’s conformance with the

Definition of Internal Auditing and the Standards and an evaluation of

whether internal auditors apply the Code of Ethics. The program also assesses

the efficiency and effectiveness of the internal audit activity and identifies

opportunities for improvement.

10.2. The IA &

PA will communicate to SLT and the ARF Committee on the internal audit

activity’s quality assurance and improvement program, including results

of ongoing internal assessments and external assessments conducted at least

every five years. Is this professional practice? Yes – can take out

if you want.

11. Update of the Internal Audit Charter

11.1. The IA &

PA will ensure this Internal Audit Charter is periodically reviewed and revised

for relevance. Any changes to the Internal Audit Charter will require

consideration by the AR&F sub-committee and the approval of the Council (by

recommendation from the Governance Committee) after taking account of the

recommendation of the Chief Executive.

Approved by resolution of Council at the meeting held

on TBA